Health Ingredients Market Size

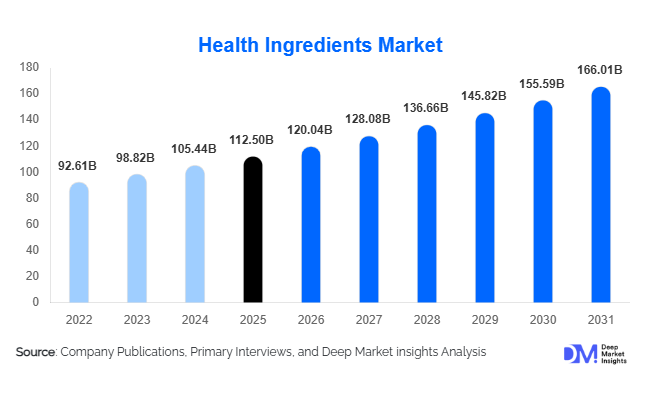

According to Deep Market Insights, the global health ingredients market size was valued at USD 112.5 billion in 2025 and is projected to grow from USD 120.04 billion in 2026 to reach USD 166.01 billion by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer awareness around preventive healthcare, increasing incorporation of functional components into everyday food and beverages, and rapid expansion of the dietary supplements industry worldwide. Growing demand for immunity-enhancing ingredients, plant-based proteins, probiotics, and specialty nutraceuticals is reshaping formulation strategies across food, beverage, and pharmaceutical manufacturers. Strong R&D investments, regulatory harmonization, and expanding middle-class consumption in the Asia-Pacific are further accelerating global market expansion.

Key Market Insights

- Vitamins account for nearly 27% of the global market share in 2025, driven by widespread fortification programs and strong post-pandemic immunity demand.

- Plant-based ingredients represent approximately 42% of the total market share, reflecting clean-label and sustainability preferences.

- Dietary supplements dominate applications with 35% share, supported by direct-to-consumer health trends.

- North America leads with 32% market share in 2025, backed by high supplement penetration and preventive healthcare spending.

- Asia-Pacific is the fastest-growing region, projected to expand at over 8% CAGR through 2031.

- The top five players collectively account for nearly 38% of global revenue, indicating moderate consolidation.

What are the latest trends in the health ingredients market?

Personalized and Precision Nutrition

Personalized nutrition is rapidly transforming ingredient innovation. Consumers are increasingly relying on microbiome testing, wearable health devices, and digital health platforms to guide supplement and functional food choices. This has accelerated demand for customized vitamin blends, targeted probiotic strains, and condition-specific formulations for immunity, cognition, and metabolic health. Ingredient suppliers are investing in clinically validated bioactive compounds and advanced delivery formats such as microencapsulation to improve bioavailability. The shift toward data-driven nutrition is enabling premium pricing and stronger brand differentiation.

Shift Toward Plant-Based and Sustainable Ingredients

Plant-based proteins, algal omega-3, fermentation-derived vitamins, and botanical extracts are gaining significant traction. Sustainability-driven procurement by multinational food manufacturers is influencing supplier strategies, with carbon footprint reduction and traceable sourcing becoming competitive advantages. Upcycled raw materials and green extraction technologies are also being adopted to improve margins and meet ESG compliance standards. This trend is particularly strong in Europe and North America, where consumers actively prioritize environmentally responsible products.

What are the key drivers in the health ingredients market?

Rising Preventive Healthcare Spending

Consumers globally are prioritizing preventive healthcare to manage chronic conditions such as cardiovascular disease, diabetes, and obesity. This is increasing demand for omega-3, fiber, vitamins, and mineral fortification in everyday food products. The global dietary supplements industry surpassed USD 180 billion in 2025, directly supporting ingredient demand growth.

Expansion of Functional Foods and Beverages

Functional beverages, protein-fortified snacks, dairy alternatives, and energy drinks are witnessing robust demand, particularly in the Asia-Pacific region. Food manufacturers are increasingly incorporating probiotics, plant proteins, and specialty nutraceuticals into mainstream SKUs, significantly expanding bulk ingredient volumes.

What are the restraints for the global market?

Regulatory and Claims Compliance Challenges

Stringent regulations regarding health claims in major markets increase R&D costs and extend product approval timelines. Clinical substantiation requirements pose barriers for smaller manufacturers.

Raw Material Price Volatility

Fluctuations in fish oil, whey protein, and botanical raw materials directly impact profit margins. Volatility in agricultural and marine sourcing markets remains a key operational challenge.

What are the key opportunities in the health ingredients industry?

Emerging Market Expansion

Rapid urbanization and growing middle-class populations in India, Southeast Asia, Brazil, and the Middle East present large-scale opportunities. Government-led food fortification initiatives for iron, vitamin D, and iodine create institutional demand for bulk ingredient suppliers.

Fermentation and Biotech-Based Innovation

Advanced fermentation technologies are enabling cost-effective production of high-purity vitamins, probiotics, and specialty amino acids. Companies investing in biotech platforms can improve margins while reducing reliance on volatile natural sources.

Ingredient Type Insights

Vitamins continue to lead the global health ingredients market, accounting for approximately 27% of total revenue in 2025. Their leadership position is primarily driven by universal application across dietary supplements, fortified staple foods, functional beverages, dairy products, and clinical nutrition formulations. Government-led fortification programs targeting vitamin D, vitamin A, and B-complex deficiencies, particularly in Asia-Pacific, Africa, and parts of Latin America, further strengthen baseline demand. In addition, post-pandemic immunity awareness has significantly increased the consumption of vitamins C and D, reinforcing their dominance across both developed and emerging markets.

Probiotics and prebiotics represent one of the fastest-growing sub-segments within specialty health ingredients, supported by rising global awareness of gut microbiome health and its connection to immunity, mental health, and metabolic function. Increasing clinical validation of strain-specific benefits is driving higher-value formulations in supplements and functional dairy. Meanwhile, plant proteins are expanding steadily within the proteins & amino acids category, fueled by the global shift toward vegan, vegetarian, and flexitarian diets. Pea, soy, and rice proteins are increasingly used in sports nutrition and dairy alternatives. Specialty nutraceuticals such as collagen peptides, coenzyme Q10, and glucosamine are gaining traction, particularly among aging populations in North America, Europe, and Japan, where demand for bone, joint, and cardiovascular support is accelerating.

Application Insights

Dietary supplements dominate the application landscape, accounting for approximately 35% of global revenue in 2025. The segment’s leadership is driven by strong direct-to-consumer sales models, e-commerce penetration, personalized nutrition trends, and higher consumer willingness to invest in preventive healthcare. Subscription-based supplement platforms and influencer-driven marketing strategies have further expanded product reach, particularly in North America and Asia-Pacific.

Functional foods and beverages collectively represent nearly 40% of the market, supported by reformulation of mainstream packaged foods to include added protein, fiber, vitamins, and probiotics. Manufacturers are increasingly embedding health ingredients into everyday consumption formats such as breakfast cereals, snack bars, ready-to-drink beverages, and dairy alternatives. Infant nutrition and clinical nutrition remain high-margin applications, especially in developed economies with aging populations and rising chronic disease prevalence. Medical-grade nutrition solutions for metabolic disorders, elderly care, and recovery support are creating stable long-term demand.

Form Insights

Powdered ingredients account for approximately 48% of global volume, making them the leading form segment. Their dominance is attributed to superior shelf stability, cost-effective transportation, formulation flexibility, and compatibility across multiple applications, including beverages, supplements, and bakery products. Bulk powder formats are particularly preferred by B2B manufacturers due to scalability advantages in large-scale production.

Liquid forms are widely used in beverage fortification and pediatric applications where rapid solubility and bioavailability are critical. Meanwhile, granules and encapsulated formats are gaining traction in specialty supplement manufacturing due to improved controlled-release functionality, taste masking capabilities, and enhanced nutrient stability. Technological advancements in microencapsulation and spray-drying are further improving ingredient performance across various delivery systems.

| By Ingredient Type | By Application | By Form | By Source |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds approximately 32% share of the global market in 2025, with the United States accounting for nearly 85% of regional demand. Regional growth is driven by high dietary supplement penetration, advanced preventive healthcare awareness, and strong R&D capabilities among major ingredient manufacturers. The presence of established nutraceutical brands, favorable regulatory clarity for supplement labeling, and strong e-commerce infrastructure further support expansion. Rising demand for plant-based proteins and sports nutrition ingredients is also reinforcing market growth. Canada contributes steadily, supported by clean-label preferences and natural health product regulations.

Asia-Pacific

Asia-Pacific represents roughly 30% of the global market and is projected to grow at over 8% CAGR through 2031, making it the fastest-growing region. China, India, and Japan are major demand centers. China’s growth is supported by rapid urbanization, increasing disposable income, and expanding domestic nutraceutical production. India is emerging as the fastest-growing country due to government-backed fortification initiatives, expanding middle-class health awareness, and “Make in India” manufacturing incentives. Japan’s aging population is driving strong demand for bone, heart, and cognitive health ingredients. Southeast Asian countries are also witnessing rising functional beverage consumption, further strengthening regional demand.

Europe

Europe accounts for approximately 25% of global revenue, led by Germany, the UK, and France. Regional growth is driven by strong consumer preference for clean-label, non-GMO, and sustainably sourced ingredients. Strict regulatory frameworks ensure high product quality, which enhances consumer trust and supports premium pricing. Germany leads in supplement consumption, while the UK shows strong demand for plant-based and sports nutrition ingredients. Aging demographics across Western Europe continue to drive demand for vitamins, omega-3, and specialty nutraceuticals.

Latin America

Latin America contributes nearly 6% of global demand, with Brazil dominating regional consumption. Growth drivers include rising middle-class purchasing power, increasing supplement awareness, and expanding retail distribution networks. Mexico and Argentina are also showing steady adoption of fortified food products. Government-led nutrition improvement programs and gradual regulatory modernization are expected to support long-term regional expansion.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of global revenue. Growth is primarily driven by GCC fortification initiatives targeting vitamin D and iron deficiencies, rising healthcare expenditure, and growing urban health awareness. The UAE and Saudi Arabia are key demand centers, supported by high disposable income and premium supplement adoption. In Africa, expanding food fortification programs and international development partnerships are creating institutional demand for bulk vitamins and minerals. Increasing local manufacturing capabilities is expected to gradually reduce import dependence and support regional supply chain stability.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Health Ingredients Market

- DSM-Firmenich

- BASF SE

- Cargill Incorporated

- Archer Daniels Midland (ADM)

- Kerry Group

- Nestlé Health Science

- Glanbia PLC

- IFF (Nutrition & Biosciences)

- Lonza Group

- Evonik Industries

- Givaudan

- Chr. Hansen

- Roquette Frères

- Arla Foods Ingredients

- Ingredion Incorporated