Halawa and Tahini Market Size

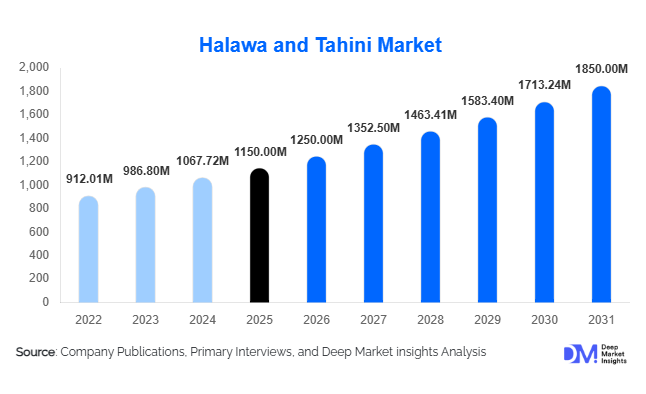

According to Deep Market Insights, the global Halawa and Tahini market size was valued at USD 1,150 million in 2025 and is projected to grow from USD 1,250 million in 2026 to reach USD 1,850 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The market growth is primarily driven by rising global demand for plant-based protein spreads, increasing adoption of Mediterranean and Middle Eastern diets, and the growing popularity of clean-label, minimally processed food products across developed and emerging economies.

Key Market Insights

- Tahini dominates global consumption trends due to its versatility in savory foods, vegan diets, and functional food formulations.

- Halawa is transitioning from a regional confectionery to a premium ethnic snack category with increasing penetration in Europe and North America.

- Middle East & Africa remains the production and consumption hub, supported by strong cultural demand and established sesame processing industries.

- Europe is witnessing strong adoption of vegan and Mediterranean diets, boosting demand for tahini-based spreads and sauces.

- APAC is emerging as the fastest-growing region due to rising health awareness, urbanization, and expanding retail penetration.

- E-commerce platforms are reshaping distribution, enabling niche ethnic food brands to reach global consumers efficiently.

What are the latest trends in the Halawa and Tahini Market?

Rise of Plant-Based and Functional Food Integration

The global shift toward plant-based nutrition is significantly influencing the halawa and tahini market. Tahini is increasingly used as a dairy alternative and nut butter substitute, particularly in vegan and allergen-sensitive diets. Food manufacturers are incorporating tahini into protein bars, salad dressings, dips, and bakery fillings to enhance nutritional value. Similarly, halawa is being reformulated into functional snack bars enriched with protein, fiber, and natural sweeteners such as honey and date syrup. This transformation is positioning sesame-based products within the broader functional food ecosystem, expanding their relevance beyond traditional ethnic consumption.

Premiumization and Flavor Innovation

Manufacturers are focusing heavily on premium and flavored product innovations to attract urban consumers. Flavored tahini variants such as garlic, chili, chocolate, and herb-infused blends are gaining traction in retail markets. Organic and stone-ground tahini products are also expanding in premium supermarket segments. Halawa is being repositioned as a gourmet confectionery with pistachio, cocoa, and almond inclusions. This premiumization trend is allowing brands to command higher margins and strengthen their positioning in developed markets.

What are the key drivers in the Halawa and Tahini market?

Rising Global Health and Clean-Label Consumption

The increasing preference for clean-label and minimally processed foods is a major driver of market growth. Consumers are actively avoiding hydrogenated fats and artificial additives, positioning tahini as a healthier alternative to conventional spreads. Its high content of healthy fats, plant-based protein, and essential minerals is driving demand across fitness-focused and health-conscious populations globally.

Expansion of Ethnic and Mediterranean Food Adoption

The globalization of food culture is significantly expanding demand for halawa and tahini. Mediterranean and Middle Eastern cuisines are now widely integrated into mainstream foodservice menus across North America and Europe. Restaurants, fast-casual chains, and packaged food brands are increasingly using tahini-based sauces and halawa-inspired desserts, boosting product visibility and consumption.

Growth of Vegan and Plant-Based Diets

The rising adoption of vegan and vegetarian diets is accelerating demand for sesame-based spreads. Tahini, being naturally plant-based and allergen-friendly, is widely used in dairy-free recipes and protein-focused diets. This dietary shift is particularly strong in urban populations across Europe, North America, and parts of Asia-Pacific, contributing to sustained demand growth.

What are the restraints for the global market?

Raw Material Supply Volatility

Sesame seed production is highly dependent on agricultural output from countries such as Sudan, India, and Ethiopia. Climate variability, geopolitical risks, and supply chain disruptions often lead to price fluctuations, impacting production costs and profit margins across the value chain.

Limited Awareness in Emerging Markets

Despite global expansion, halawa and tahini remain relatively niche in several emerging economies. Limited consumer awareness, unfamiliarity with usage applications, and competition from established local spreads restrict mass-market penetration in regions such as parts of Asia-Pacific and Latin America.

What are the key opportunities in the Halawa and Tahini industry?

Expansion in Functional and Nutritional Food Segments

The integration of tahini into functional foods such as protein bars, sports nutrition products, and fortified snacks presents a significant opportunity. Growing demand for plant-based protein sources is encouraging manufacturers to position sesame-based products as nutrient-dense superfoods. This opens strong growth potential in health-focused retail and fitness markets.

Growth of E-commerce and Direct-to-Consumer Channels

E-commerce platforms are enabling global accessibility for niche ethnic food brands. Online retail allows producers to bypass traditional distribution barriers and reach international consumers directly. Subscription-based models, specialty health-food platforms, and digital grocery ecosystems are driving repeat purchases and brand loyalty.

B2B Industrial Food Applications

Food manufacturers are increasingly using tahini and sesame paste as key ingredients in sauces, bakery fillings, and confectionery formulations. Halawa is also gaining traction in processed desserts and energy bars. This industrial integration is unlocking large-volume demand from the bakery, confectionery, and packaged food sectors globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1150 Million |

| Market Size in 2026 | USD 1250 Million |

| Market Size in 2031 | USD 1850 Million |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global market for tahini and related sesame-based products is strongly shaped by evolving consumer preferences, cultural consumption patterns, and increasing awareness of plant-based nutrition. Among all product types, tahini continues to hold a dominant position in the global landscape, accounting for nearly 48% of the total market share. This dominance is primarily attributed to its deep integration into both traditional and modern diets, along with its expanding use across household consumption and large-scale industrial food processing applications. Tahini’s creamy texture, high protein content, and nutrient-rich profile make it a preferred ingredient in vegan and vegetarian diets, where it is widely used as a substitute for dairy-based spreads and sauces. Additionally, the growing popularity of Mediterranean and Middle Eastern cuisines across North America, Europe, and Asia-Pacific has significantly elevated its global demand trajectory.The key growth driver for tahini is its multifunctional usage in food preparation, ranging from dips such as hummus to salad dressings, bakery fillings, and dessert bases. Food manufacturers are increasingly incorporating tahini into processed and packaged foods due to its natural emulsification properties and clean-label appeal. The rise of health-conscious consumer behavior is also fueling demand, as tahini is perceived as a nutrient-dense superfood rich in healthy fats, calcium, iron, and antioxidants. Furthermore, the expansion of vegan food culture and plant-based diets has significantly contributed to its sustained global growth momentum.Sugar-free and functional variants are emerging as a highly promising niche segment, particularly targeting diabetic consumers, fitness enthusiasts, and individuals following low-sugar or ketogenic diets. These products are often fortified with additional nutrients such as protein, fiber, or omega-3 fatty acids, further enhancing their appeal in the functional food category. The growth of this segment is strongly supported by increasing global prevalence of lifestyle-related diseases and the rising demand for guilt-free indulgence products that align with modern dietary restrictions.

Application Insights

Household consumption remains the leading application segment in the global market, supported by increasing home cooking trends, rising awareness of healthy eating habits, and the growing popularity of international cuisines in everyday diets. Consumers are increasingly using tahini and halawa as versatile pantry staples, incorporating them into breakfast spreads, sauces, smoothies, and baking recipes. The convenience of ready-to-use packaging and the availability of diverse flavor profiles have further strengthened household adoption across both developed and emerging economies.The food processing industry represents the fastest-growing application segment, driven by its extensive use of tahini as a functional ingredient in bakery products, sauces, confectionery items, and ready-to-eat meals. Food manufacturers value tahini for its emulsifying properties, flavor enhancement capabilities, and ability to improve texture and nutritional profile in processed foods. The expansion of clean-label and natural ingredient formulations has significantly accelerated its integration into industrial food production.Functional food applications are emerging as a high-growth sub-segment, particularly in protein bars, vegan desserts, health shakes, and fortified snacks. The increasing demand for nutrient-dense foods that support fitness, weight management, and overall wellness is driving manufacturers to integrate tahini into health-focused product formulations. This segment is expected to witness sustained growth as consumers prioritize functional benefits alongside taste and convenience.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the global distribution landscape due to their extensive product visibility, strong brand presence, and ability to influence impulse purchasing behavior. These retail formats offer consumers the advantage of product comparison, variety selection, and immediate availability, making them a preferred channel for mainstream household purchases. The presence of dedicated health food sections within large retail stores has also boosted the visibility of organic and premium sesame-based products.Online retail represents the fastest-growing distribution channel, driven by the rapid expansion of e-commerce platforms, changing consumer shopping behavior, and increasing demand for convenience. Digital platforms enable consumers to access a wide variety of international and specialty food products that may not be available in local stores. Subscription-based models, direct brand websites, and third-party marketplaces are significantly contributing to the growth of online sales.Direct-to-consumer (DTC) channels are gaining traction as brands increasingly focus on building stronger customer relationships, improving profit margins, and enhancing brand loyalty. Through digital platforms and subscription models, manufacturers are able to directly engage with consumers, gather feedback, and introduce new product innovations more efficiently.

Explore more data points, trends and opportunities Download Free Sample Report

Halawa and Tahini Market Segmentations

By Product Type

- Tahini

- Halawa / Halva Confectionery

- Flavored Tahini

- Organic & Premium Sesame-Based Products

- Functional & Sugar-Free Variants

By Ingredient Base

- Hulled Sesame Seeds-Based Products

- Unhulled Sesame Seeds-Based Products

- Blended Seed Formulations

- Natural Sweetener-Based Halawa (Honey/Date Syrup)

By Packaging Type

- Glass Jars

- Plastic Tubs

- Squeeze Bottles

- Single-Serve Sachets

- Bulk & Industrial Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail / E-commerce Platforms

- Specialty & Organic Stores

- Foodservice (HoReCa)

- B2B / Industrial Supply Chains

End-Use Application

- Household Consumption

- Food Processing Industry

- Foodservice Industry

- Functional & Nutritional Foods

Regional Insights

Middle East & Africa

The Middle East & Africa region dominates the global market with approximately 36% market share in 2025, largely due to its deep-rooted cultural consumption patterns and long-established sesame processing industries. Countries such as Turkey, Egypt, Israel, and Saudi Arabia serve as both major consumption hubs and production centers, ensuring a stable supply chain and strong domestic demand. Tahini and halawa are integral components of daily diets, reinforcing consistent consumption across all income groups.The key growth drivers in this region include strong culinary heritage, high per capita consumption of sesame-based products, and robust export infrastructure supporting global distribution. Additionally, rising urbanization and modernization of food retail systems are expanding product accessibility beyond traditional markets. Increasing tourism and the global popularity of Middle Eastern cuisine are further enhancing international demand for regionally produced sesame products.

Europe

Europe accounts for around 24% of the global market share, with strong demand concentrated in countries such as Germany, the United Kingdom, and France. The region’s growth is heavily influenced by increasing adoption of vegan and vegetarian lifestyles, rising awareness of clean-label foods, and growing interest in Mediterranean dietary patterns.The primary growth drivers in Europe include the rapid expansion of plant-based food trends, strong consumer preference for organic and non-GMO products, and increasing incorporation of ethnic cuisines into mainstream consumption habits. Additionally, regulatory emphasis on food transparency and sustainability has encouraged manufacturers to offer high-quality, minimally processed sesame-based products. The premiumization trend is also strong in Europe, with consumers willing to pay higher prices for artisanal and organic variants.

North America

North America holds approximately 22% market share, with the United States representing the largest contributor. Growth in this region is driven by rising health awareness, increasing popularity of Mediterranean diets, and the expansion of ethnic and specialty food retail channels. Consumers are increasingly adopting tahini as a healthier alternative to traditional spreads, supported by growing awareness of its nutritional benefits.Key growth drivers in North America include strong demand for plant-based proteins, rapid expansion of health-focused food categories, and increasing availability of international food products in mainstream supermarkets. The influence of fitness culture and wellness trends has also significantly boosted demand for functional and sugar-free variants. Furthermore, the growth of food delivery services and online grocery platforms has improved product accessibility across diverse consumer segments.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR of over 9.5%. Key markets such as China, India, Japan, and Australia are witnessing increasing demand due to rising disposable incomes, urbanization, and exposure to global food cultures. The region is gradually adopting sesame-based products as part of a broader shift toward healthier and more diverse dietary habits.The main growth drivers in Asia-Pacific include rapid expansion of modern retail infrastructure, increasing influence of Western and Middle Eastern cuisines, and growing awareness of health and wellness foods. Additionally, the rising popularity of vegan and vegetarian diets, particularly in urban centers, is significantly contributing to demand growth. E-commerce penetration is also playing a crucial role in introducing niche international food products to a broader consumer base.

Latin America

Latin America represents an emerging market with gradual but steady adoption of sesame-based products in countries such as Brazil, Mexico, and Argentina. While the market is still in a developing stage, increasing exposure to global dietary trends and rising health awareness are supporting demand growth.Key growth drivers in this region include expanding middle-class populations, increasing import penetration of functional food products, and growing interest in plant-based nutrition. Additionally, the influence of international cuisines through tourism and digital media is contributing to the gradual integration of tahini and halawa into local diets. As retail infrastructure improves, the region is expected to witness stronger long-term growth potential.

Key Players in the Global Halawa and Tahini Market

- Prince Tahini Co.

- Achva Food Industries

- Al Wadi Al Akhdar

- Soom Foods

- Halwani Bros

- Once Again Nut Butter Collective

- Ghorbani Brothers

- Roland Foods

- Joyva Corporation

- Krinos Foods

- Savola Group

- Sun Valley Foods

- Al Yaman Foods

- Sesajal S.A. de C.V.

- Beirut Sesame Co.