Gummy Market Size

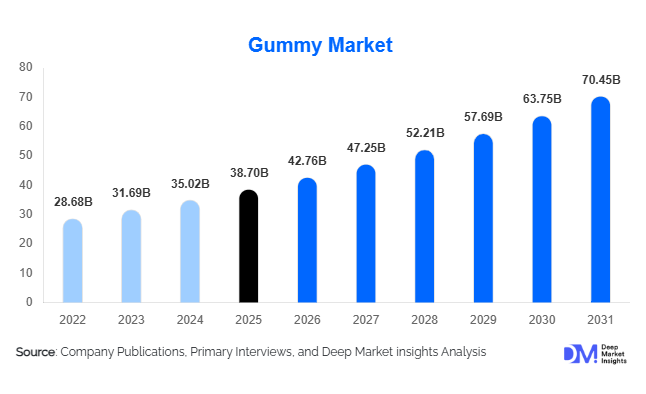

According to Deep Market Insights, the global gummy market size was valued at USD 38.7 billion in 2025 and is projected to grow from USD 42.76 billion in 2026 to reach USD 70.45 billion by 2031, expanding at a CAGR of 10.5% during the forecast period (2026–2031). The gummy market growth is primarily driven by increasing demand for functional nutrition, rising consumer preference for convenient supplement formats, and expanding adoption of sugar-free, vegan, and clean-label gummy products across global markets.

Key Market Insights

- Functional and nutraceutical gummies are rapidly transforming the market, with consumers increasingly preferring chewable wellness products over traditional tablets and capsules.

- Plant-based and pectin-based gummies are witnessing strong demand growth, supported by rising vegan populations and clean-label consumption trends.

- North America dominates the global gummy market, led by high nutraceutical spending, premium supplement consumption, and widespread adoption of wellness gummies.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, expanding e-commerce penetration, and increasing preventive healthcare awareness.

- E-commerce and direct-to-consumer channels are reshaping gummy sales, allowing brands to market personalized nutrition and subscription-based wellness products globally.

- Technological innovation in flavor masking, bioavailability enhancement, and controlled-release formulations is enabling manufacturers to expand premium gummy product portfolios.

Gummy Market Trends

Rise of Functional and Wellness Gummies

The gummy market is increasingly shifting toward functional nutrition and wellness-focused applications. Consumers are demanding gummies fortified with vitamins, minerals, collagen, probiotics, adaptogens, and botanical extracts that support immunity, sleep, stress management, digestive health, and beauty enhancement. Functional gummies are becoming mainstream across both adult and pediatric nutrition categories due to their convenience, pleasant taste, and improved compliance compared to traditional supplement formats. Manufacturers are investing heavily in clinically backed formulations and personalized nutrition concepts targeting specific consumer demographics such as women, athletes, children, and senior citizens. Beauty gummies infused with biotin, collagen, and hyaluronic acid are witnessing particularly strong growth among younger consumers focused on skincare and wellness.

Plant-Based and Sugar-Free Innovation

Demand for vegan, sugar-free, and clean-label gummies is reshaping global product innovation strategies. Pectin-based and agar-based gummies are increasingly replacing traditional gelatin formulations due to rising vegan populations and ethical sourcing concerns. Consumers are also seeking low-sugar and diabetic-friendly products formulated with natural sweeteners such as stevia and monk fruit. Regulatory pressure surrounding sugar reduction and artificial additives is encouraging manufacturers to reformulate products using organic ingredients, natural colors, and non-GMO certifications. Sustainable packaging solutions, biodegradable materials, and environmentally conscious sourcing practices are also becoming critical competitive differentiators within premium gummy segments.

Gummy Market Drivers

Growing Demand for Preventive Healthcare

The increasing global focus on preventive healthcare is one of the strongest growth drivers for the gummy market. Consumers are proactively investing in nutritional supplements that support long-term wellness, immunity enhancement, and disease prevention. Gummy supplements have gained significant popularity because they provide an enjoyable and convenient alternative to conventional capsules and tablets. Vitamin gummies, immunity gummies, and sleep-support formulations are experiencing rapid demand growth across North America, Europe, and Asia-Pacific. Aging populations and rising healthcare awareness are further accelerating demand for nutraceutical gummies that support bone health, cognitive wellness, cardiovascular health, and digestive balance.

Expansion of E-Commerce and Direct-to-Consumer Sales

The rapid growth of online retail and direct-to-consumer distribution channels is significantly expanding the gummy market globally. E-commerce platforms enable manufacturers to launch niche wellness products, target health-conscious consumers directly, and leverage subscription-based supplement models. Digital marketing, influencer campaigns, and social media wellness trends are further boosting gummy product visibility among younger demographics. Personalized nutrition brands are increasingly using online channels to offer customized gummy solutions based on lifestyle, dietary preferences, and health goals. The convenience of doorstep delivery and recurring subscription services has strengthened consumer loyalty and repeat purchases within the functional gummy segment.

Gummy Market Restraints

High Manufacturing and Ingredient Costs

The production of functional gummies involves higher manufacturing complexity and ingredient costs compared to conventional confectionery products. Specialized formulation requirements related to flavor masking, moisture control, texture stabilization, and ingredient bioavailability increase production expenses. Premium ingredients such as collagen peptides, probiotics, omega-3 oils, and botanical extracts further elevate manufacturing costs. Vegan and pectin-based formulations also remain more expensive than gelatin-based alternatives, limiting affordability in price-sensitive markets. These factors can compress profit margins and create pricing challenges for manufacturers operating in highly competitive retail environments.

Regulatory and Product Stability Challenges

The gummy market faces significant regulatory complexity across different countries regarding supplement labeling, dosage limits, medicinal claims, and ingredient approvals. Manufacturers operating globally must comply with varying standards related to nutraceutical products, CBD ingredients, sugar content, and child-safe packaging regulations. Shelf-life limitations and sensitivity to heat and humidity also create formulation and logistics challenges, especially in tropical regions. Functional ingredients such as probiotics and omega oils require advanced stabilization technologies to maintain efficacy over time, increasing operational complexity and quality assurance requirements for manufacturers.

Gummy Market Opportunities

Personalized Nutrition Gummies

The growing popularity of personalized nutrition presents substantial opportunities for gummy manufacturers. Consumers increasingly seek customized supplements tailored to their age, gender, lifestyle, and specific health concerns. Companies are leveraging AI-driven nutrition platforms and direct-to-consumer subscription models to provide personalized gummy packs targeting immunity, sleep, energy, digestion, beauty, and stress management. This trend is particularly attractive among younger consumers who value convenience, customization, and wellness-focused lifestyles. Personalized nutrition gummies also support higher margins and stronger customer retention compared to standardized supplement products.

Expansion into Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East represent major growth opportunities for gummy manufacturers. Rising disposable incomes, increasing urbanization, and improving healthcare awareness are accelerating demand for nutritional supplements and functional confectionery products in countries such as China, India, Brazil, Indonesia, and Saudi Arabia. Expanding retail modernization and e-commerce penetration are enabling global and regional brands to access previously underserved consumers. Manufacturers are increasingly investing in localized production facilities and region-specific formulations to cater to diverse taste preferences and regulatory environments while reducing supply chain costs.

Product Type Insights

Gummy supplements dominate the market, accounting for nearly 46% of global revenue in 2025 due to rising demand for convenient nutritional delivery systems. Vitamin gummies remain the leading category, driven by increasing preventive healthcare adoption and immunity-focused consumption patterns. Beauty gummies containing collagen, biotin, and skin-health ingredients are rapidly gaining popularity among younger consumers. Traditional gummy candies continue to maintain strong demand globally, particularly fruit-flavored and sour variants that appeal to children and impulse buyers. Sugar-free gummies are emerging as one of the fastest-growing categories due to increasing diabetic populations and rising health-conscious consumer behavior. CBD gummies and herbal wellness gummies are also expanding rapidly within specialized functional nutrition segments, particularly in North America.

Ingredient Base Insights

Gelatin-based gummies continue to dominate the market with nearly 58% market share owing to their cost efficiency, superior texture, and elasticity. However, pectin-based gummies are witnessing the fastest growth due to increasing demand for vegan and plant-based formulations. Manufacturers are increasingly using pectin and agar to address clean-label and ethical sourcing preferences among consumers in Europe and North America. Carrageenan and starch-based formulations are also gaining traction in specialty confectionery and nutraceutical applications where texture customization and stability are critical. Innovation in plant-derived ingredients is expected to further reshape the ingredient landscape over the coming years.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels, accounting for approximately 39% of global gummy sales in 2025. These channels benefit from strong product visibility, impulse purchases, and extensive retail penetration. Pharmacies and drug stores are highly important for nutraceutical gummies, particularly immunity, sleep, and digestive health products. However, online retail and direct-to-consumer channels are experiencing the fastest growth rates globally. Consumers increasingly prefer purchasing wellness gummies through e-commerce platforms due to subscription models, personalized recommendations, and wider product availability. Social media-driven marketing campaigns and influencer endorsements are also strengthening digital gummy sales across younger demographics.

Consumer Group Insights

Adults represent the largest consumer segment in the gummy market, accounting for nearly 48% of global demand in 2025. Rising adoption of immunity gummies, sleep aids, beauty supplements, and stress management products among working professionals is driving growth in this category. Children remain a major consumer group due to strong demand for vitamin gummies and fruit-flavored confectionery products. Geriatric consumers are increasingly adopting gummy supplements because they offer easier consumption compared to traditional tablets. Women-specific gummies targeting prenatal health, hair care, skin wellness, and hormonal support are also witnessing rapid expansion globally. Athletes and fitness-focused consumers are contributing to growing demand for energy gummies, electrolyte gummies, and sports nutrition formulations.

End-Use Insights

Nutraceuticals remain the largest end-use segment in the gummy market, accounting for nearly 44% of total market revenue in 2025. Preventive healthcare trends and growing awareness regarding dietary supplementation are fueling strong demand for functional gummies worldwide. The pharmaceutical sector is increasingly adopting gummy formulations for pediatric medicines and OTC wellness products due to improved patient compliance. Confectionery applications continue to maintain strong global demand, particularly among children and younger consumers seeking innovative flavors and textures. Sports nutrition is emerging as a high-growth end-use segment, supported by increasing gym memberships, active lifestyles, and rising demand for convenient energy and recovery supplements.

| By Product Type | By Ingredient Base | By Flavor Type | By Consumer Group | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 38% of the global gummy market in 2025, making it the leading regional market. The United States dominates regional demand due to strong nutraceutical consumption, high dietary supplement spending, and widespread adoption of functional wellness products. Immunity gummies, beauty supplements, and CBD gummies are particularly popular among adult consumers. Canada is also witnessing growing demand for vegan, sugar-free, and clean-label gummies as health-conscious purchasing behavior strengthens across retail and e-commerce channels. Strong innovation capabilities and premium product adoption continue to support regional market expansion.

Europe

Europe held nearly 27% market share in 2025, driven by strong demand from Germany, the United Kingdom, France, and Italy. Germany remains one of the largest nutraceutical gummy markets due to high healthcare awareness and strong adoption of preventive wellness products. The United Kingdom is witnessing significant growth in vegan gummies and sugar-reduced confectionery products due to increasing consumer focus on healthier lifestyles. Regulatory emphasis on clean-label ingredients and sugar reduction is encouraging innovation across the region. European consumers are also highly receptive to organic, non-GMO, and sustainable gummy products.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 12% during the forecast period. China leads regional demand due to increasing middle-class consumption, expanding e-commerce infrastructure, and rising health awareness among younger consumers. Japan and South Korea are major markets for collagen gummies, beauty supplements, and premium wellness products. India is emerging rapidly due to increasing urbanization, rising disposable incomes, and growing pediatric nutrition demand. Regional manufacturers are expanding affordable gummy supplement portfolios while global brands are investing heavily in localized production facilities and distribution partnerships.

Latin America

Latin America is witnessing steady growth led by Brazil and Mexico. Brazil represents the largest market within the region due to strong confectionery consumption and growing interest in functional nutritional supplements. Expanding retail modernization and online supplement sales are supporting greater accessibility to premium gummy products. Mexican consumers are increasingly adopting immunity and wellness gummies as healthcare awareness continues to improve. The region also benefits from rising demand for affordable nutritional products among younger populations.

Middle East & Africa

The Middle East & Africa region is experiencing increasing demand for halal-certified gummies and wellness supplements. Saudi Arabia and the UAE are emerging as important markets driven by rising healthcare expenditure, premium wellness consumption, and expanding retail infrastructure. South Africa is also becoming a regional nutraceutical manufacturing hub with growing export activity. Increasing urbanization, improving healthcare access, and expanding awareness regarding preventive nutrition are expected to support long-term market growth across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Gummy Market

- Haribo

- Mars Incorporated

- Mondelez International

- Nestlé

- Ferrara Candy Company

- Church & Dwight

- Bayer

- SmartyPants Vitamins

- Hero Nutritionals

- Nature’s Way

- YumEarth

- Procaps Group

- Amway

- H&H Group

- Sirio Pharma