Ground Meat Market Size

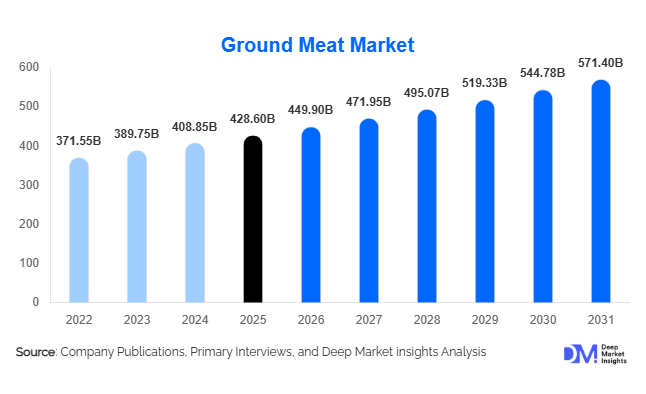

According to Deep Market Insights, the global ground meat market size was valued at USD 428.6 billion in 2025 and is projected to grow from USD 449.9 billion in 2026 to reach USD 571.4 billion by 2031, expanding at a CAGR of 4.9% during the forecast period (2026–2031). The market growth is primarily driven by rising global protein consumption, increasing demand for convenient and ready-to-cook meat formats, and expanding quick-service restaurant (QSR) penetration worldwide. Ground meat remains one of the most versatile and affordable protein formats, widely used across retail, foodservice, and processed food manufacturing applications.

Urbanization, dual-income households, and time-constrained lifestyles are accelerating demand for easy-to-prepare meal ingredients, positioning ground meat as a staple across developed and emerging economies. Growth is further supported by technological advancements in meat processing, cold chain infrastructure expansion, and improved packaging technologies extending product shelf life. Emerging markets across Asia-Pacific and Latin America are witnessing strong consumption growth due to rising disposable incomes and westernization of diets. Meanwhile, developed markets are shifting toward premium, organic, and antibiotic-free ground meat offerings, reflecting evolving consumer preferences toward quality and traceability.

Key Market Insights

- Ground beef remains the dominant product category, driven by global burger consumption and foodservice demand.

- Retail packaged ground meat sales are expanding rapidly due to growth in supermarkets and e-commerce grocery platforms.

- Asia-Pacific represents the fastest-growing consumption region, supported by rising protein intake and urbanization.

- Automation and advanced meat processing technologies are improving yield efficiency and cost competitiveness.

- Premiumization trends including organic, grass-fed, and clean-label meat products are gaining traction in developed economies.

- Cold chain investments across emerging markets are enabling wider distribution and reducing spoilage losses.

What are the latest trends in the ground meat market?

Shift Toward Value-Added and Premium Ground Meat

Consumers increasingly prefer differentiated meat products such as organic, hormone-free, grass-fed, and regionally sourced ground meat. Retailers are expanding premium private-label offerings, while processors invest in traceability technologies and transparent labeling. Premium ground meat commands higher margins and appeals to health-conscious consumers seeking quality assurance. This trend is particularly strong in North America and Europe, where sustainability certifications and animal welfare considerations influence purchasing decisions. Manufacturers are also introducing blended meat formats incorporating vegetables or alternative proteins to address sustainability concerns without compromising taste.

Expansion of Ready-to-Cook and Processed Applications

The growing popularity of ready meals, frozen foods, and convenience cooking solutions is boosting demand for standardized ground meat inputs. Food manufacturers increasingly rely on pre-seasoned and portion-controlled ground meat for meal kits, frozen entrees, and snack applications. Quick-service restaurants continue expanding globally, driving consistent demand for ground meat used in burgers, meatballs, sausages, and fillings. Automation in grinding and portioning processes ensures uniform quality and scalability, enabling processors to meet large-volume contracts efficiently.

What are the key drivers in the ground meat market?

Rising Global Protein Consumption

Increasing population growth and rising income levels are significantly boosting animal protein demand. Ground meat offers affordability compared to whole cuts, making it accessible across income groups. Rapid dietary transitions in Asia and Africa toward higher protein intake are accelerating consumption volumes, particularly for poultry and beef-based ground meat products.

Growth of Quick-Service Restaurants and Foodservice Chains

The global expansion of fast-food chains has strongly influenced ground meat demand. Burgers and processed meat products remain core menu items across international restaurant chains. Foodservice operators favor ground meat due to cost efficiency, versatility, and standardized cooking performance. The rapid rise of delivery platforms further amplifies prepared food consumption, indirectly driving processing volumes.

Advancements in Cold Chain and Packaging Technologies

Improved refrigeration logistics and modified atmosphere packaging (MAP) technologies have expanded shelf life and distribution reach. Emerging economies are investing heavily in refrigerated transport and storage infrastructure, enabling processors to penetrate semi-urban and rural markets. These developments reduce wastage while maintaining product safety standards.

What are the restraints for the global market?

Volatility in Livestock and Feed Prices

Fluctuating feed costs, climate impacts, and disease outbreaks create instability in raw material pricing. These cost pressures directly influence processor margins and retail pricing, leading to periodic demand fluctuations. Producers must increasingly adopt risk management strategies and supply diversification to maintain profitability.

Regulatory and Sustainability Pressures

Environmental concerns related to livestock emissions and stricter food safety regulations present ongoing challenges. Governments are implementing tighter standards around processing hygiene, traceability, and emissions reduction. Compliance increases operational costs, particularly for smaller processors lacking technological capabilities.

What are the key opportunities in the ground meat industry?

Emerging Market Consumption Growth

Rapid urban expansion across India, Southeast Asia, and Africa presents significant growth opportunities. Rising middle-class populations are increasing meat consumption frequency, while modern retail penetration improves accessibility. Companies investing early in localized processing facilities and distribution networks can capture long-term demand growth.

Technology Integration and Automation

Automation in meat grinding, sorting, and packaging improves operational efficiency while reducing contamination risks. AI-enabled quality monitoring and robotics enhance productivity and consistency. Technology adoption also supports traceability, allowing companies to meet regulatory requirements and consumer transparency expectations.

Expansion of Export-Oriented Processing

Export-driven production hubs in Brazil, the U.S., and Australia continue expanding capacity to serve international markets. Trade agreements and rising demand in import-dependent countries create opportunities for processors specializing in frozen ground meat exports. Export diversification reduces reliance on domestic demand cycles and stabilizes revenue streams.

Product Type Insights

The global ground meat market demonstrates strong diversification across product categories; however, ground beef continues to dominate overall consumption patterns, accounting for approximately 38% share of the global market in 2025. The leadership of ground beef is primarily driven by its deep integration into global food culture, particularly through burgers, meat-based ready meals, and foodservice menu standardization. Across North America and parts of Europe, beef-based products remain the backbone of quick-service restaurant menus, where consistency, flavor profile familiarity, and scalable processing capabilities make ground beef the preferred protein format. The expansion of international burger chains, combined with premium gourmet burger concepts and casual dining formats, continues to reinforce structural demand for ground beef globally.In addition to foodservice reliance, ground beef benefits from well-established livestock supply chains, efficient processing technologies, and widespread consumer acceptance across both developed and emerging economies. Advances in grinding technology, portion-controlled packaging, and modified atmosphere packaging have extended shelf life and enabled broader retail penetration. Furthermore, consumer preference for protein-rich diets and high satiety foods supports steady demand growth, particularly among younger demographics and urban consumers seeking convenient meal preparation solutions.Ground poultry represents the second-largest product category, accounting for nearly 29% of global market share, and is experiencing one of the fastest growth trajectories within the industry. This expansion is strongly supported by affordability advantages, lower production costs, and favorable health perceptions compared to red meat. Consumers increasingly associate poultry with lean protein intake, reduced fat content, and dietary flexibility, making ground chicken and turkey highly attractive in health-conscious markets. Rising inflationary pressures in several regions have further accelerated substitution from beef to poultry, particularly among middle-income households seeking cost-effective protein sources.Ground pork accounts for approximately 21% of global demand, maintaining strong regional dominance, particularly in East Asia and several European countries. Pork’s culinary adaptability across dumplings, sausages, meat fillings, and processed foods ensures stable consumption levels. In China and Southeast Asia, ground pork remains a staple protein embedded in traditional cuisine, driving consistent household and foodservice demand. European markets also rely heavily on pork-based ground meat for charcuterie production, regional sausages, and value-added meat preparations.Growth in this segment is supported by efficient hog farming systems and integrated processing operations that allow cost competitiveness and large-scale output. Additionally, innovation in seasoning technologies and regional flavor customization enhances product differentiation and premium positioning opportunities. Increasing adoption of traceability systems and animal welfare certifications across Europe is further strengthening consumer confidence in pork-based products.

Application Insights

Foodservice applications represent the largest demand segment, contributing nearly 42% of global ground meat consumption in 2025. The segment’s leadership is strongly linked to the rapid international expansion of quick-service restaurants (QSRs), casual dining chains, and delivery-focused restaurant models. Urbanization and rising disposable income levels have reshaped global eating habits, encouraging frequent dining outside the home and increasing dependence on standardized meat ingredients that enable consistent menu execution across large restaurant networks.Retail household consumption accounts for approximately 35% of total market demand, supported by the global expansion of packaged meat offerings and evolving home cooking behaviors. The COVID-era shift toward home meal preparation established lasting consumer habits centered on convenience cooking and meal planning. Consumers increasingly purchase pre-portioned ground meat products for quick recipes, batch cooking, and freezer storage. Improved packaging technologies, including vacuum sealing and resealable formats, have enhanced product freshness and reduced waste, encouraging higher retail adoption.Additionally, the growing popularity of online recipes, cooking tutorials, and social media food trends has elevated consumer experimentation with ground meat-based meals. Retailers continue to introduce flavored variants, organic options, and premium blends targeting differentiated consumer preferences. This segment benefits from rising demand among dual-income households seeking quick yet nutritious meal solutions.Processed food manufacturing contributes roughly 23% of global demand, supported by the strong expansion of frozen foods, ready meals, and protein-based snack categories. Food manufacturers increasingly incorporate ground meat into convenience-oriented products such as frozen pasta dishes, meat pies, dumplings, and breakfast items. The rapid growth of frozen food consumption in emerging economies, combined with increasing cold chain infrastructure investment, is enabling this segment to expand beyond traditionally mature markets.Innovation in processed foods, including high-protein snacks, microwaveable meals, and ready-to-eat formats, continues to drive industrial demand. Manufacturers favor ground meat due to its adaptability in shaping, seasoning absorption, and compatibility with automated production lines. The leading driver for the application segment remains the dominance of foodservice demand, supported by global restaurant expansion and changing consumer dining lifestyles.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global distribution channels, accounting for approximately 48% of market share. Their leadership is supported by extensive cold chain infrastructure, standardized food safety controls, and strong consumer trust in product quality and freshness. Large-format retail outlets provide consumers with wide product variety, competitive pricing, and convenient access to both fresh and frozen ground meat options. Retail chains increasingly invest in private-label meat brands, allowing them to offer competitive pricing while maintaining quality assurance.The growth of modern retail infrastructure across emerging economies has significantly strengthened this channel’s position. Urban consumers increasingly rely on organized retail environments where product traceability, hygiene standards, and refrigeration systems meet regulatory expectations. In-store butchery services and freshly ground meat counters also enhance customer engagement and reinforce perceptions of freshness.Online grocery and direct-to-consumer channels represent a rapidly expanding 20% share, supported by digital retail adoption and evolving consumer purchasing behavior. E-commerce platforms offer subscription-based meat delivery, customizable portion sizes, and farm-to-home traceability features that appeal to convenience-focused consumers. Growth in mobile commerce, digital payments, and last-mile cold delivery infrastructure has significantly accelerated adoption, particularly in urban Asia-Pacific markets.The increasing integration of omnichannel retail strategies, where consumers combine online ordering with offline pickup or delivery, is reshaping distribution dynamics. Retailers and meat processors are investing heavily in logistics optimization, insulated packaging solutions, and predictive demand analytics to ensure freshness and minimize spoilage. The leading driver within distribution channels remains supermarket dominance, supported by established cold chain networks and consumer purchasing confidence.

End-Use Insights

The quick-service restaurant industry represents the fastest-growing end-use segment, expanding at a rate exceeding 6% annually. Rising global fast-food consumption, driven by urban lifestyles and time-constrained consumers, has positioned QSRs as major purchasers of ground meat products. International franchise expansion into emerging economies has significantly increased demand for standardized meat supplies capable of maintaining taste consistency across regions.Ground meat’s adaptability enables QSR operators to innovate menus while maintaining operational efficiency. Burgers, wraps, meat bowls, and fusion cuisine concepts increasingly rely on ground meat formats that allow rapid preparation and scalable cooking processes. The proliferation of drive-through services and delivery-focused restaurant models further amplifies demand.Processed food manufacturers represent another critical end-use category as they expand production of frozen meals, protein snacks, and ready-to-eat foods. Industrial buyers increasingly prioritize consistent fat ratios, uniform grind textures, and extended shelf stability, encouraging processors to invest in advanced grinding and preservation technologies. Growth in convenience foods across Asia-Pacific and Latin America continues to strengthen industrial consumption patterns.Export-oriented processors benefit from rising meat imports across China, Japan, and Middle Eastern countries, where domestic production constraints increase reliance on international suppliers. Trade agreements, improved cold logistics, and standardized quality certifications facilitate cross-border meat flows and support industry globalization.Retail household demand continues expanding steadily as meal-prep culture gains popularity worldwide. Consumers increasingly prepare meals in advance to manage busy schedules, driving purchases of versatile ingredients like ground meat. Health-conscious households also favor controlled portion cooking, enabling customization of ingredients and nutritional content. The leading growth driver across end-use segments remains rapid expansion of quick-service restaurants combined with rising global convenience consumption patterns.

| By Product Type | By Processing Type | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 29% of the global ground meat market in 2025, making it one of the most mature and technologically advanced regions. The United States dominates regional consumption due to deeply rooted burger culture, high per-capita meat intake, and an extensive quick-service restaurant ecosystem. Advanced meat processing infrastructure, automation adoption, and integrated livestock supply chains enable large-scale production efficiency and consistent product quality.Regional growth is primarily driven by strong foodservice demand, premiumization trends, and innovation in value-added meat products. Consumers increasingly seek organic, grass-fed, and antibiotic-free ground meat options, encouraging processors to diversify product portfolios. The expansion of meal kits, ready-to-cook retail products, and online grocery platforms further supports market growth. Canada contributes stable demand through retail packaged meat consumption and export activity, supported by stringent quality standards and efficient cold logistics systems.Technological investments in traceability, blockchain-based supply monitoring, and sustainable processing practices are reshaping the competitive landscape. Additionally, rising consumer interest in protein-rich diets and convenience foods reinforces long-term demand stability across the region.

Europe

Europe represents nearly 24% of global market share, characterized by strong regulatory oversight, premium product positioning, and diverse culinary traditions. Germany, the United Kingdom, France, and Spain lead regional consumption, supported by both retail and foodservice demand. European consumers increasingly favor sustainably sourced and ethically produced meat, encouraging processors to adopt environmentally responsible production practices.Regional growth drivers include rising demand for premium ground meat products, expansion of private-label retail offerings, and modernization of meat processing facilities to comply with stringent food safety regulations. Innovation in packaging sustainability, reduced plastic usage, and carbon footprint transparency has become a key competitive differentiator. Additionally, traditional sausage and processed meat consumption continues to sustain steady demand for ground pork and blended meat products.The growing popularity of convenience meals and chilled ready-to-cook products across urban European households supports continued retail expansion. Government regulations promoting traceability and animal welfare standards also encourage industry consolidation and technological upgrades.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for approximately 27% of global demand. Rapid urbanization, rising middle-class populations, and changing dietary patterns are transforming protein consumption across the region. China leads regional demand due to widespread use of ground pork in traditional cuisine and processed foods, while India shows accelerating growth in poultry-based ground meat consumption driven by affordability and increasing protein awareness.Japan and South Korea maintain strong processed meat consumption supported by convenience food culture and advanced retail infrastructure. Expansion of modern supermarkets, cold storage capacity, and e-commerce grocery platforms has significantly improved product accessibility. Western-style dining trends and international restaurant chain expansion further stimulate demand for ground beef products in metropolitan areas.Regional growth is also driven by rising disposable incomes, increasing female workforce participation, and growing demand for ready-to-cook meals among urban consumers. Investments in domestic meat processing capacity and improvements in cold chain logistics continue to enhance supply reliability and market penetration.

Latin America

Latin America holds approximately 11% market share, with Brazil and Argentina serving as primary contributors. The region benefits from abundant livestock resources, strong agricultural infrastructure, and competitive export capabilities. Brazil functions both as a major consumer market and a global exporter of beef and poultry products, supporting steady industry expansion.Regional growth drivers include increasing urbanization, rising fast-food penetration, and expanding middle-class populations seeking affordable protein sources. Local cuisine traditions heavily incorporate ground meat into everyday meals, ensuring stable baseline consumption. Investments in meat processing modernization and export certification standards continue improving international trade opportunities.Growth in supermarket chains and cold storage facilities across urban centers enhances product accessibility, while regional trade agreements facilitate cross-border meat distribution within Latin America.

Middle East & Africa

The Middle East & Africa region accounts for nearly 9% of global demand, supported primarily by strong import dependence and expanding foodservice industries. Saudi Arabia, the United Arab Emirates, and South Africa lead regional consumption due to growing urban populations, tourism expansion, and rising hospitality investments.Regional growth is driven by increasing tourism activity, rapid development of hotel and restaurant infrastructure, and rising disposable incomes among younger populations. Limited domestic livestock production in several Middle Eastern countries increases reliance on imported ground meat, creating opportunities for global exporters. Halal-certified processing and strict quality standards play a critical role in shaping purchasing decisions.Urbanization and modernization of retail infrastructure across African markets are gradually improving cold chain availability, enabling broader market penetration. Expansion of international restaurant franchises and convenience food adoption continues to strengthen long-term demand prospects across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Ground Meat Market

- JBS S.A.

- Tyson Foods Inc.

- Cargill Incorporated

- WH Group Limited

- Marfrig Global Foods

- Hormel Foods Corporation

- BRF S.A.

- Perdue Farms

- Sanderson Farms

- OSI Group

- Maple Leaf Foods

- Minerva Foods

- Vion Food Group

- NH Foods Ltd.

- Danish Crown A/S