Greenhouse Horticulture Market Size

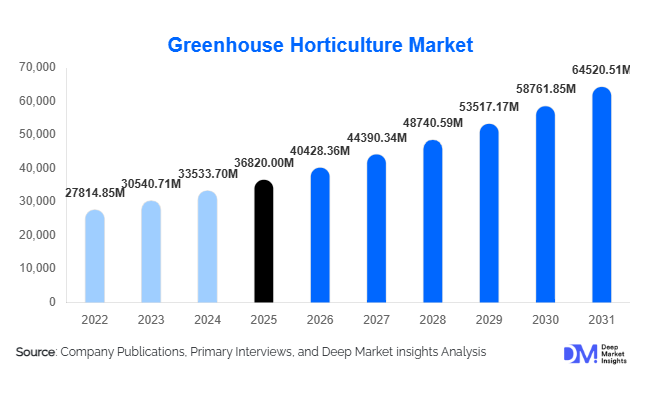

According to Deep Market Insights, the global greenhouse horticulture market size was valued at USD 36,820 million in 2025 and is projected to grow from USD 40,428.36 million in 2026 to reach USD 64,520.51 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The greenhouse horticulture market growth is primarily driven by increasing demand for year-round crop production, rising adoption of controlled environment agriculture (CEA), and growing pressure on conventional farming systems due to climate variability and land scarcity. Governments and commercial growers are increasingly investing in protected cultivation technologies to enhance productivity, reduce water consumption, and ensure consistent crop quality.

Key Market Insights

- Controlled environment agriculture is becoming mainstream, enabling predictable yields and reduced climate risk exposure.

- High-tech greenhouses integrating automation and AI monitoring systems are rapidly expanding across developed and emerging economies.

- Asia-Pacific dominates production capacity, supported by large-scale vegetable cultivation and government-backed modernization programs.

- Europe leads technological innovation, particularly in hydroponics, climate control systems, and energy-efficient greenhouse designs.

- Urban farming and vertical greenhouse integration are emerging as key growth themes in densely populated cities.

- Sustainability pressures, including water conservation and pesticide reduction, are accelerating greenhouse adoption globally.

What are the latest trends in the greenhouse horticulture market?

Shift Toward Smart and Automated Greenhouses

Greenhouse horticulture is rapidly transitioning toward digitalized production environments. Growers are deploying IoT-enabled sensors, automated irrigation systems, AI-based climate management platforms, and predictive analytics tools that optimize crop growth conditions in real time. Automated fertigation and remote monitoring technologies reduce labor dependency while improving yield consistency. Robotics for harvesting and crop inspection is gaining traction in high-value crops such as tomatoes, peppers, and strawberries. These smart systems allow growers to precisely manage temperature, humidity, CO₂ levels, and nutrient delivery, increasing productivity while minimizing resource wastage.

Expansion of Hydroponic and Soilless Cultivation

Hydroponics and other soilless cultivation methods are becoming central to greenhouse horticulture due to higher productivity per square meter and lower water usage compared to traditional farming. Growers are adopting nutrient film technique (NFT), deep water culture, and aeroponics systems to meet rising demand for pesticide-free produce. Retailers increasingly favor greenhouse-grown vegetables for their uniform quality and supply reliability. Urban agriculture initiatives are integrating hydroponic greenhouses within metropolitan areas, reducing transportation costs and supporting localized food systems.

What are the key drivers in the greenhouse horticulture market?

Rising Demand for Year-Round Food Supply

Population growth and urbanization are increasing pressure on agricultural systems to deliver consistent food supply throughout the year. Greenhouse horticulture enables off-season production regardless of climatic conditions, ensuring stable availability of vegetables, fruits, and ornamentals. Retail chains and foodservice providers increasingly rely on greenhouse producers to maintain uninterrupted supply contracts, driving investment in protected cultivation infrastructure.

Water Efficiency and Sustainability Requirements

Water scarcity and environmental regulations are encouraging adoption of greenhouse systems that use up to 70–90% less water than open-field agriculture. Recirculating irrigation systems and controlled nutrient application significantly reduce runoff and fertilizer losses. Governments promoting climate-resilient agriculture are offering subsidies for greenhouse construction, accelerating adoption in regions facing drought risks.

Growth of High-Value Crop Production

Greenhouse cultivation enables premium crop production with higher yields and improved quality standards. Tomatoes, cucumbers, berries, leafy greens, and floriculture products achieve superior uniformity and shelf life under protected conditions. Export-oriented producers increasingly rely on greenhouse horticulture to meet stringent quality and phytosanitary standards required by international markets.

What are the restraints for the global market?

High Initial Capital Investment

Establishing modern greenhouses requires substantial upfront investment in infrastructure, climate control systems, irrigation technologies, and automation equipment. Small-scale farmers often face financing constraints despite long-term productivity benefits. Energy-intensive operations further increase operational expenditure in colder climates.

Energy Consumption and Operational Complexity

Heating, cooling, and artificial lighting requirements raise energy costs, particularly in technologically advanced greenhouses. Skilled labor shortages and technical expertise requirements also create operational barriers, slowing adoption among traditional growers transitioning from open-field farming.

What are the key opportunities in the greenhouse horticulture industry?

Government-Supported Food Security Programs

Many countries are integrating greenhouse horticulture into national food security strategies to reduce dependence on imports and stabilize domestic food supply. Subsidies, low-interest loans, and infrastructure grants are encouraging growers to adopt protected cultivation. Emerging economies across Asia and the Middle East are prioritizing greenhouse expansion to overcome arable land limitations and harsh climatic conditions.

Urban and Vertical Greenhouse Farming

Urban population expansion is creating strong demand for localized fresh produce. Rooftop greenhouses and vertical farming-integrated greenhouse systems are emerging in megacities to shorten supply chains and reduce carbon emissions. Retailers and supermarkets increasingly partner with urban greenhouse operators for hyperlocal sourcing, creating new investment avenues.

Integration of Renewable Energy Solutions

Solar-powered climate control systems, geothermal heating, and energy-efficient glazing technologies present significant opportunities to reduce operational costs. Greenhouses powered by renewable energy sources are gaining investor interest as sustainability reporting becomes critical for agribusiness operations.

Product Type Insights

Plastic greenhouses continue to dominate the global greenhouse horticulture market, accounting for nearly 52% of the total market share in 2025, primarily due to their cost-effectiveness, structural flexibility, and adaptability across diverse climatic conditions. Their relatively low installation and maintenance costs make them highly attractive for growers in emerging economies transitioning from open-field cultivation to protected agriculture systems. Plastic film structures allow faster deployment cycles and scalable expansion, enabling commercial producers to respond quickly to rising food demand and seasonal variability. In addition, technological improvements in UV-resistant and multi-layer polyethylene films have significantly improved durability and crop protection, strengthening adoption among mid-scale and large commercial farms. While glass greenhouses maintain strong penetration in technologically advanced regions such as Europe, their higher capital investment limits adoption primarily to high-value crop cultivation requiring maximum light transmission and long-term operational stability. Glass structures are particularly favored in precision farming environments where automation, artificial lighting integration, and climate optimization are essential for premium crop production. Meanwhile, polycarbonate greenhouses are gaining increasing traction as an intermediate solution, combining insulation efficiency with structural durability. Their superior thermal retention reduces energy consumption in colder climates, supporting sustainability goals and lowering operational costs over time. Overall, plastic greenhouses remain the leading segment as they provide the optimal balance between affordability, productivity enhancement, and scalability, making them the preferred infrastructure choice for expanding global greenhouse cultivation.

Crop Type Insights

Vegetables represent the leading crop segment, contributing approximately 48% of total greenhouse horticulture revenue in 2025, supported by strong global consumption patterns and the growing need for year-round fresh produce supply. Tomatoes, cucumbers, bell peppers, and leafy greens dominate greenhouse cultivation due to predictable demand from supermarket chains, foodservice providers, and processing industries. The leading driver behind vegetable dominance lies in their shorter crop cycles, higher yield per square meter, and compatibility with controlled-environment agriculture technologies, allowing growers to maximize productivity and revenue consistency. Greenhouse vegetable production also enables reduced pesticide usage and improved quality uniformity, aligning with rising consumer preference for safe and traceable food products. Fruit cultivation, particularly strawberries, blueberries, and specialty berries, is expanding rapidly as growers leverage greenhouse systems to extend harvest seasons and protect delicate crops from climate variability. Floriculture continues to maintain stable demand supported by ornamental plant markets, landscaping industries, and event-driven consumption; however, vegetables remain the primary revenue generator due to large-scale commercial procurement and essential food supply requirements. Increasing urbanization, dietary shifts toward fresh and healthy foods, and growth in organized retail channels further reinforce vegetables as the dominant crop category within greenhouse horticulture.

Technology Insights

Hydroponic systems lead technological adoption, accounting for nearly 44% of greenhouse installations globally in 2025, driven by their ability to significantly enhance productivity while optimizing water and nutrient efficiency. The leading driver for hydroponics adoption is the growing pressure on arable land and freshwater resources, encouraging growers to adopt soil-less cultivation systems capable of delivering higher yields with lower environmental impact. Hydroponic cultivation minimizes soil-borne diseases, enables precise nutrient control, and allows consistent crop quality, making it highly suitable for commercial-scale greenhouse operations supplying retail and export markets. Alongside hydroponics, climate control automation technologies are witnessing rapid expansion, particularly across Europe and North America, where labor shortages and energy optimization requirements are accelerating digital transformation in agriculture. Advanced monitoring systems integrating sensors, artificial intelligence, and real-time analytics allow growers to regulate temperature, humidity, irrigation, and lighting conditions with precision, improving crop outcomes and operational efficiency. The integration of IoT-enabled platforms and predictive analytics further supports data-driven cultivation strategies, enabling greenhouse operators to reduce waste, enhance yield predictability, and improve profitability. As sustainability and resource efficiency become central priorities globally, technology adoption continues to reshape greenhouse horticulture into a highly controlled and technologically advanced agricultural model.

Structure Type Insights

Standalone greenhouses hold the largest market share, representing approximately 61% of the global greenhouse horticulture market, primarily due to their ease of installation, operational flexibility, and suitability across farms of varying sizes. The leading driver supporting this segment is the ability of standalone structures to serve both smallholder farmers and large commercial growers without requiring complex infrastructure integration. These structures allow phased expansion, enabling growers to scale production gradually based on market demand and investment capacity. In contrast, multi-span greenhouse structures are increasingly adopted by commercial enterprises seeking economies of scale, improved space utilization, and centralized climate management systems. Multi-span facilities enhance productivity through uniform environmental control and reduced energy loss across larger cultivation areas. Rooftop and urban-integrated greenhouse formats, although currently niche, are emerging rapidly in densely populated metropolitan regions where proximity to consumers reduces transportation costs and carbon emissions. Urban agriculture initiatives and smart-city development strategies are expected to support long-term growth of these innovative greenhouse formats, particularly as cities seek sustainable local food production solutions.

End-Use Insights

Commercial growers dominate the greenhouse horticulture market, accounting for nearly 67% of total market share in 2025, driven primarily by large-scale production contracts with supermarkets, food distributors, and export buyers. The leading growth driver for this segment is the increasing demand for consistent, high-quality produce supplied throughout the year regardless of seasonal constraints. Commercial greenhouse operators benefit from economies of scale, advanced technologies, and integrated supply chains that enable predictable output and standardized quality levels. Research institutions and agricultural universities represent smaller but strategically significant segments, contributing to innovations in seed genetics, climate optimization, and sustainable cultivation practices. Nurseries also play a critical role in supplying seedlings and young plants for greenhouse production systems, supporting industry expansion through improved crop propagation techniques.

End-Use Industry Analysis

The food retail and fresh produce supply chain remains the primary end-use industry driving greenhouse horticulture demand worldwide. Supermarkets increasingly prioritize consistent product availability, standardized appearance, and reduced pesticide residues, encouraging growers to transition toward controlled-environment agriculture. Rising consumer awareness regarding food safety and sustainability has strengthened retailer preference for greenhouse-grown vegetables, which offer improved traceability and quality assurance. The expansion of organized retail networks and e-commerce grocery platforms further accelerates demand for reliable year-round supply. Food processing industries are also increasing procurement of greenhouse-grown tomatoes, peppers, and specialty vegetables due to uniform size, predictable yields, and processing efficiency advantages. Export-oriented greenhouse production is expanding rapidly, particularly supplying European and Middle Eastern markets from Asia and North Africa, supported by improved cold-chain logistics and trade integration. Emerging applications are extending beyond food production, including pharmaceutical-grade plant cultivation, functional foods, and nutraceutical crop production within controlled environments, creating diversified revenue opportunities and strengthening the long-term commercial viability of greenhouse horticulture investments.

| By Structure Type | By Crop Type | By Technology | By End Use | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 41% of the global greenhouse horticulture market in 2025, making it the largest regional market driven by rapid population growth, rising food demand, and government-backed agricultural modernization programs. China leads regional production capacity through extensive deployment of cost-efficient plastic greenhouses supporting large-scale vegetable cultivation and domestic food security objectives. India is experiencing accelerated adoption supported by subsidy programs, protected farming initiatives, and increasing farmer awareness of yield optimization under climate variability conditions. Japan and South Korea emphasize technologically advanced greenhouse systems, driven by aging agricultural workforces and labor shortages that encourage automation and robotics integration. Urbanization, rising middle-class consumption, and increasing demand for pesticide-free produce continue to fuel regional expansion, while improvements in irrigation infrastructure and climate-resilient farming policies further strengthen greenhouse investments across the region.

Europe

Europe holds nearly 29% of global market share, characterized by advanced technological adoption and strong regulatory support for sustainable agriculture. The Netherlands serves as a global innovation hub for high-tech greenhouse systems, combining automation, artificial lighting, and energy-efficient cultivation practices to achieve some of the highest productivity levels worldwide. Spain plays a critical role as a major exporter of greenhouse vegetables across European Union markets, benefiting from favorable climatic conditions and well-established logistics networks. Increasing environmental regulations, carbon reduction targets, and water conservation policies are driving investment in energy-efficient glass greenhouses and precision climate management technologies. Consumer preference for locally grown, sustainably produced food further accelerates greenhouse adoption across France, Italy, and Northern Europe.

North America

North America demonstrates strong growth momentum across the United States and Canada, supported by rising demand for locally produced fresh food and efforts to reduce dependence on imported vegetables. Controlled environment agriculture investments are expanding near major urban consumption centers, enabling shorter supply chains and fresher produce delivery. Technological innovation, venture capital funding, and the emergence of large commercial greenhouse operators are transforming regional agricultural production models. Increasing climate unpredictability and water management concerns are also encouraging growers to adopt greenhouse systems that ensure production stability and resource efficiency.

Middle East & Africa

The Middle East represents one of the fastest-growing greenhouse horticulture markets, particularly in the United Arab Emirates and Saudi Arabia, where food security strategies and limited arable land drive adoption of controlled cultivation systems. Harsh climatic conditions and water scarcity have accelerated investment in advanced greenhouse technologies incorporating desalination-supported irrigation, climate cooling systems, and hydroponic cultivation. Israel continues to serve as a global technology innovator, contributing advanced irrigation solutions, fertigation systems, and greenhouse engineering expertise adopted worldwide. Across Africa, greenhouse adoption is gradually expanding as governments and development organizations promote modern farming practices to improve food production efficiency and export competitiveness.

Latin America

Latin America is witnessing steady expansion led by Mexico, Brazil, and Chile, supported by favorable climatic conditions and strong export-oriented agricultural industries. Mexico benefits significantly from proximity to North American markets, enabling greenhouse vegetable exports that meet stringent quality standards required by international retailers. Brazil is increasingly adopting greenhouse cultivation to stabilize production against climate variability and improve productivity in high-value crops. Chile focuses heavily on greenhouse fruit cultivation for global export markets, leveraging controlled environments to extend growing seasons and enhance crop quality. Increasing foreign investment, improvements in agricultural infrastructure, and expanding trade agreements continue to strengthen greenhouse horticulture development across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Greenhouse Horticulture Market

- Richel Group

- Netafim Ltd.

- Certhon

- Priva Holding B.V.

- Argus Control Systems Ltd.

- Rough Brothers Inc.

- Luiten Greenhouses

- Dalsem Greenhouse Projects

- Van der Hoeven Horticultural Projects

- Harnois Greenhouses

- Lumigrow Inc.

- Svensson Group

- Agra Tech Inc.

- GreenTech Agro LLC

- Top Greenhouses Ltd.