Green Tea Extract Supplements Market Size

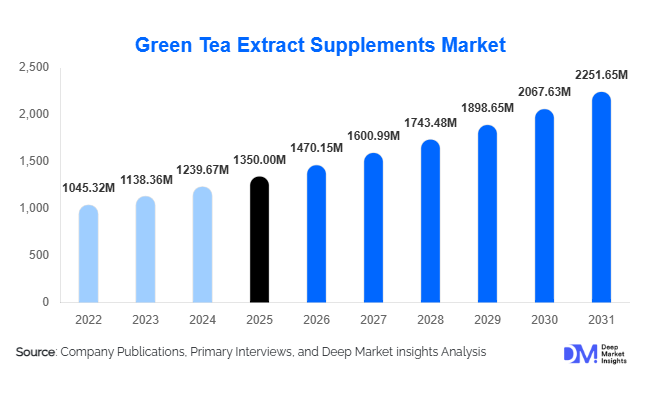

According to Deep Market Insights,the global green tea extract supplements market size was valued at USD 1,350 million in 2025 and is projected to grow from USD 1,470.15 million in 2026 to reach USD 2,251.65 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing consumer focus on weight management, preventive healthcare, and plant-based antioxidant supplements, along with rising awareness of the health benefits of EGCG-rich green tea extracts and online retail adoption.

Key Market Insights

- Capsules and tablets dominate the product format, due to their convenience, precise dosage, and extended shelf life, making them the preferred choice globally.

- Standardized EGCG extracts (≥50%) lead the extract type segment, driven by clinical evidence supporting weight management, cardiovascular health, and antioxidant benefits.

- Weight management applications account for the largest share, with consumers seeking natural solutions for fat metabolism and thermogenesis.

- Online retail channels are expanding rapidly, fueled by subscription models, e-commerce platforms, and influencer-driven marketing campaigns.

- Asia-Pacific is emerging as the fastest-growing region, led by China and India, supported by growing middle-class populations, rising disposable incomes, and expanding awareness of herbal wellness supplements.

- Technological adoption, including advanced extraction methods, microencapsulation, and improved bioavailability formulations, is enhancing product efficacy and market competitiveness.

What are the latest trends in the green tea extract supplements market?

Premiumization Through Standardized and Clinically Backed Extracts

Manufacturers are increasingly offering high-EGCG standardized extracts and bioavailability-enhanced formulations. Clinical validation of catechin content and antioxidant potency is helping brands differentiate themselves, enabling premium pricing and consumer trust. Microencapsulation and liposomal delivery technologies are being adopted to improve stability, absorption, and efficacy, particularly for weight management and cardiovascular health applications.

Expansion into Functional Foods, Beverages, and Cosmeceuticals

Green tea extracts are no longer limited to capsules and tablets. The ingredient is increasingly incorporated into fortified beverages, protein bars, metabolism-boosting supplements, and skincare products. Cosmeceutical applications leverage the antioxidant and anti-aging properties of catechins, opening new revenue streams beyond traditional nutraceutical formats. Cross-industry integration strengthens brand visibility and attracts new consumer demographics seeking multifunctional health benefits.

What are the key drivers in the green tea extract supplements market?

Rising Obesity and Metabolic Syndrome Prevalence

Global health concerns around obesity, diabetes, and metabolic disorders are fueling demand for natural weight management solutions. Green tea extract supplements, especially EGCG-rich formulations, are clinically associated with fat oxidation and thermogenesis, making them a preferred choice among health-conscious consumers and fitness enthusiasts. Programs integrating supplementation with lifestyle interventions further boost adoption rates.

Growing Preference for Plant-Based and Clean-Label Products

Consumers increasingly favor herbal, organic, and decaffeinated formulations over synthetic alternatives. This trend has led to higher demand for organic-certified green tea extracts, decaffeinated options, and full-spectrum botanical extracts. Clean-label positioning and transparency in ingredient sourcing are emerging as key factors influencing purchase decisions, particularly in North America and Europe.

Increased Awareness of Cardiovascular and Immune Health Benefits

EGCG and polyphenols in green tea extracts support vascular health, reduce inflammation, and enhance antioxidant defense. As preventive healthcare becomes a priority, middle-aged and elderly consumers are driving growth in antioxidant-focused supplement applications. Health campaigns emphasizing natural, plant-derived bioactives are reinforcing market adoption.

What are the restraints for the global market?

Regulatory Scrutiny on Health Claims and Safety

Strict regulations around labeling, dosage, and health claims pose challenges for manufacturers. Excessive EGCG intake may cause liver toxicity, requiring careful dosage monitoring and compliance with regional regulatory bodies. These factors increase operational costs and complexity for product development and marketing.

Volatility in Raw Material Supply and Prices

Green tea leaf harvests in China, India, and Japan are susceptible to climatic fluctuations, impacting catechin yields and extract availability. Supply chain disruptions and price volatility can affect manufacturing costs and market pricing, limiting profitability for manufacturers reliant on consistent high-quality raw material.

What are the key opportunities in the green tea extract supplements market?

Digital and Direct-to-Consumer Expansion

The surge in e-commerce and subscription-based models presents significant opportunities. Brands can reach global consumers directly, offer personalized formulations, and gather data-driven insights on consumption patterns. Emerging markets such as India, Brazil, and Southeast Asia show double-digit growth in online nutraceutical adoption, representing untapped potential for international companies.

Integration into Multi-Industry Products

Green tea extracts are increasingly incorporated into functional foods, beverages, and cosmeceuticals. This cross-industry application diversifies revenue streams and broadens market reach beyond traditional capsules and tablets. Anti-aging skincare, metabolic drinks, and protein supplements represent lucrative segments with growing consumer acceptance.

Premiumization Through Evidence-Based Formulations

Consumer demand is shifting toward clinically validated products. Companies that invest in clinical trials, high-potency EGCG extracts, and bioavailability-enhanced formulations can capture higher margins and establish brand authority. Regulatory clarity and scientific validation create barriers to entry, benefiting established players and innovative newcomers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1350 Million |

| Market Size in 2026 | USD 1470.15 Million |

| Market Size in 2031 | USD 2251.65 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Capsules continue to dominate the global market due to their precise dosing, convenience, long shelf life, and superior stability of active ingredients. Tablets remain a significant segment but face competition from capsules because of slower absorption and gastrointestinal considerations. Liquid extracts and softgels serve niche audiences prioritizing rapid bioavailability and targeted health benefits, while functional gummies are emerging as a preferred format among younger consumers, offering palatability, ease of consumption, and innovative flavor experiences. The growth of capsules and softgels is further supported by rising demand for standardized and clinically validated EGCG formulations.

Application Insights

Weight management is the leading application, fueled by EGCG's thermogenic and metabolism-enhancing properties and the global surge in obesity and lifestyle-related disorders. Antioxidant and immunity support applications are experiencing steady growth, particularly for cardiovascular health, anti-aging, and cellular protection benefits. Emerging applications in sports nutrition and cognitive health are gaining traction, driven by fitness enthusiasts seeking performance optimization and the aging population seeking preventive cognitive support. The overall growth across applications is further propelled by increasing consumer awareness of proactive wellness and preventive healthcare solutions.

Distribution Channel Insights

Online retail channels dominate the market due to the convenience of home delivery, availability of subscription-based models, and influence of digital marketing and social media campaigns. Pharmacies and drug stores continue to hold relevance, offering credibility, brand trust, and point-of-sale engagement. Supermarkets, specialty health stores, and direct-to-consumer models are increasingly integrating e-commerce capabilities, allowing brands to combine offline credibility with online reach, while also offering personalized and loyalty-based programs to retain consumers.

Consumer Demographic Insights

Adults aged 18–45 are the primary drivers of demand, motivated by proactive wellness, fitness trends, and interest in preventive health. Middle-aged and elderly consumers (46+ years) are increasingly adopting supplements for cardiovascular health, immune support, and chronic disease prevention. Sports and fitness enthusiasts prioritize performance-enhancing and recovery-focused formulations, while women-focused products emphasizing weight management, skin health, and holistic wellness are gaining significant traction. Overall, consumer interest is increasingly shifting toward clinically validated, natural, and sustainable product offerings.

Explore more data points, trends and opportunities Download Free Sample Report

Green Tea Extract Supplements Market Segmentations

By Product Type

- Capsules

- Tablets

- Powder

- Liquid Extracts

- Softgels

- Functional Gummies

By Extract Type

- Standardized EGCG Extract

- Polyphenol-Rich Extract

- Decaffeinated Green Tea Extract

- Organic Certified Green Tea Extract

- Full-Spectrum Green Tea Extract

By Application / Health Benefit

- Weight Management

- Antioxidant & Immunity Support

- Cardiovascular Health

- Cognitive & Brain Health

- Skin & Anti-Aging

- Sports Nutrition & Metabolic Energy

By Distribution Channel

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Online Retail

- Direct-to-Consumer / Subscription Models

By End-User / Consumer Demographic

- Adults (18–45 Years)

- Middle-Aged & Geriatric (46+ Years)

- Sports & Fitness Consumers

- Women-Focused Formulations

- Clinical / Practitioner-Recommended

Regional Insights

North America

North America accounts for approximately 32% of the 2025 market, with the United States as the primary contributor. Growth is driven by strong preventive healthcare awareness, high disposable incomes, advanced healthcare infrastructure, and established e-commerce platforms. Consumers increasingly favor premium, standardized EGCG extracts, while regulatory support for dietary supplements ensures product safety and efficacy. The adoption of online retail, coupled with wellness-focused lifestyle trends and fitness-conscious populations, further propels regional growth.

Europe

Europe represents around 22% of the market in 2025, led by Germany, the U.K., and France. Growth is supported by high consumer health awareness, stringent regulatory frameworks, and demand for clinically validated and organic extracts. Western Europe shows particular preference for eco-conscious and sustainable formulations, while the increasing prevalence of lifestyle-related diseases encourages adoption of weight management and antioxidant products. Expansion of pharmacy-led distribution, alongside e-commerce integration, is enhancing market reach and consumer accessibility.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing market, contributing approximately 36% of the 2025 share. China leads in production capacity, while India demonstrates rapid consumption growth due to rising online retail adoption, urbanization, and increased awareness of herbal wellness solutions. Japan’s mature market emphasizes quality, safety, and standardized extracts. The regional surge is driven by a combination of rising disposable incomes, urban health-conscious populations, expanding e-commerce penetration, and growing interest in preventive healthcare, weight management, and immunity-boosting formulations.

Latin America

Latin America, led by Brazil, Mexico, and Argentina, is an emerging market with increasing potential. Growth is primarily fueled by urban, affluent consumers who prioritize weight management, antioxidant, and immunity support supplements. Rising awareness of lifestyle-related health concerns, expansion of modern retail channels, and gradual adoption of e-commerce platforms are supporting market development. Local product customization and marketing campaigns targeting younger, health-conscious populations are further enhancing adoption rates.

Middle East & Africa

The Middle East, spearheaded by the UAE and Saudi Arabia, is witnessing steady growth due to high-income populations, rising preventive health awareness, and rapid adoption of online retail channels. Africa remains predominantly a production hub but is experiencing gradual demand growth in urban centers, driven by increasing healthcare awareness, expansion of modern retail infrastructure, and rising interest in functional wellness products. Premiumization trends and the adoption of natural, standardized supplements are expected to further drive market expansion across the region.

Key Players in the Green Tea Extract Supplements Market

- Amway

- Herbalife Nutrition

- NOW Foods

- Nature’s Way

- GNC Holdings

- Swanson Health

- Blackmores

- Jamieson Wellness

- Nature’s Bounty

- Life Extension

- Himalaya Wellness

- DSM Nutritional Products

- Indena S.p.A.

- Taiyo International

- NutraScience Labs