Greek Yogurt Market Size

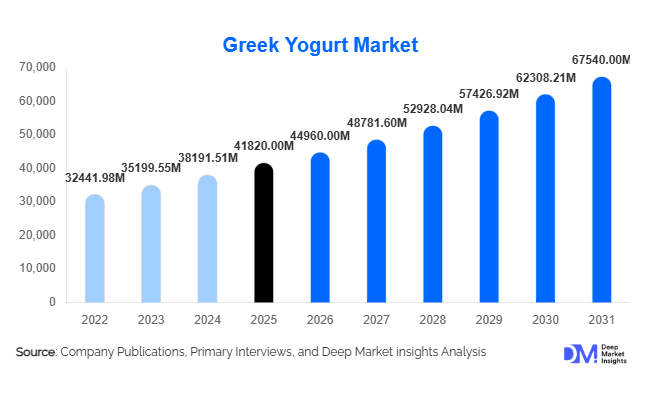

According to Deep Market Insights, the global Greek yogurt market size was valued at USD 41,820 million in 2025 and is projected to grow from USD 44,960 million in 2026 to reach USD 67,540 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer preference for high-protein dairy products, increasing awareness of gut health and probiotics, and the global shift toward functional and clean-label foods. Greek yogurt has evolved from a niche Mediterranean dairy product into a mainstream health-oriented snack and meal replacement category across developed and emerging economies.

Demand expansion is supported by changing dietary patterns favoring protein-rich breakfasts, convenient on-the-go nutrition, and reduced sugar consumption. Manufacturers are increasingly launching lactose-free, plant-blended, and fortified Greek yogurt variants targeting fitness enthusiasts, aging populations, and flexitarian consumers. Retail modernization, e-commerce grocery penetration, and refrigerated logistics improvements are also enabling wider accessibility across Asia-Pacific and Latin America. Innovation in flavors, texture enhancement, and packaging formats such as drinkable yogurt and multipacks is further expanding consumer adoption. Additionally, premiumization trends and private-label growth across supermarkets are intensifying competition while improving affordability, accelerating market penetration globally.

Key Market Insights

- High-protein functional foods trend continues to position Greek yogurt as a leading healthy dairy alternative worldwide.

- North America dominates global consumption due to mature dairy innovation ecosystems and strong fitness-oriented consumer behavior.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and Western dietary adoption.

- Clean-label and low-sugar formulations are becoming primary product differentiation strategies.

- Private-label expansion is reshaping pricing structures and improving affordability in retail channels.

- Technology adoption in fermentation and cold-chain logistics is improving shelf life and export viability.

What are the latest trends in the Greek yogurt market?

Protein-Enriched and Functional Nutrition Expansion

Greek yogurt is increasingly positioned within functional nutrition rather than traditional dairy consumption. Consumers seek products supporting digestion, immunity, muscle recovery, and weight management. Manufacturers are incorporating probiotics, prebiotics, collagen peptides, vitamins, and omega-3 ingredients into formulations. High-protein snack culture, particularly among millennials and Gen Z consumers, has expanded Greek yogurt usage beyond breakfast into post-workout and meal replacement occasions. Brands are also introducing hybrid dairy products combining yogurt with cereals, seeds, and fruit inclusions to enhance nutritional value and convenience.

Flavor Innovation and Premiumization

Flavor diversification is reshaping consumer engagement globally. Exotic fruits, regional flavors, dessert-inspired variants, and reduced-sugar formulations are gaining traction. Premium Greek yogurt products featuring organic milk, grass-fed sourcing, and artisanal fermentation methods are attracting health-conscious urban consumers willing to pay higher prices. Premiumization has enabled companies to improve margins despite rising dairy input costs. Packaging innovation such as resealable cups and drinkable formats is improving convenience and expanding consumption occasions.

What are the key drivers in the Greek yogurt market?

Growing Health and Wellness Awareness

Consumers increasingly associate Greek yogurt with digestive health, protein intake, and weight management benefits. Rising obesity concerns and lifestyle diseases are pushing consumers toward nutrient-dense foods. Diet trends such as keto, high-protein, and low-carb eating patterns strongly favor Greek yogurt consumption. Healthcare professionals and nutrition influencers further amplify demand through digital platforms, strengthening category penetration globally.

Expansion of Organized Retail and Cold Chain Infrastructure

Modern supermarkets, hypermarkets, and online grocery platforms have significantly improved product availability. Investments in refrigeration logistics enable manufacturers to penetrate emerging markets where dairy distribution was previously limited. Improved shelf stability and packaging innovation are supporting cross-border trade growth.

Product Innovation and Diversification

Continuous innovation in lactose-free, vegan-blended, and fortified Greek yogurt products attracts broader consumer segments including lactose-intolerant and plant-forward consumers. Companies are expanding drinkable yogurt formats and snack-sized packaging, encouraging impulse purchases and higher consumption frequency.

What are the restraints for the global market?

High Production and Raw Milk Costs

Greek yogurt production requires higher milk input compared to regular yogurt due to straining processes, resulting in elevated production costs. Fluctuating milk prices and energy costs directly impact manufacturer profit margins and retail pricing competitiveness.

Cold Chain Dependence and Shelf-Life Limitations

The need for continuous refrigeration increases logistics expenses and limits penetration in rural or infrastructure-constrained markets. Supply disruptions or inadequate cold storage can lead to product losses, acting as a growth constraint in developing regions.

What are the key opportunities in the Greek yogurt industry?

Emerging Market Expansion

Asia-Pacific, Middle East, and Latin America present significant untapped opportunities due to rising disposable income and increasing adoption of Western dietary habits. Urban consumers in India, China, Brazil, and Southeast Asia are rapidly adopting protein-rich snacks, creating strong demand potential for localized Greek yogurt flavors and affordable packaging formats.

Plant-Dairy Hybrid Innovation

Hybrid yogurt formulations combining dairy proteins with plant ingredients such as oats, almonds, or coconut offer new growth avenues. These products appeal to flexitarian consumers seeking sustainability without fully abandoning dairy nutrition. Such innovations also help manufacturers differentiate products in competitive markets.

Foodservice and Institutional Demand

Greek yogurt usage is expanding into cafés, quick-service restaurants, bakery fillings, smoothies, and healthy desserts. Foodservice partnerships enable bulk sales volumes and brand visibility, especially in urban markets where healthy menu offerings are expanding rapidly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 41820 Million |

| Market Size in 2026 | USD 44960 Million |

| Market Size in 2031 | USD 67540 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global Greek yogurt market demonstrates strong diversification across product types, with plain Greek yogurt continuing to dominate overall consumption patterns. In 2025, plain Greek yogurt accounts for approximately 38% of the global market, primarily due to its broad functional versatility across both household and commercial applications. Consumers increasingly prefer plain variants because they serve as a flexible base ingredient for breakfast bowls, smoothies, savory recipes, sauces, and high-protein meal preparation. The rise of fitness-oriented lifestyles and protein-forward dietary habits has significantly reinforced demand, as plain Greek yogurt offers high protein content without added sugars or artificial ingredients. Health-conscious consumers, particularly millennials and Gen Z populations, are gravitating toward minimally processed foods, further strengthening this segment’s leadership position.Lactose-free Greek yogurt represents one of the fastest-growing product categories globally, driven by rising awareness of lactose intolerance and digestive health concerns. Advances in dairy enzyme processing technologies have enabled manufacturers to maintain traditional taste and texture while improving digestibility. This segment is gaining traction not only among lactose-intolerant consumers but also among wellness-focused individuals seeking gut-friendly alternatives. The expansion of functional dairy products, combined with probiotic fortification and digestive wellness marketing, is expected to sustain accelerated growth for lactose-free variants throughout the forecast period.

Fat Content Insights

By fat content, low-fat Greek yogurt leads the global market with nearly 42% market share, reflecting the widespread adoption of calorie-conscious eating habits and balanced nutrition approaches. Consumers increasingly seek foods that deliver high protein with moderate caloric intake, positioning low-fat Greek yogurt as an ideal daily consumption product. Healthcare awareness campaigns addressing obesity, cardiovascular health, and metabolic wellness have reinforced demand across both developed and emerging economies. Additionally, low-fat variants maintain a favorable balance between taste and nutritional perception, enabling strong acceptance across diverse demographic groups.Non-fat Greek yogurt continues to maintain a significant consumer base, particularly among weight-management and fitness-focused populations. The segment remains highly popular in North America and parts of Europe, where structured diet programs and calorie tracking practices remain prevalent. Innovations such as improved texture stabilization, protein enhancement, and natural sweetening solutions have helped address historical taste challenges associated with non-fat formulations. As a result, manufacturers are successfully retaining health-conscious consumers while improving repeat purchase rates.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 55% of global market share. Their leadership is primarily driven by extensive refrigeration infrastructure, strong brand visibility, and the ability to offer a wide assortment of product varieties under one roof. Consumers benefit from product comparison, promotional pricing, and access to both global brands and private-label alternatives. Retail chains increasingly allocate premium shelf space to high-protein dairy products, recognizing Greek yogurt as a high-growth category that drives frequent store visits.Online retail represents the fastest-growing distribution channel globally, supported by rapid digital transformation in grocery purchasing behavior. The proliferation of e-commerce platforms, quick-commerce delivery services, and subscription-based grocery models has significantly improved access to refrigerated dairy products. Consumers increasingly value home delivery convenience, recurring purchase automation, and broader product selection unavailable in physical stores. Digital platforms also allow brands to communicate nutritional benefits directly to consumers, strengthening brand engagement and personalization strategies.

End-Use Insights

Household consumption dominates the Greek yogurt market, accounting for nearly 70% of total demand, supported by its integration into daily eating routines. Greek yogurt has evolved from a niche dairy product into a staple food consumed across breakfast, snacks, desserts, and meal preparation occasions. Rising awareness of protein intake, digestive wellness, and functional nutrition has encouraged regular household consumption across age groups. Parents increasingly select Greek yogurt as a healthier alternative to sugary snacks for children, further expanding adoption within family households.The foodservice sector is witnessing rapid expansion as cafés, quick-service restaurants, bakeries, and health-focused eateries incorporate Greek yogurt into diversified menus. Smoothie bowls, parfaits, frozen yogurt desserts, salad dressings, and protein-rich breakfast offerings are driving institutional demand. Foodservice operators value Greek yogurt for its versatility, extended shelf life relative to fresh dairy products, and ability to align menus with wellness-oriented consumer expectations. Growth in café culture, particularly across urban Asia-Pacific and North America, continues to create new commercial consumption opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Greek Yogurt Market Segmentations

By Product Type

- Plain Greek Yogurt

- Flavored Greek Yogurt

- Organic Greek Yogurt

- Lactose-Free Greek Yogurt

- Drinkable Greek Yogurt

By Fat Content

- Full-Fat Greek Yogurt

- Low-Fat Greek Yogurt

- Non-Fat Greek Yogurt

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Food Stores

- Foodservice & HoReCa

By End Use

- Household Consumption

- Foodservice Industry

- Institutional Buyers

Regional Insights

North America

North America accounted for approximately 36% of the global Greek yogurt market in 2025, maintaining its leadership position due to mature consumer awareness and strong product innovation ecosystems. The United States represents the largest contributor, where high-protein dietary trends, fitness culture, and widespread adoption of functional foods sustain consistent demand growth. Consumers increasingly replace traditional breakfast foods with protein-rich alternatives, positioning Greek yogurt as a convenient and nutritionally dense option.Regional growth is further supported by continuous innovation from leading dairy brands introducing probiotic-enhanced formulations, reduced-sugar varieties, and plant-dairy hybrid products. Retail penetration remains exceptionally high due to advanced cold-chain logistics and widespread supermarket networks. Private-label expansion by major retail chains has also improved price accessibility, broadening consumer reach. In Canada, demand growth is driven by premium organic offerings, sustainability-focused packaging initiatives, and increasing interest in locally sourced dairy products. Rising multicultural populations and evolving dietary preferences continue to diversify flavor innovation across the region.

Europe

Europe holds nearly 29% market share, supported by deeply rooted yogurt consumption traditions and strong dairy heritage. Countries such as Greece, Germany, the United Kingdom, and France represent key markets where yogurt consumption is already embedded within daily dietary habits. Authenticity and product origin play a crucial role in purchasing decisions, with consumers placing high value on traditional production methods and regional dairy sourcing.Regional growth is driven by increasing demand for premium and organic dairy products, supported by stringent food quality regulations and consumer trust in European dairy standards. Health-conscious consumers are increasingly adopting high-protein diets, reinforcing Greek yogurt’s positioning as a functional food. Additionally, sustainability initiatives across European markets are encouraging manufacturers to adopt recyclable packaging, carbon-reduction strategies, and ethical sourcing practices. Expansion of lactose-free and plant-blended yogurt options is also supporting category diversification, attracting flexitarian consumers seeking digestive-friendly alternatives.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, fueled by rapid urbanization, expanding middle-class populations, and rising awareness of Western dietary patterns. Countries such as China, India, Japan, and Australia are experiencing accelerated adoption as consumers increasingly prioritize health, convenience, and premium nutrition. Greek yogurt is gaining popularity as a modern, aspirational food associated with fitness and wellness lifestyles.Regional growth drivers include expanding modern retail infrastructure, increasing refrigeration penetration, and aggressive marketing by multinational dairy companies introducing localized flavors tailored to regional taste preferences. In India, double-digit growth is supported by rapid expansion of organized retail, e-commerce grocery platforms, and increasing protein awareness among younger consumers. In China and Japan, functional foods and digestive health trends are encouraging demand for probiotic-rich dairy products. Australia’s strong dairy production capabilities and premium export positioning further contribute to regional market expansion.

Latin America

Latin America is emerging as a promising growth region led by Brazil and Mexico, where improving economic conditions and rising disposable incomes are enabling greater adoption of premium dairy products. Consumers are increasingly shifting toward healthier snack alternatives, creating opportunities for Greek yogurt manufacturers to expand market presence. Urbanization and modernization of retail channels have significantly improved product availability across metropolitan areas.Regional growth is also supported by increasing awareness of protein-rich diets and growing participation in fitness activities. Manufacturers are introducing smaller, affordable packaging formats to attract price-sensitive consumers while maintaining premium product positioning. Partnerships between local dairy producers and international brands are accelerating technology transfer and product innovation, further strengthening market penetration.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth driven by rising disposable incomes, expanding expatriate populations, and increasing demand for premium dairy products. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are leading adoption due to strong retail infrastructure and exposure to global food trends. Greek yogurt aligns well with regional dietary preferences emphasizing dairy consumption and high-protein nutrition.Growth drivers include expanding modern supermarket chains, increasing health awareness campaigns, and rising demand for convenient yet nutritious food options among urban consumers. The hospitality and foodservice sectors play a significant role in market expansion, particularly through hotel breakfasts, café menus, and wellness-focused dining concepts. Additionally, younger demographics across the region are increasingly influenced by global health trends promoted through social media, accelerating acceptance of functional dairy products. Investments in cold-chain logistics and local dairy processing facilities are expected to further improve accessibility and sustain long-term regional growth.

Key Players in the Greek Yogurt Market

- Nestlé S.A.

- Danone S.A.

- General Mills Inc.

- Chobani LLC

- Lactalis Group

- FAGE International S.A.

- Arla Foods amba

- Müller Group

- Yeo Valley Organic

- Stonyfield Farm Inc.

- Meiji Holdings Co., Ltd.

- Morinaga Milk Industry Co., Ltd.

- China Mengniu Dairy Company Limited

- Bright Dairy & Food Co., Ltd.

- Parmalat S.p.A.