Grape Juice Concentrate Market Size

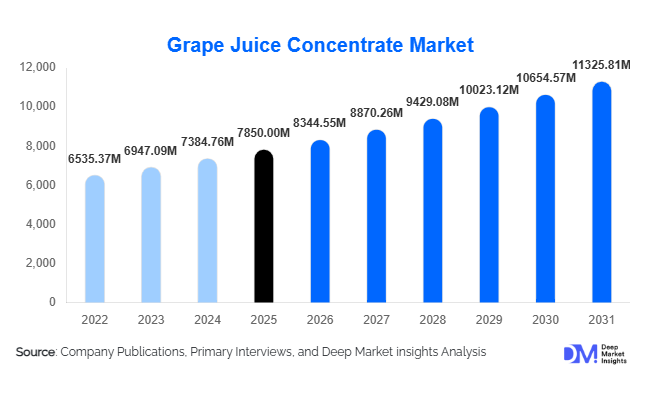

According to Deep Market Insights,the global grape juice concentrate market size was valued at USD 7,850 million in 2026 and is projected to grow from USD 8,344.55 million in 2026 to reach USD 11,325.81 million by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The market growth is primarily driven by increasing health-conscious consumption, rising demand for natural and functional beverages, and the growing application of grape juice concentrates across food processing, nutraceuticals, and cosmetic industries.

Key Market Insights

- Pure and organic grape juice concentrates are gaining popularity, driven by consumer preference for minimally processed, nutrient-rich products.

- The beverage industry dominates demand, particularly in juices, smoothies, and functional drinks, accounting for a significant share of global consumption.

- North America remains a key consumer region, with the U.S. and Canada leading adoption of natural and functional juice products.

- Asia-Pacific is the fastest-growing region, driven by rising urbanization, disposable income, and increasing health awareness in countries like China and India.

- Technological adoption in concentration methods, such as vacuum evaporation and membrane filtration, is enhancing quality, shelf life, and color retention.

- Export opportunities are expanding in Europe and the Middle East, supporting global growth and international supply chains.

What are the latest trends in the grape juice concentrate market?

Shift Toward Organic and Functional Products

Consumers increasingly prefer organic grape juice concentrates due to their health benefits, minimal processing, and absence of synthetic additives. This trend is driving manufacturers to expand organic product lines and label transparency. Functional variants enriched with antioxidants, polyphenols, and vitamins are gaining traction, catering to the growing demand for immunity-boosting and anti-aging beverages. Health-conscious millennials and Gen Z consumers are especially fueling demand for these fortified, high-quality concentrates.

Industrial and Foodservice Integration

Grape juice concentrates are being widely adopted in food and beverage manufacturing for beverages, confectioneries, jams, sauces, and bakery products. Industrial usage is increasing due to the convenience of long shelf life, concentrated flavor, and nutritional benefits. Foodservice operators are also adopting bag-in-box and bulk concentrates to reduce costs, enhance consistency, and improve menu variety. This trend has contributed to stronger B2B demand alongside traditional retail consumption.

What are the key drivers in the grape juice concentrate market?

Rising Health Awareness

Consumers are increasingly recognizing the benefits of grape-derived antioxidants such as resveratrol. This awareness is driving the adoption of natural, nutrient-dense beverages, boosting demand for pure and organic grape juice concentrates globally. Functional applications in nutraceuticals, wellness drinks, and fortified foods further amplify growth.

Growth of Food & Beverage Industry

The global food and beverage industry is expanding, particularly in processed and functional beverages. Grape juice concentrates are used as natural sweeteners, flavor enhancers, and functional ingredients in soft drinks, smoothies, jams, and bakery items. This broad applicability ensures sustained demand from industrial and retail customers.

Technological Advancements

Advanced processing methods, such as vacuum evaporation, membrane filtration, and flash concentration, have improved flavor retention, color stability, and shelf life of grape juice concentrates. Technology adoption enables manufacturers to deliver consistent, high-quality products that meet regulatory standards and consumer expectations.

What are the restraints for the global market?

Volatility in Raw Material Prices

Grape availability is seasonal, and prices can fluctuate due to weather conditions, pest infestations, or supply chain disruptions. This volatility affects manufacturing costs, profitability, and pricing strategies.

Regulatory Compliance Challenges

Strict food safety standards and regulations in North America, Europe, and APAC increase operational complexity. Compliance with these regulations requires investment in quality control, certifications, and testing, which may limit market entry for smaller producers.

What are the key opportunities in the grape juice concentrate market?

Emerging Markets Expansion

Emerging economies such as China, India, Brazil, and Mexico present significant growth opportunities due to increasing disposable incomes, urbanization, and health-focused consumption. Localized flavors, small-format packaging, and competitive pricing can help manufacturers penetrate these markets effectively.

Integration into Functional Foods & Nutraceuticals

Grape juice concentrates’ antioxidant properties make them ideal for functional foods, dietary supplements, and health-oriented beverages. Collaborations with nutraceutical companies or introducing fortified products can drive additional revenue streams and differentiate offerings in the market.

Government Support and Export Growth

Policies such as “Make in India” and other regional incentives encourage local production and quality improvements. Simultaneously, growing export demand from Europe, North America, and the Middle East allows manufacturers to strengthen global supply chains, maximize revenue, and diversify market exposure.

Product Type Insights

100% pure grape juice concentrate continues to dominate the global market, accounting for approximately 45% of consumption in 2025. Its strong preference is fueled by increasing consumer demand for natural, minimally processed, and antioxidant-rich products. Health-conscious consumers are actively seeking products that provide functional benefits without added sugars or artificial ingredients. Blended grape juice concentrates, combining multiple fruit varieties, and organic grape juice concentrates are gaining traction, particularly among niche health-focused and gourmet segments. The rising interest in organic and plant-based diets further supports growth in these emerging categories, creating opportunities for product diversification and premium positioning.

Application Insights

The beverage sector remains the largest end-use segment for grape juice concentrate, representing nearly 50% of global demand. Its applications span juices, smoothies, functional drinks, and soft drinks, driven by consumers’ preference for naturally fortified beverages and immunity-boosting ingredients. The food processing industry, including bakery products, jams, sauces, and confectionery, is witnessing rapid adoption due to the concentrate’s natural flavoring and preservative properties. Nutraceutical and cosmetic applications are also emerging, leveraging grape extracts’ antioxidant and anti-aging properties. Export-driven demand from North America and Europe enhances opportunities for manufacturers targeting industrial and retail buyers, while innovation in functional and fortified beverages continues to fuel application growth.

Distribution Channel Insights

Supermarkets and hypermarkets dominate retail sales due to convenience, accessibility, and the ability to offer bulk packaging. Online retail is growing rapidly, especially for niche organic, premium, and functional products, driven by the expansion of e-commerce platforms and direct-to-consumer models. Industrial and foodservice channels remain critical for B2B demand, with bag-in-box and bulk concentrate formats preferred for cost efficiency, operational convenience, and consistent quality. Subscription models and specialized e-commerce channels targeting younger, health-conscious consumers are gaining momentum, further diversifying distribution strategies and enhancing market reach.

End-Use Insights

Beverages continue to represent the largest end-use industry for grape juice concentrate, benefiting from the rising consumption of functional and ready-to-drink products. Food processing applications, including bakery, confectionery, sauces, and jams, are expanding rapidly due to the demand for natural flavors and clean-label ingredients. Nutraceutical applications are growing particularly in Asia-Pacific and Latin America, driven by health awareness and aging populations seeking antioxidant-rich solutions. The wine industry continues to rely on grape juice concentrate as a key raw material, while cosmetic and personal care applications are emerging globally. Export-driven demand from North America, Europe, and the Middle East is further strengthening overall market growth, with manufacturers leveraging high-quality concentrate as a versatile ingredient across industries.

| By Product Type | By Packaging Type | By Distribution Channel | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

The United States dominates the North American market, holding approximately 20% of global share in 2025. Growth is driven by high health awareness, increasing functional beverage consumption, and consumer preference for clean-label and organic products. Canada demonstrates steady adoption, particularly in organic and specialty juice products, supported by rising disposable income and evolving consumer lifestyles. The presence of advanced processing technologies and strong retail infrastructure further reinforces regional market expansion.

Europe

Germany and France account for nearly 30% of Europe’s market share in 2025. Growth is supported by established grape cultivation, high per-capita consumption, and extensive use of grape concentrates in the food and beverage industry. Consumer preference for premium and functional beverages, coupled with strong export capabilities and adherence to stringent food safety standards, positions Europe as a stable and mature market. Emerging trends such as organic and sustainable sourcing are also influencing product innovation and regional growth.

Asia-Pacific

China and India are the fastest-growing markets in Asia-Pacific, registering a CAGR of approximately 7.5%. Urbanization, rising disposable incomes, and increasing health awareness are the primary growth drivers. Consumers are gravitating toward natural, functional, and fortified beverages, while manufacturers are investing in local production to meet demand. Japan and South Korea maintain steady demand for premium and functional beverage products, supported by an aging population and preference for antioxidant-rich juices. Expansion of modern retail chains and online platforms further facilitates market penetration in the region.

Latin America

Brazil and Argentina dominate regional consumption, driven by strong domestic beverage processing industries and significant grape cultivation. Increasing outbound export activity, coupled with rising investment in cold storage and processing infrastructure, supports market growth. Health-conscious consumers are adopting natural and minimally processed products, while beverage manufacturers are innovating with blended and functional grape juice concentrates to cater to evolving preferences. The region also benefits from proximity to key export markets, enhancing trade opportunities.

Middle East & Africa

Africa remains a vital production hub, with South Africa serving as a key supplier of high-quality grape juice concentrates. The Middle East, led by the UAE and Saudi Arabia, is emerging as a consumer market due to high-income populations, growing health awareness, and a strong preference for imported concentrates. Increasing investments in cold chain infrastructure, modern retail expansion, and rising demand for functional beverages are driving growth. The region’s focus on premium and organic products further strengthens market opportunities for global manufacturers.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Grape Juice Concentrate Market

- Concord Foods Inc.

- Welch's

- Glanbia PLC

- Del Monte Foods, Inc.

- Fruit of the Loom, Inc.

- Sunraysia Natural Foods

- Frutarom Industries Ltd.

- Parle Agro Pvt. Ltd.

- Mondelez International, Inc.

- Ocean Spray Cranberries, Inc.

- California Natural Products

- Schreiber Foods, Inc.

- Greenyard NV

- ADM (Archer Daniels Midland Company)

- Olam International