Gluten Free Food Market Size

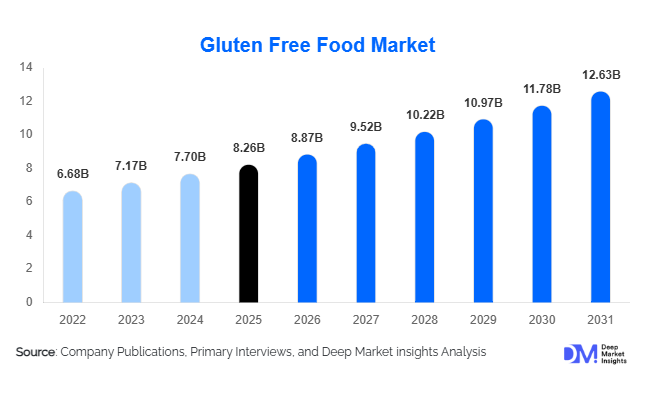

According to Deep Market Insights, the global gluten free food market size was valued at USD 8.26 billion in 2025 and is projected to grow from USD 8.87 billion in 2026 to reach USD 12.63 billion by 2031, expanding at a CAGR of 7.34% during the forecast period (2026–2031). The gluten free food market growth is primarily driven by rising awareness of gluten intolerance and celiac disease, increasing adoption of clean-label dietary habits, and expanding consumer preference for digestive-health-focused food products. Once considered a niche medical diet category, gluten-free foods have evolved into a mainstream wellness segment supported by product innovation, improved taste profiles, and expanding retail availability worldwide.

Key Market Insights

- Gluten-free diets are transitioning from medical necessity to lifestyle adoption, significantly expanding the consumer base beyond diagnosed patients.

- Bakery products dominate global demand, as manufacturers continue improving texture and taste through alternative grain innovation.

- North America leads market consumption, supported by strong labeling regulations and high consumer awareness.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and increasing health consciousness.

- Online retail and specialty health stores are reshaping distribution, improving accessibility and product discovery.

- Functional nutrition integration, including high-protein and fiber-enriched gluten-free foods, is driving premium product innovation.

What are the latest trends in the gluten free food market?

Functional and Nutrient-Enriched Gluten-Free Products

Manufacturers are increasingly developing gluten-free foods that deliver additional health benefits beyond allergen avoidance. Products enriched with plant proteins, probiotics, fiber, and ancient grains are gaining traction among wellness-focused consumers. Functional positioning allows brands to command premium pricing while appealing to sports nutrition consumers and health-conscious millennials. Innovations using chickpea flour, quinoa, millet, and sorghum are improving nutritional density while maintaining desirable taste and texture characteristics. This shift toward multifunctional foods is transforming gluten-free products into everyday dietary staples rather than specialty alternatives.

Expansion of Clean-Label and Natural Ingredient Formulations

Consumers increasingly prefer products with transparent ingredient lists and minimal processing. Gluten-free foods align strongly with clean-label trends, encouraging manufacturers to eliminate artificial additives and preservatives. Brands are investing in natural stabilizers, fermentation techniques, and enzyme technologies to improve shelf stability without compromising labeling claims. Retailers are also expanding private-label gluten-free portfolios, making products more accessible and affordable while strengthening consumer trust in certified labeling standards.

What are the key drivers in the gluten free food market?

Growing Health Awareness and Digestive Wellness Trends

Rising consumer awareness of digestive health and food sensitivities is a major growth driver. Increasing diagnosis of celiac disease and gluten intolerance, combined with preventive dietary adoption, has broadened the demand base globally. Consumers increasingly associate gluten-free foods with improved gut health, weight management, and reduced inflammation, encouraging routine consumption even among non-medical users.

Product Innovation and Improved Sensory Quality

Technological advances in flour blending, hydrocolloids, and processing techniques have significantly enhanced the taste and texture of gluten-free foods. Manufacturers now replicate wheat-like elasticity and softness, enabling gluten-free bakery and snack products to compete directly with conventional offerings. Continuous innovation has improved repeat purchase rates and reduced consumer resistance historically associated with gluten-free alternatives.

What are the restraints for the global market?

Premium Pricing and Cost Sensitivity

Gluten-free foods remain more expensive than traditional products due to specialized ingredients, certification requirements, and segregated manufacturing processes. Price premiums ranging from 30% to over 100% limit adoption in price-sensitive markets, particularly across developing economies. Scaling production efficiencies remains critical to long-term affordability.

Supply Chain and Cross-Contamination Risks

Maintaining gluten-free certification requires strict supply chain controls and dedicated production environments. Cross-contamination risks increase operational complexity and compliance costs, posing challenges for smaller manufacturers entering the market. Regulatory variations across regions further complicate global standardization efforts.

What are the key opportunities in the gluten free food industry?

Emerging Market Expansion

Rapid urbanization and increasing health awareness across Asia-Pacific and Latin America present significant opportunities for gluten-free food manufacturers. Countries such as India, China, and Brazil are witnessing growing adoption of wellness diets supported by expanding modern retail infrastructure. Local grain utilization, including millet and sorghum, enables cost-efficient product development tailored to regional dietary preferences.

Foodservice and Institutional Adoption

Restaurants, airlines, hospitals, and educational institutions are increasingly incorporating gluten-free meal options to accommodate dietary requirements. Standardized allergen management practices are enabling large-scale procurement contracts, creating stable demand channels for manufacturers. Foodservice expansion is expected to become a key growth contributor over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.26 Billion |

| Market Size in 2026 | USD 8.87 Billion |

| Market Size in 2031 | USD 12.63 Billion |

| CAGR | 7.34% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The gluten-free bakery products segment continues to dominate the global gluten-free food market, accounting for nearly 34% of total market share in 2025. The strong performance of this segment is primarily driven by the essential role bakery items play in daily diets, where gluten-free alternatives serve as direct substitutes for traditional wheat-based staples. Products such as bread, cookies, cakes, muffins, and pizza bases remain highly consumed due to their convenience and familiarity among consumers transitioning to gluten-free lifestyles. Continuous advancements in ingredient science, including improved alternative flour blends derived from rice, almond, sorghum, and millet, alongside enhanced fermentation and enzyme technologies, have significantly improved product texture, taste, and shelf stability. These improvements have reduced historical barriers related to dryness and poor structure, thereby accelerating consumer acceptance and repeat purchases.Snacks and ready-to-eat gluten-free products represent the fastest-growing product category, driven by evolving consumption patterns characterized by busy lifestyles and increased demand for convenient yet health-oriented food options. Manufacturers are increasingly introducing protein-enriched and fiber-fortified snack variants to align with functional nutrition trends. Gluten-free pasta and cereals are also witnessing steady expansion as brands diversify portfolios and introduce nutrient-enhanced formulations targeting wellness-focused and preventive-health consumers. Innovation in fortified grains, clean-label formulations, and plant-based ingredient integration is further strengthening growth across product categories while expanding appeal beyond medically required diets.

Application Insights

Household retail consumption remains the leading application segment, contributing approximately 57% of global demand. The dominance of this segment is largely driven by increasing consumer awareness regarding digestive health, food sensitivities, and lifestyle-driven dietary choices. The expansion of organized retail, improved product accessibility, and wider availability of certified gluten-free labels have encouraged consumers to incorporate gluten-free foods into everyday meal preparation. Growth in home cooking trends and personalized nutrition habits has further reinforced retail consumption patterns globally.Foodservice applications are experiencing rapid growth as restaurants, cafés, and quick-service restaurant chains increasingly introduce allergen-friendly menus to attract health-conscious consumers and accommodate dietary restrictions. The expansion of gluten-free menu labeling and cross-contamination management practices has strengthened consumer trust in dining establishments. Industrial food processing companies are also emerging as key contributors to market demand, integrating gluten-free ingredients into packaged meals, frozen foods, sauces, and snack products to meet rising consumer expectations for inclusive food options. Institutional catering services, including hospitals, schools, and airline meal providers, are evolving into stable demand contributors due to regulatory dietary accommodation requirements and growing global travel and healthcare service utilization.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global distribution channels, accounting for nearly 41% market share, supported by strong consumer confidence in standardized product labeling, extensive shelf visibility, and the availability of diverse product portfolios under one roof. Large retail chains also benefit from established supplier networks and private-label gluten-free product development, enabling competitive pricing and wider consumer penetration.Online retail represents the fastest-growing distribution channel, driven by digital grocery adoption, subscription-based purchasing models, and direct-to-consumer strategies adopted by emerging gluten-free brands. E-commerce platforms enable access to niche and specialty dietary products that may not be widely available in physical stores, particularly in developing markets. Specialty health and wellness stores continue to maintain relevance by attracting premium consumers seeking curated product selections, expert recommendations, and personalized dietary solutions. Additionally, foodservice distribution networks are expanding as bulk procurement of certified gluten-free ingredients increases among restaurants and institutional buyers, further strengthening supply chain integration.

Consumer Type Insights

Lifestyle consumers represent the largest consumer segment, accounting for approximately 46% of total market demand in 2025. The leadership of this segment is driven by the growing perception of gluten-free diets as part of broader wellness, weight management, and clean-eating lifestyles rather than solely medical necessity. Social media influence, fitness culture expansion, and increasing awareness of digestive health have encouraged voluntary dietary adoption among mainstream consumers, significantly expanding the addressable market.Medically diagnosed consumers, including individuals with celiac disease and gluten intolerance, continue to provide a stable and recurring demand base, ensuring consistent product consumption regardless of economic fluctuations. Sports nutrition and functional diet consumers are emerging rapidly as manufacturers introduce high-protein, low-inflammatory, and performance-oriented gluten-free products aligned with athletic and active lifestyles. The pediatric and family nutrition segment is also expanding as parents increasingly prioritize allergen-safe and easily digestible food options for children, supported by rising diagnosis rates of food sensitivities and growing awareness of preventive nutrition.

Explore more data points, trends and opportunities Download Free Sample Report

Gluten Free Food Market Segmentations

By Product Type

- Gluten-Free Bakery Products

- Gluten-Free Snacks & Ready-to-Eat Foods

- Gluten-Free Pasta & Noodles

- Gluten-Free Cereals & Breakfast Products

- Gluten-Free Flour & Baking Mixes

- Gluten-Free Dairy Alternatives & Frozen Foods

By Application

- Household Retail Consumption

- Foodservice & Restaurants

- Industrial Food Processing

- Institutional Catering

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail & Direct-to-Consumer

- Specialty Health & Organic Stores

- Convenience Stores

- Foodservice & Wholesale Distribution

By Consumer Type

- Medically Diagnosed Consumers

- Lifestyle & Wellness Consumers

- Sports Nutrition Consumers

- Pediatric & Family Nutrition Segment

Regional Insights

North America

North America holds the largest share of the gluten-free food market, accounting for approximately 38% of global demand in 2025. The United States remains the primary growth engine due to high consumer awareness, strong purchasing power, and well-established regulatory frameworks governing allergen labeling and food safety standards. Advanced retail infrastructure, widespread product availability, and strong participation from multinational food manufacturers continue to support market maturity. Regional growth is further driven by increasing adoption of wellness-focused diets, strong innovation pipelines from food companies, expansion of private-label gluten-free offerings, and growing demand for functional and clean-label foods. Canada contributes steady growth supported by healthcare-driven dietary awareness, rising diagnosis rates of gluten intolerance, and high per capita spending on premium specialty foods.

Europe

Europe accounts for nearly 31% of global market share, supported by strong consumption across Italy, Germany, the United Kingdom, and France. The region benefits from well-established healthcare awareness programs and government support initiatives for individuals with celiac disease, particularly reimbursement schemes in countries such as Italy that encourage regular consumption of certified gluten-free products. Regional growth is further driven by strong consumer preference for organic, natural, and clean-label foods, which aligns closely with gluten-free product positioning. Continuous innovation in artisanal bakery alternatives, premium product formulations, and sustainable packaging solutions also strengthens market expansion. Increasing vegan and plant-based dietary trends across Europe further complement gluten-free product adoption.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, projected to expand at a CAGR exceeding 13% during the forecast period. Growth is supported by rapid urbanization, rising disposable incomes, and increasing awareness of lifestyle-related health issues across emerging economies such as India and China. Expansion of modern retail infrastructure and e-commerce grocery platforms is significantly improving product accessibility. Traditional gluten-free grains including rice, millet, and sorghum provide a natural foundation for localized product innovation, enabling cost-effective manufacturing and culturally relevant product development. Australia and Japan represent relatively mature markets characterized by strong health awareness and premium product adoption, while Southeast Asian markets are witnessing increasing demand driven by younger consumer demographics and Western dietary influences.

Latin America

Latin America is experiencing gradual but consistent adoption of gluten-free foods, led by Brazil and Mexico. Increasing urbanization and rising middle-class populations are encouraging dietary diversification and greater spending on health-oriented products. Regional growth is supported by expanding supermarket penetration, improved product labeling awareness, and strategic expansion by multinational food brands introducing localized gluten-free offerings. Growing interest in wellness diets and preventive healthcare practices among urban consumers is further accelerating demand, while regional manufacturers are increasingly investing in product innovation using locally sourced grains.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market, particularly in the United Arab Emirates and South Africa, where premium retail environments and high dependence on imported specialty foods drive consumption. Increasing expatriate populations with established dietary preferences are contributing significantly to market demand. Regional growth is further supported by expansion of modern grocery retail formats, rising health awareness, and increasing availability of certified gluten-free products through international retail chains. Improvements in healthcare diagnostics related to food sensitivities and growing consumer exposure to global wellness trends are expected to gradually strengthen long-term market penetration across the region.

Key Players in the Gluten Free Food Market

- General Mills Inc.

- Kellogg Company

- Nestlé S.A.

- The Kraft Heinz Company

- Conagra Brands Inc.

- Dr. Schär AG

- The Hain Celestial Group Inc.

- Mondelez International Inc.

- PepsiCo Inc.

- Barilla Group

- Bob’s Red Mill Natural Foods

- Amy’s Kitchen Inc.

- Hero Group

- Freedom Foods Group Ltd.

- Enjoy Life Foods