Gluten-Free Coating Premix Market Size

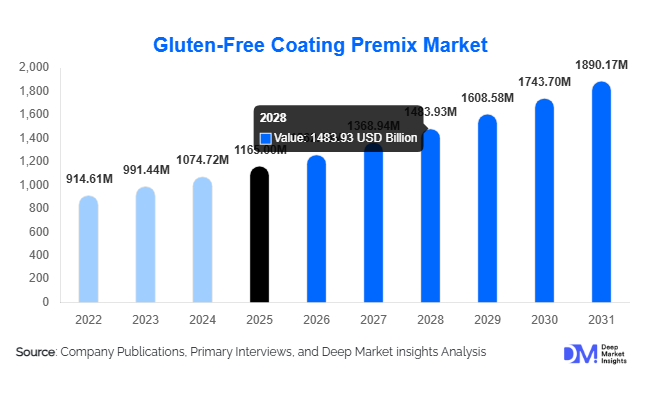

According to Deep Market Insights, the global gluten-free coating premix market size was valued at USD 1,165 million in 2025 and is projected to grow from USD 1,262.86 million in 2026 to reach USD 1,890.17 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). Market growth is primarily driven by rising gluten intolerance awareness, increasing demand for allergen-free processed foods, and rapid expansion of plant-based and coated convenience food categories. Food manufacturers across North America and Europe are actively reformulating products to meet gluten-free certification standards, while Asia-Pacific is emerging as a strong export-driven production hub for coated poultry and seafood products. Advancements in rice, chickpea, and multi-grain premix formulations are improving texture, adhesion, and oil absorption control, further accelerating industrial adoption.

Key Market Insights

- Meat & poultry applications dominate, accounting for over 40% of total market demand due to strong consumption of coated chicken and frozen fried products.

- Rice-based premixes lead the flour base segment, supported by cost efficiency, neutral flavor profile, and global availability.

- North America holds the largest market share, driven by high gluten-free product penetration and strict allergen labeling standards.

- Asia-Pacific is the fastest-growing region, supported by export-oriented food processing industries in China, India, and Thailand.

- Direct B2B sales dominate distribution, reflecting long-term procurement contracts between ingredient manufacturers and food processors.

- Plant-based protein coatings are emerging as a high-growth niche, requiring customized gluten-free adhesion systems.

What are the latest trends in the gluten-free coating premix market?

Rise of Clean-Label & Multi-Grain Functional Blends

Manufacturers are increasingly shifting toward clean-label formulations that exclude artificial additives while maintaining functional performance. Multi-grain blends incorporating sorghum, millet, quinoa, and chickpea flour are gaining traction for their nutritional positioning and improved crisp retention. Food processors are demanding shorter ingredient lists, non-GMO certifications, and allergen-segregated production facilities. This trend is particularly strong in North America and Western Europe, where consumers closely scrutinize ingredient transparency. Functional starch blends and hydrocolloids are also being optimized to replicate gluten’s binding properties, improving freeze-thaw stability and post-frying texture.

Growth of Plant-Based & Export-Oriented Coated Foods

The rapid growth of plant-based meat alternatives is reshaping coating premix innovation. Plant protein products require enhanced adhesion and flavor masking, creating demand for customized gluten-free batter and breading systems. Additionally, Asia-Pacific food processors are expanding gluten-free certified production lines to meet export requirements from the U.S. and Europe. Coated shrimp, chicken nuggets, and ready-to-fry snacks manufactured in Thailand, India, and China are increasingly supplied to Western retail markets, strengthening cross-border ingredient demand.

What are the key drivers in the gluten-free coating premix market?

Increasing Gluten Sensitivity & Lifestyle Diet Adoption

Growing awareness of celiac disease and non-celiac gluten sensitivity has expanded the consumer base for gluten-free foods. Beyond medically diagnosed cases, lifestyle-driven gluten avoidance is increasing among health-conscious consumers. Retail brands and QSR chains are reformulating coated food products to cater to this expanding demographic, supporting sustained ingredient demand.

Expansion of Quick-Service Restaurants (QSRs)

Global expansion of fried chicken chains, seafood restaurants, and snack-focused QSRs is fueling large-scale procurement of standardized gluten-free batter systems. Emerging markets are witnessing rapid outlet expansion, particularly in Asia and the Middle East, boosting ingredient volume consumption. QSR operators increasingly require certified allergen-free premixes to reduce cross-contamination risks.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuating prices of rice, pulses, and specialty grains directly impact production costs. Chickpea and quinoa-based formulations carry higher input costs compared to conventional wheat systems, compressing margins for manufacturers.

Performance Limitations Compared to Wheat-Based Systems

Gluten-free coatings may lack elasticity and binding strength, requiring advanced formulation technologies to match wheat-based textures. Continuous R&D investments are necessary to ensure adhesion, crispness, and shelf stability.

What are the key opportunities in the gluten-free coating premix industry?

Plant-Based Protein Coating Systems

Alternative protein producers require advanced gluten-free coating technologies that enhance mouthfeel and structural integrity. Customized premixes tailored to soy, pea, and mycoprotein applications present strong long-term revenue potential.

Export-Driven Manufacturing Partnerships

Asia-Pacific exporters producing gluten-free coated seafood and poultry for Western markets represent a significant growth avenue. Ingredient suppliers forming long-term contracts with export-oriented processors can capitalize on rising global trade in value-added frozen foods.

Product Type Insights

Breading & crumb premixes dominate the global gluten-free coating ingredients market, accounting for approximately 34% of the 2025 market share. The segment’s leadership is primarily driven by the rapid expansion of frozen ready-to-cook poultry and seafood products, where consistent texture, adhesion, and crispness are critical quality parameters. Food manufacturers increasingly prefer standardized premix solutions to ensure uniform coating performance, extended shelf stability, and optimized oil absorption during frying.

Tempura premixes and seasoned coating systems are witnessing steady growth, supported by the globalization of Asian-style cuisine across North America and Europe. The rising popularity of crispy shrimp, tempura vegetables, and fusion fast-food products has accelerated demand for light-textured batters. Meanwhile, custom functional coating blends are emerging as premium offerings, enabling manufacturers to tailor attributes such as crunch retention, flavor release, moisture control, and reduced oil uptake. These value-added functional systems are gaining traction among premium frozen food brands and QSR chains seeking product differentiation.

Application Insights

Meat & poultry applications hold the largest share at 41% of the 2025 global market, driven by high global consumption of breaded chicken nuggets, fillets, patties, and wings. The leading driver for this segment is the sustained demand for convenience-based protein products, particularly in quick-service restaurants and retail frozen aisles. Additionally, gluten-free reformulation initiatives among mainstream brands are further supporting segment dominance.Seafood applications represent a strong export-oriented category, especially coated shrimp, fish fillets, and calamari products. Increasing international seafood trade and demand for ready-to-fry formats continue to support steady volume growth.

Plant-based protein applications are the fastest-growing segment, expanding at over 10% annually. Growth is fueled by the rapid expansion of alternative meat brands requiring gluten-free coating systems to enhance texture realism and consumer acceptance. The leading driver in this segment is the need for allergen-free, clean-label formulations that replicate the sensory appeal of traditional breaded meat products.

Distribution Channel Insights

Direct B2B sales account for nearly 63% of total market share, reflecting long-term, high-volume contracts between ingredient manufacturers and large-scale food processing companies. The primary growth driver for this channel is the need for customized formulation support, technical service collaboration, and stable raw material pricing agreements.Specialty ingredient distributors serve mid-sized and regional processors by offering diversified portfolios and localized technical assistance. Meanwhile, digital procurement platforms are gradually gaining adoption among smaller manufacturers seeking price transparency, flexible sourcing, and faster lead times. The increasing digitization of supply chain management is expected to strengthen this channel over the forecast period.

End-Use Industry Insights

Food processing companies dominate the market with approximately 52% market share, driven largely by frozen food manufacturers and ready-to-eat meal producers. The leading growth driver in this segment is the rising global demand for packaged convenience foods that require consistent, scalable coating solutions.Quick Service Restaurants (QSRs) represent the fastest-growing end-use segment, supported by rapid global outlet expansion, menu innovation, and increasing gluten-free product offerings. Major QSR chains are incorporating allergen-free coated menu items to address growing consumer dietary preferences.Institutional catering services and airline meal providers are gradually integrating gluten-free coated options into standardized menus. Although smaller in share, this segment benefits from rising regulatory compliance requirements and the expansion of large-scale catering contracts.

| By Product Type | By Flour Base | By Application | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 36% of the 2025 market share, making it the leading regional market. The United States drives the majority of regional demand due to high consumption of breaded poultry and seafood products, strong retail penetration of gluten-free frozen foods, and advanced food processing infrastructure.The primary regional growth drivers include stringent allergen labeling regulations, high consumer awareness regarding gluten intolerance, and strong demand for premium convenience foods. Additionally, Canada’s expanding private-label gluten-free product lines and increasing health-conscious consumer base further contribute to regional expansion.

Europe

Europe holds nearly 29% market share, with Germany, the United Kingdom, France, and Italy leading regional consumption. Strict EU allergen regulations and certification standards for gluten-free production create a structured regulatory environment that supports product transparency and consumer trust.Key regional growth drivers include rising demand for clean-label foods, expansion of private-label gluten-free offerings, and increasing adoption of plant-based coated products. Western Europe remains dominant, while Eastern Europe presents emerging opportunities due to growing urbanization and processed food demand.

Asia-Pacific

Asia-Pacific represents around 24% of the global market and is the fastest-growing region, expanding at nearly 9.8% CAGR. China, India, Japan, and Thailand are major contributors to regional revenue growth.The leading growth drivers include rapid expansion of the food processing industry, rising disposable incomes, urbanization, and increasing Western-style fast food consumption. India’s food processing growth under government-backed manufacturing initiatives and Thailand’s dominance in seafood exports significantly contribute to demand for gluten-free coating systems. Additionally, Japan’s mature convenience food sector continues to support stable demand.

Latin America

Latin America holds approximately 5% market share, led by Brazil and Mexico. Growth in the region is primarily supported by expanding poultry exports, increasing domestic processed food consumption, and improving cold chain infrastructure.The modernization of food manufacturing facilities and rising penetration of international QSR chains are additional drivers supporting gradual market expansion across the region.

Middle East & Africa

The Middle East & Africa region accounts for roughly 6% of the global market. The UAE and Saudi Arabia are key demand centers due to high levels of premium food imports and expanding hospitality sectors.Regional growth is driven by rising QSR penetration, tourism sector expansion, increasing reliance on imported processed foods, and growing awareness of specialty dietary products. While the market remains relatively smaller compared to developed regions, improving retail infrastructure and premium product demand are expected to support steady growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Gluten-Free Coating Premix Market

- Kerry Group plc

- Cargill Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tate & Lyle PLC

- Sensient Technologies Corporation

- Associated British Foods plc

- Ajinomoto Co., Inc.

- Newly Weds Foods

- Blendex Company

- Bowman Ingredients

- House-Autry Mills

- Prima Limited

- McCormick & Company

- Bunge Limited