Gluten Free Biscuits Market Size

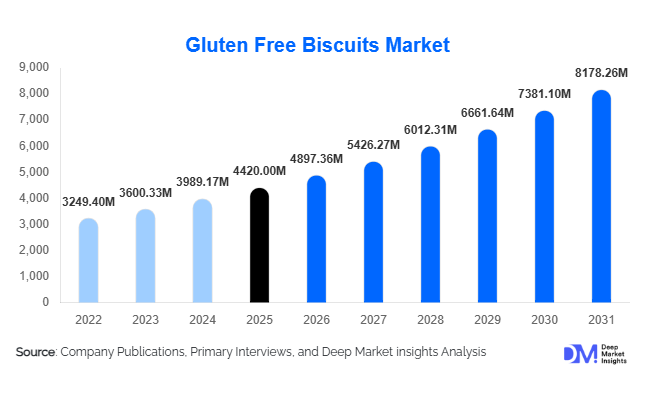

According to Deep Market Insights, the global gluten free biscuits market size was valued at USD 4,420 million in 2025 and is projected to grow from USD 4,897.36 million in 2026 to reach USD 8,178.26 million by 2031, expanding at a CAGR of 10.8% during the forecast period (2026–2031). The gluten free biscuits market growth is primarily driven by the rising prevalence of gluten intolerance and celiac disease, increasing consumer inclination toward health and wellness products, and growing demand for clean-label, allergen-free snacks. The transition of gluten-free products from niche medical foods to mainstream lifestyle choices is further accelerating global demand.

Key Market Insights

- Gluten-free biscuits are increasingly positioned as functional and health-oriented snacks, appealing to both medically required and lifestyle-driven consumers.

- Product innovation using alternative flours such as almond, coconut, and chickpea is significantly improving taste, texture, and nutritional value.

- North America dominates the global market, driven by strong consumer awareness and established retail infrastructure.

- Asia-Pacific is the fastest-growing region, supported by rising disposable income and western dietary adoption.

- E-commerce and direct-to-consumer channels are transforming distribution, enabling niche brands to scale globally.

- Sustainable packaging and clean-label formulations are emerging as key differentiators among premium brands.

What are the latest trends in the gluten free biscuits market?

Rise of Functional and Fortified Biscuits

Manufacturers are increasingly incorporating functional ingredients such as protein isolates, dietary fiber, probiotics, and superfoods into gluten-free biscuits. These innovations are aimed at enhancing nutritional value while aligning with consumer demand for healthier snacking options. Products targeting specific health concerns such as digestion, immunity, and weight management are gaining traction, particularly among urban consumers. The integration of plant-based proteins and low glycemic index ingredients is also expanding the appeal of gluten-free biscuits to fitness enthusiasts and diabetic consumers, transforming the segment into a broader functional food category.

Clean Label and Sustainable Product Development

Consumers are increasingly prioritizing transparency in food labeling and environmental sustainability. This has led to a surge in demand for gluten-free biscuits made with organic, non-GMO, and minimally processed ingredients. Manufacturers are also shifting toward eco-friendly packaging solutions such as biodegradable wraps and recyclable materials. Sustainability certifications and ethical sourcing practices are becoming critical for brand differentiation, particularly in developed markets. This trend is not only enhancing brand loyalty but also enabling companies to command premium pricing in competitive markets.

What are the key drivers in the gluten free biscuits market?

Increasing Prevalence of Gluten Intolerance

The growing incidence of celiac disease and non-celiac gluten sensitivity is a primary driver of market growth. Improved diagnostic capabilities and awareness campaigns have expanded the consumer base requiring gluten-free diets. This has created a steady demand for gluten-free bakery products, including biscuits, across both developed and emerging markets.

Expansion of Health-Conscious Consumer Base

Beyond medical necessity, a significant portion of consumers is adopting gluten-free diets as part of a healthier lifestyle. Gluten-free products are often perceived as easier to digest and beneficial for weight management. This perception has broadened market demand, with health-conscious individuals actively seeking gluten-free snack options.

What are the restraints for the global market?

High Product Pricing

Gluten-free biscuits are generally more expensive than conventional biscuits due to higher raw material costs and specialized manufacturing processes. Ingredients such as almond flour and coconut flour are costlier, which increases the final product price. This limits accessibility in price-sensitive markets and restricts widespread adoption.

Taste and Texture Challenges

Despite advancements in formulation, gluten-free biscuits often face criticism for inferior taste and texture compared to traditional products. Achieving the desired mouthfeel without gluten remains a technical challenge, requiring continuous innovation and investment in research and development.

What are the key opportunities in the gluten free biscuits industry?

Emerging Market Expansion

Regions such as Asia-Pacific, Latin America, and the Middle East present significant growth opportunities due to increasing urbanization, rising disposable incomes, and growing awareness of gluten-related health issues. Countries like India and China are particularly underpenetrated, offering substantial scope for market expansion. As awareness improves, these regions are expected to contribute significantly to future demand growth.

Premium and Functional Product Innovation

The development of premium gluten-free biscuits with added health benefits is creating new revenue streams. Products enriched with protein, fiber, and superfoods are attracting health-conscious consumers willing to pay higher prices. This trend is enabling manufacturers to differentiate their offerings and improve profit margins while addressing evolving consumer preferences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4420.00 Million |

| Market Size in 2026 | USD 4897.36 Million |

| Market Size in 2031 | USD 8178.26 Million |

| CAGR | 10.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The gluten free biscuits market is witnessing strong segmentation dynamics, with sweet biscuits continuing to dominate the global landscape, accounting for approximately 48% of total market share in 2025. This dominance is primarily driven by the deeply rooted consumer inclination toward indulgent snacking experiences combined with the growing availability of gluten-free alternatives that closely mimic traditional wheat-based products in taste and texture. Manufacturers are heavily investing in product innovation, incorporating diverse flavors such as chocolate, vanilla, fruit-infused variants, and premium artisanal offerings to appeal to both gluten-sensitive and mainstream consumers. The leading driver for this segment is the increasing demand for indulgent yet diet-compliant snack options, as consumers no longer want to compromise on taste while adhering to gluten-free lifestyles. Additionally, attractive packaging, aggressive branding strategies, and strong shelf visibility in retail stores further reinforce the segment’s leadership.Functional gluten-free biscuits are emerging as one of the fastest-growing segments within the market, driven by the convergence of nutrition and convenience. These products are fortified with proteins, dietary fiber, vitamins, and minerals, targeting specific consumer needs such as digestive health, energy boosting, and weight management. The leading growth driver for this segment is the increasing consumer focus on functional nutrition and preventive healthcare, particularly among millennials and fitness enthusiasts. Brands are leveraging clean-label formulations, plant-based proteins, and superfood ingredients to differentiate their offerings and tap into the premium segment of the market.Another noteworthy trend is the growing demand for gluten-free biscuits tailored for children. These products are often fortified with essential nutrients such as calcium, iron, and vitamins to support growth and development, while also featuring appealing shapes, flavors, and packaging to attract younger consumers. The expansion of this sub-segment is driven by the rising prevalence of food allergies among children and increasing parental awareness regarding dietary safety. As a result, manufacturers are focusing on creating allergen-free, nutritious, and tasty snack options that cater specifically to this demographic, further broadening the market scope.

Application Insights

In terms of application, household consumption remains the dominant segment, accounting for nearly 68% of total demand in the gluten free biscuits market. This dominance is largely attributed to the rising trend of at-home snacking, which gained momentum during recent years and continues to persist as a long-term consumer behavior. The leading driver for this segment is the growing adoption of gluten-free diets as part of everyday lifestyle choices, rather than being limited to medical necessity. Consumers are increasingly incorporating gluten-free products into their daily routines due to perceived health benefits, digestive comfort, and weight management considerations. The availability of a wide range of products across price points further supports this segment’s growth, making gluten-free biscuits accessible to a broader consumer base.Institutional applications, particularly in hospitals, schools, and corporate cafeterias, are also gaining importance within the market. These settings require strict adherence to dietary guidelines and allergen management, making gluten-free products a critical component of meal planning. The segment’s growth is driven by the increasing emphasis on dietary compliance and health-focused meal programs, especially in developed regions where regulatory frameworks support the inclusion of allergen-free food options. Furthermore, the growing awareness of gluten intolerance and celiac disease among institutional decision-makers is encouraging the adoption of gluten-free biscuits as safe and convenient snack options.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the distribution landscape, holding approximately 42% of the market share. Their leadership is supported by extensive product assortments, competitive pricing, and strong consumer trust. The leading driver for this channel is the ability to provide a one-stop shopping experience with high product visibility and accessibility. These retail formats allow consumers to compare multiple brands and product variants, facilitating informed purchasing decisions. Additionally, strategic shelf placement, in-store promotions, and sampling campaigns play a crucial role in driving sales within this channel.Specialty health food stores and pharmacies play a vital role in catering to niche consumer segments, particularly those with specific dietary requirements or medical conditions. These outlets often offer curated selections of gluten-free products, along with expert guidance and product transparency. The growth of this channel is driven by the increasing demand for trusted sources of health-oriented and allergen-free products. Consumers seeking high-quality, certified gluten-free biscuits often prefer these specialized stores due to their focus on quality assurance and product authenticity.The expansion of omnichannel strategies is reshaping the distribution landscape, enabling brands to integrate online and offline channels seamlessly. This approach enhances market penetration and ensures consistent brand presence across multiple touchpoints. The driver behind this trend is the need for integrated retail experiences that align with evolving consumer expectations, allowing brands to maximize reach and optimize sales performance.

Consumer Type Insights

Health and wellness consumers represent the largest segment, accounting for around 38% of the market. This segment is driven by individuals who prioritize balanced nutrition, clean-label products, and overall well-being. The leading driver here is the increasing shift toward preventive healthcare and lifestyle-based dietary choices. These consumers are not necessarily gluten intolerant but choose gluten-free products as part of a broader health-conscious lifestyle, contributing significantly to market expansion.Celiac patients and gluten-intolerant individuals continue to form a stable and essential demand base for gluten-free biscuits. For these consumers, gluten-free products are a necessity rather than a preference. The growth of this segment is supported by the rising diagnosis rates and improved awareness of gluten-related disorders, along with better product availability and labeling standards. Manufacturers are focusing on strict quality control and certification to ensure product safety for this sensitive group.Vegan and clean-label consumers are emerging as a significant growth segment, driven by ethical, environmental, and health considerations. These consumers prefer products that are free from artificial additives, preservatives, and animal-derived ingredients. The key driver for this segment is the increasing demand for transparency, sustainability, and plant-based nutrition. Gluten-free biscuits that align with these values are gaining popularity, particularly among younger demographics.Weight management consumers are also contributing to market demand, as gluten-free products are often perceived as healthier alternatives to conventional snacks. Although this perception is not always nutritionally accurate, it continues to influence purchasing decisions. The segment is driven by the growing focus on calorie control and healthier snacking habits, especially among urban populations and fitness enthusiasts.

Explore more data points, trends and opportunities Download Free Sample Report

Gluten Free Biscuits Market Segmentations

By Product Type

- Sweet Biscuits

- Savory Biscuits

- Functional Biscuits

- Kids’ Biscuits

By Ingredient Base

- Rice Flour-Based

- Corn Flour-Based

- Almond Flour-Based

- Coconut Flour-Based

- Oat-Based

- Multigrain Gluten-Free Blends

- Legume-Based

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Health Stores

- Pharmacies

- Direct-to-Consumer

Regional Insights

North America

North America holds the largest share of the gluten free biscuits market, accounting for approximately 38% in 2025. The United States leads the region, supported by high consumer awareness of gluten-related disorders, a well-established retail infrastructure, and the widespread availability of gluten-free products across multiple channels. A key growth driver in this region is the strong consumer awareness and proactive adoption of specialized diets, including gluten-free, keto, and clean-label trends. Additionally, the presence of major market players and continuous product innovation contribute to sustained market growth. Canada also plays a significant role, with growth driven by favorable regulatory frameworks for gluten labeling and increasing health consciousness among consumers. The region benefits from advanced supply chains and strong marketing strategies, further solidifying its leadership position.

Europe

Europe accounts for around 30% of the global market, with key countries including the United Kingdom, Germany, Italy, and France. The region is characterized by stringent food safety and labeling regulations, which enhance consumer confidence in gluten-free products. The primary driver for growth in Europe is the strict regulatory environment combined with high consumer awareness of dietary health. Additionally, the rising demand for organic and clean-label products is significantly influencing market dynamics. European consumers are increasingly seeking premium, artisanal gluten-free biscuits made with natural ingredients, supporting the growth of niche and specialty brands. The region’s strong bakery tradition also facilitates the adoption of gluten-free alternatives, further driving market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the gluten free biscuits market, with a projected CAGR exceeding 12%. Countries such as China and India are emerging as key markets due to rapid urbanization, rising disposable incomes, and increasing exposure to global dietary trends. The leading driver for this region is the growing awareness of health and wellness combined with expanding middle-class populations. As consumers become more informed about gluten intolerance and dietary choices, demand for gluten-free products is rising steadily. Japan and Australia represent more mature markets within the region, characterized by stable demand and a strong preference for premium and high-quality products. Additionally, the expansion of modern retail formats and e-commerce platforms is facilitating greater product accessibility across the region.

Latin America

Latin America holds approximately 8% of the global market, with Brazil and Mexico leading demand. The region is experiencing gradual growth, supported by increasing health awareness and improvements in retail infrastructure. The key driver for this region is the rising consumer interest in healthier food options and the gradual adoption of specialized diets. Although awareness of gluten intolerance is still developing compared to other regions, growing urbanization and exposure to international food trends are contributing to market expansion. Local manufacturers are also beginning to introduce gluten-free product lines, further supporting growth.

Middle East & Africa

The Middle East and Africa account for around 6% of the market, with growth driven by urbanization, rising disposable incomes, and increasing availability of specialty food products. Countries such as the UAE and South Africa are key contributors to regional demand. The primary growth driver in this region is the expanding expatriate population and increasing demand for international food products, including gluten-free options. Additionally, the development of modern retail infrastructure and the growing presence of global brands are enhancing product availability. Rising health awareness and the gradual shift toward healthier lifestyles are also supporting market growth, although the region remains in the early stages of adoption compared to more developed markets.

Key Players in the Gluten Free Biscuits Market

- Mondelez International

- Nestlé S.A.

- General Mills Inc.

- Kellogg Company

- PepsiCo Inc.

- The Hain Celestial Group

- Dr. Schär AG

- Enjoy Life Foods

- Freedom Foods Group

- Bob’s Red Mill Natural Foods

- Nature’s Path Foods

- Lotus Bakeries

- Arnott’s Group

- Hero Group

- Barilla Group