Glucose Syrup, Dextrose & Maltodextrin Market Size

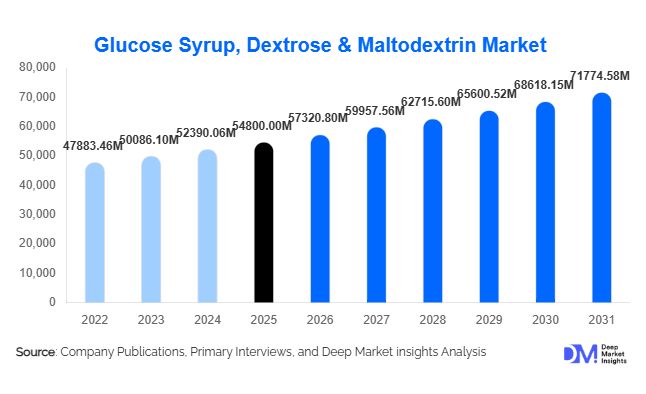

According to Deep Market Insights, the global glucose syrup, dextrose & maltodextrin market size was valued at USD 54,800 million in 2025 and is projected to grow from USD 57,320.80 million in 2026 to reach USD 71,774.58 million by 2031, expanding at a CAGR of 4.6% during the forecast period (2026–2031). Market growth is primarily driven by increasing demand for processed and packaged foods, rising consumption of clinical and sports nutrition products, and expanding pharmaceutical applications. The growing role of carbohydrate-based ingredients in fermentation, bio-based chemicals, and industrial processing further supports steady global demand.

Key Market Insights

- Food & beverages account for nearly 68% of total demand, with bakery, confectionery, dairy, and beverage manufacturing driving large-volume consumption.

- Corn-based production dominates with over 60% share, supported by established wet-milling infrastructure in the U.S., China, and Europe.

- Asia-Pacific leads the global market with approximately 38% share, driven by China and India’s expanding food processing and fermentation industries.

- Pharmaceutical-grade dextrose is experiencing accelerated growth, driven by rising demand for IV fluids and clinical nutrition applications.

- Liquid form accounts for nearly 58% of market volume, owing to seamless integration into industrial production systems.

- The top five players hold around 42–45% of the global market, reflecting moderate consolidation with strong multinational participation.

What are the latest trends in the glucose syrup, dextrose & maltodextrin market?

Rising Demand for Specialty and Clean-Label Ingredients

Food manufacturers are increasingly shifting toward non-GMO, organic-certified, and clean-label carbohydrate ingredients. Maltodextrin with controlled dextrose equivalent (DE) values is gaining traction in infant formula, nutraceuticals, and sports nutrition due to its digestibility and functional stability. Specialty pharmaceutical-grade dextrose complying with USP and EP standards is also expanding in clinical nutrition and injectable formulations. Producers are investing in enzymatic hydrolysis technologies to improve purity, reduce residual proteins, and enhance traceability, responding to regulatory and consumer-driven transparency requirements.

Integration with Bio-Manufacturing and Fermentation Industries

Glucose syrup and dextrose are increasingly used as fermentation substrates in the production of amino acids, citric acid, lactic acid, antibiotics, and bio-based chemicals. With the global bio-economy expanding, carbohydrate feedstock demand is strengthening, particularly in China and Europe. Investments in bio-based plastics and green chemicals are creating downstream industrial applications beyond traditional food uses. This trend positions starch-derived sweeteners as critical raw materials within sustainable manufacturing ecosystems.

What are the key drivers in the glucose syrup, dextrose & maltodextrin market?

Expansion of Processed Food and Beverage Manufacturing

Global processed food output continues to grow steadily, particularly in the Asia-Pacific and Latin America. Glucose syrup functions as a sweetener, humectant, and texture stabilizer in confectionery and baked goods, while maltodextrin improves mouthfeel and shelf stability in dairy and beverage products. The structural rise in urban consumption and modern retail penetration directly supports ingredient demand.

Growing Pharmaceutical and Clinical Nutrition Demand

Dextrose is widely used in IV fluids, oral rehydration salts, and injectable solutions. Expansion of healthcare infrastructure in emerging markets and increasing hospitalization rates globally are strengthening pharmaceutical-grade carbohydrate demand. The clinical nutrition sector, growing above 6% annually, further boosts high-purity dextrose and maltodextrin consumption.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in corn, wheat, and cassava prices significantly influence production costs. Weather disruptions, trade restrictions, and geopolitical tensions can compress margins, particularly for manufacturers lacking vertical integration.

Regulatory Pressure on Sugar Consumption

Sugar reduction policies and health awareness campaigns in Europe and North America indirectly impact glucose syrup demand, especially in carbonated beverages. Reformulation trends toward alternative sweeteners present a long-term competitive challenge.

What are the key opportunities in the industry?

Emerging Market Capacity Expansion

Countries such as India, Vietnam, and Indonesia are rapidly expanding food processing and fermentation industries. Government-backed industrial corridors and export incentives create favorable conditions for starch hydrolysis capacity additions, particularly cassava-based production in Southeast Asia.

High-Value Specialty Grades and Functional Nutrition

Manufacturers focusing on low-DE maltodextrin, organic-certified glucose syrups, and pharmaceutical-grade dextrose can achieve premium pricing. Sports nutrition, infant formula, and medical foods are high-growth segments offering superior margins compared to bulk sweetener applications.

Below is the optimized, expanded, and more analytical version of your requested sections. Leading segment drivers are clearly highlighted, and regional growth drivers are incorporated for each geography.

Product Type Insights

Glucose syrup remains the leading product segment, accounting for approximately 46% of total market revenue in 2025. Its dominance is primarily driven by its extensive application in confectionery, bakery fillings, beverages, and processed foods, where it functions as a sweetener, humectant, crystallization inhibitor, and texture stabilizer. The strong growth of global confectionery production, particularly in Asia-Pacific and Latin America, continues to reinforce demand for high-DE glucose syrups. Additionally, beverage manufacturers prefer high-DE variants due to their fermentability and cost-efficiency compared to sucrose.

Dextrose holds a substantial share of the market, supported by its critical role in pharmaceutical formulations, IV fluids, oral rehydration salts, and clinical nutrition products. The expansion of healthcare infrastructure in emerging economies and increasing hospitalization rates globally are driving pharmaceutical-grade dextrose demand. Meanwhile, maltodextrin is the fastest-growing product category, fueled by rising consumption in sports nutrition, infant formula, and functional foods. Medium- and low-DE maltodextrin grades dominate clean-label and controlled-release formulations due to their digestibility, neutral taste, and stabilizing properties. Growth in nutraceuticals and high-protein beverages is further accelerating specialty maltodextrin demand.

Raw Material Insights

Corn-based production accounts for nearly 62% of global output in 2025, making it the dominant raw material segment. This leadership is supported by well-established wet-milling infrastructure in the United States, China, and parts of Europe. Corn offers higher starch yield, consistent supply chains, and cost efficiencies due to large-scale agricultural production and government subsidies in key producing countries. Vertical integration among major players further strengthens corn’s cost advantage and supply security.

Cassava-based production is expanding rapidly in Thailand and Vietnam, driven by export-oriented manufacturing and lower raw material costs. Cassava starch provides flexibility in regions with limited corn availability and supports growing demand in Southeast Asia and China. Wheat-based production remains relevant in Europe, particularly due to regional agricultural availability and regulatory preferences supporting non-GMO wheat sourcing. However, wheat-based production faces cost pressures due to fluctuating grain markets and geopolitical supply disruptions.

Form Insights

Liquid form dominates the market with approximately 58% share in 2025, primarily due to its direct compatibility with large-scale beverage, confectionery, and fermentation production lines. Bulk tanker transportation, ease of blending, and reduced rehydration requirements make liquid glucose syrup highly efficient for industrial processors. Fermentation industries also prefer liquid dextrose solutions for seamless integration into bioreactors and enzymatic processes.

Powder and crystalline forms are increasingly important in pharmaceutical and nutraceutical applications, where precise dosing, longer shelf stability, and transport flexibility are critical. Dextrose monohydrate and anhydrous crystalline forms are widely used in injectable and oral pharmaceutical formulations. Powdered maltodextrin is preferred in dry beverage mixes, infant formula, and sports nutrition blends due to its low moisture content and storage stability.

Application Insights

Food & beverages remain the dominant application segment, accounting for approximately 68% of total market demand in 2025. Growth in packaged foods, bakery products, dairy desserts, and ready-to-drink beverages continues to support high-volume consumption. Urbanization, changing dietary patterns, and retail modernization in emerging markets are key structural drivers.

Pharmaceuticals and nutraceuticals represent the second-largest application segment, driven by expanding IV fluid production, medical nutrition demand, and dietary supplements. Industrial fermentation is emerging as a steady-growth application area, supported by increasing production of citric acid, lactic acid, amino acids, and bio-based chemicals. Infant nutrition remains a specialized but high-margin segment, particularly in Asia-Pacific, where demand for premium formula products continues to expand.

Distribution Channel Insights

Direct industrial sales dominate the market with nearly 75% share, reflecting the bulk procurement practices of multinational food, beverage, and pharmaceutical manufacturers. Long-term supply contracts, integrated logistics networks, and price hedging strategies characterize this channel. Large buyers prioritize supply reliability and cost stability, favoring vertically integrated producers.

Ingredient distributors cater primarily to small- and medium-sized food processors, offering technical support and flexible order volumes. Contract manufacturing supply is gaining traction in specialty nutrition and pharmaceutical segments, where customized formulations and smaller batch production are required.

| By Product Type | By Raw Material | By Form | By Application | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 38% of the global market share in 2025, making it the largest regional market. China leads both production and consumption, supported by its massive fermentation industry, expanding processed food manufacturing, and strong export orientation. The country’s bio-based chemical sector significantly drives glucose and dextrose demand as fermentation substrates.

India is the fastest-growing major market in the region, expanding at a 6–7% CAGR due to rapid food processing industrialization, government-backed manufacturing initiatives, rising healthcare expenditure, and growing sports nutrition demand. Southeast Asian countries such as Thailand and Vietnam are key cassava-based exporters, benefiting from favorable agricultural conditions and strong trade linkages with China and Japan. Urban population growth and rising disposable incomes further strengthen regional consumption trends.

North America

North America holds roughly 27% of global demand, with the United States accounting for the majority share. The region’s dominance is supported by advanced corn wet-milling infrastructure, abundant raw material availability, and strong pharmaceutical manufacturing capacity. Growth drivers include steady processed food consumption, expanding demand for clinical nutrition, and growing bio-industrial applications, such as bioplastics and organic acids. Government incentives for bio-manufacturing and renewable chemicals are further strengthening industrial glucose demand.

Europe

Europe represents approximately 22% of the global market, led by Germany, France, and the Netherlands. Regional growth is supported by pharmaceutical-grade ingredient demand and high-value specialty applications. However, sugar reduction regulations and beverage reformulation policies moderate growth in conventional sweetener segments. Investments in sustainable bio-economy initiatives and green chemical production are emerging as important drivers, particularly in Western Europe.

Latin America

Latin America contributes about 8% of global demand, with Brazil and Mexico as primary markets. Brazil benefits from an integrated corn processing infrastructure and expanding domestic food production. Rising urbanization, growth in packaged foods, and increasing exports of processed food products are supporting regional demand. Mexico’s strong beverage manufacturing base also contributes significantly to glucose syrup consumption.

Middle East & Africa

The Middle East & Africa region accounts for nearly 5% of the global market share. Demand growth is driven by expanding beverage production, increasing food imports, and the gradual development of local pharmaceutical manufacturing. Saudi Arabia and South Africa are key markets, supported by industrial diversification initiatives and investments in food security. Population growth, rising urban consumption, and increasing healthcare spending are expected to gradually accelerate regional demand over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Glucose Syrup, Dextrose & Maltodextrin Market

- Cargill

- Archer Daniels Midland (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- Tereos Group

- Grain Processing Corporation

- AGRANA Beteiligungs-AG

- COFCO Biochemical

- Global Bio-Chem Technology

- Gulshan Polyols

- Avebe

- Lihua Starch

- Thai Roong Ruang Group

- Daesang Corporation