Gloriosa Superba Market Size

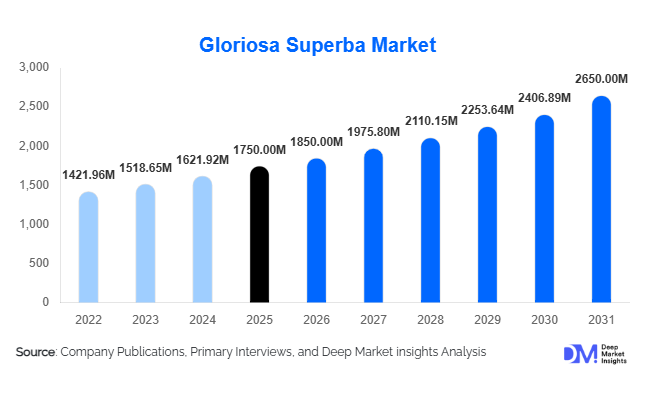

According to Deep Market Insights, the global Gloriosa superba market size was valued at USD 1,750 million in 2025 and is projected to grow from USD 1,850 million in 2026 to reach USD 2,560 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for colchicine-based pharmaceutical formulations, increasing adoption of plant-derived active pharmaceutical ingredients (APIs), and expanding applications in herbal medicine, oncology research, and cytogenetic studies.

Key Market Insights

- Pharmaceutical demand for colchicine remains the dominant growth driver, particularly for gout treatment, anti-inflammatory drugs, and emerging oncology applications.

- Standardized alkaloid extracts are gaining strong traction as pharmaceutical companies increasingly demand high-purity, regulated botanical APIs.

- Asia-Pacific dominates global supply, led by India and Sri Lanka, due to favorable agro-climatic conditions and established medicinal plant cultivation systems.

- North America and Europe lead consumption of high-value extracts, driven by strong pharmaceutical R&D ecosystems and strict quality regulations.

- Shift toward organized cultivation and contract farming is reducing dependency on wild harvesting and improving supply chain traceability.

- Growing integration of botanical compounds in biotech research is expanding demand from laboratories and academic institutions.

What are the latest trends in the Gloriosa Superba Market?

Standardization and Pharmaceutical-Grade Extraction Growth

A major trend shaping the Gloriosa superba market is the rapid transition from raw botanical trade to pharmaceutical-grade standardized extracts. Manufacturers are increasingly investing in advanced extraction technologies such as supercritical fluid extraction and chromatographic purification systems to isolate colchicine with higher purity and consistency. This shift is being driven by stringent regulatory requirements in developed markets and the growing preference for plant-derived APIs in drug manufacturing. As a result, value addition within the supply chain is increasing, with extract-based products commanding significantly higher margins compared to raw tubers and seeds.

Expansion of Cultivation and Sustainable Sourcing Models

Another key trend is the expansion of structured cultivation programs and contract farming models. Historically, Gloriosa superba supply has been heavily dependent on wild harvesting, leading to supply instability and ecological concerns. Governments and private agribusiness firms are now promoting regulated cultivation zones to ensure sustainable sourcing, consistent alkaloid yield, and improved traceability. This trend is particularly strong in Asia-Pacific, where medicinal plant cultivation is being integrated into rural agricultural development programs. Sustainability certification and export compliance standards are also becoming important market differentiators.

What are the key drivers in the Gloriosa Superba Market?

Rising Demand for Colchicine-Based Pharmaceuticals

The most significant driver of the market is the increasing global demand for colchicine, a key alkaloid extracted from Gloriosa superba. It is widely used in the treatment of gout, familial Mediterranean fever, and is increasingly being explored for oncology-related applications. The expansion of pharmaceutical pipelines focused on plant-derived APIs is further accelerating demand, particularly in North America and Europe, where regulatory frameworks support standardized botanical drug development. This has resulted in sustained procurement of high-purity extracts from global suppliers.

Growth in Herbal and Traditional Medicine Systems

The rising adoption of herbal and traditional medicine systems, including Ayurveda and other plant-based healthcare models, is another strong growth driver. Gloriosa superba is increasingly used in controlled herbal formulations due to its bioactive properties. Expanding consumer preference for natural and plant-based remedies is boosting demand across Asia-Pacific and select Western alternative medicine markets, further widening its commercial applications beyond pharmaceuticals.

Expanding Biotechnology and Research Applications

Growing investment in biotechnology, cytogenetics, and cancer research is significantly supporting market expansion. Colchicine derived from Gloriosa superba is widely used in chromosome analysis and cellular research studies. Increasing funding for life sciences research institutions globally is strengthening demand for high-purity extracts, particularly for laboratory-grade applications.

What are the restraints for the global market?

Toxicity and Regulatory Compliance Challenges

One of the key restraints in the Gloriosa superba market is the inherent toxicity of the plant’s alkaloid compounds. Colchicine requires strict handling, dosage control, and processing standards, which increases production costs and regulatory complexity. This limits its use to controlled pharmaceutical and research environments, restricting broader commercialization opportunities.

Supply Chain Instability and Overharvesting Risks

The market also faces challenges related to supply chain instability due to reliance on wild harvesting in certain regions. Overexploitation of natural populations has raised sustainability concerns, leading to regulatory restrictions in some countries. These issues contribute to price volatility and create barriers to consistent global supply.

What are the key opportunities in the Gloriosa Superba Industry?

Pharmaceutical API Expansion and High-Purity Extraction Technologies

A major opportunity lies in scaling up pharmaceutical-grade API production from Gloriosa superba. Increasing demand for plant-based drug ingredients presents strong potential for manufacturers investing in advanced purification and extraction infrastructure. Companies that can achieve consistent high-purity colchicine extraction will gain long-term contracts from global pharmaceutical firms.

Contract Farming and Organized Cultivation Expansion

The development of structured cultivation ecosystems offers a significant opportunity for market expansion. Contract farming models can stabilize supply, improve quality consistency, and support export compliance. Governments promoting medicinal plant agriculture are expected to drive large-scale cultivation initiatives, particularly in India and Southeast Asia.

Growth in Oncology and Genetic Research Applications

Increasing global investment in oncology and genetic research is creating new demand avenues. Gloriosa superba-derived colchicine is widely used in chromosomal studies and cancer research applications. Expansion of biotechnology labs and academic research funding is expected to further strengthen this niche but high-value segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1750 Million |

| Market Size in 2026 | USD 1850 Million |

| Market Size in 2031 | USD 2650 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product type segmentation of the Gloriosa superba market reflects a clear and accelerating transition toward cultivated sources, with cultivated tubers emerging as the dominant segment. In 2025, cultivated tubers account for an estimated 38% share of the global market, primarily due to their consistent alkaloid concentration, particularly colchicine, and enhanced traceability across regulated supply chains. Pharmaceutical manufacturers increasingly prioritize standardized raw materials that ensure batch-to-batch uniformity, making cultivated tubers significantly more reliable compared to wild-harvested variants. This consistency directly supports drug formulation stability and regulatory compliance, which are critical factors in pharmaceutical production.Seeds represent a secondary but strategically important segment, primarily supporting propagation and the expansion of controlled farming operations. With rising investments in medicinal plant cultivation, seeds are gaining importance as foundational inputs for scaling production capacity. Their role in genetic improvement and yield optimization also contributes to long-term market sustainability. Meanwhile, leaves and stems hold minimal commercial significance due to their comparatively low alkaloid content; however, they are occasionally utilized in research and experimental applications, particularly in phytochemical and cytogenetic studies.Overall, the dominance of cultivated tubers is driven by their superior quality consistency, regulatory compliance, sustainability advantages, and alignment with large-scale pharmaceutical production requirements. This segment is expected to maintain its leadership position as the industry continues to prioritize traceable and standardized botanical inputs.

Application Insights

Application-wise, the pharmaceutical segment clearly dominates the Gloriosa superba market, accounting for approximately 56% share in 2025. This dominance is primarily attributed to the well-established therapeutic use of colchicine, a key alkaloid derived from the plant, in the treatment of gout and other inflammatory conditions. Beyond its traditional applications, colchicine is gaining increasing attention in oncology research, where it is being explored for its anti-mitotic properties and potential use in cancer therapies. The expanding scope of pharmaceutical research and development is therefore a major driver for this segment.Nutraceutical and herbal applications are witnessing steady growth, driven by the global shift toward preventive healthcare and natural wellness solutions. Consumers are increasingly favoring plant-based supplements that offer anti-inflammatory and therapeutic benefits without the side effects commonly associated with synthetic drugs. This trend is particularly pronounced in emerging economies as well as in developed markets where clean-label and organic products are gaining traction. As a result, manufacturers are incorporating Gloriosa extracts into herbal formulations, further expanding the application base.Overall, the pharmaceutical segment remains the primary growth engine, driven by increasing disease prevalence, expanding research applications, and the growing acceptance of botanical APIs in modern medicine.

Distribution Channel Insights

The distribution landscape of the Gloriosa superba market is characterized by a strong dominance of direct B2B sales channels, which account for approximately 45% share in 2025. This dominance is largely driven by the preferences of pharmaceutical companies, which prioritize direct sourcing from certified cultivators and extract manufacturers to ensure quality control, traceability, and regulatory compliance. Direct procurement enables better coordination between suppliers and buyers, reduces intermediaries, and enhances supply chain transparency, all of which are critical in regulated industries.Specialty botanical traders, traditionally active in raw material markets, are facing challenges due to increasing regulatory scrutiny and the need for standardized products. While they continue to serve niche markets, their role is diminishing in the face of growing demand for certified and traceable supply chains. Overall, the distribution channel landscape is evolving toward greater integration, transparency, and efficiency, with direct B2B sales remaining the leading segment due to their alignment with industry requirements.

End-Use Insights

In terms of end-use, pharmaceutical and biopharmaceutical companies represent the largest segment, accounting for approximately 48% of total demand in 2025. The dominance of this segment is primarily driven by the extensive use of Gloriosa-derived compounds in drug formulation and research. The increasing focus on developing plant-based therapeutics, coupled with rising investments in pharmaceutical R&D, is significantly boosting demand from this segment. Additionally, the need for high-purity and standardized raw materials further strengthens the reliance of pharmaceutical companies on cultivated sources.Export-driven demand plays a significant role, especially for producers in Asia-Pacific who supply raw materials and extracts to developed markets such as North America and Europe. The increasing globalization of pharmaceutical supply chains is enabling producers to tap into international demand, further diversifying end-use applications. Overall, the end-use landscape is expanding, with pharmaceutical companies remaining the primary drivers due to their consistent and large-scale demand.

Explore more data points, trends and opportunities Download Free Sample Report

Gloriosa Superba Market Segmentations

By Product Type

- Cultivated Tubers

- Wild-Harvested Tubers

- Seeds

- Leaves & Stems

By Form

- Raw Dried Plant Material

- Powdered Extract

- Standardized Alkaloid Extract

- Liquid Botanical Extracts

By Application

- Pharmaceutical Use

- Nutraceuticals & Dietary Supplements

- Cosmetic & Dermatological Applications

- Research & Cytogenetic Applications

By End-Use Industry

- Pharmaceutical & Biopharmaceutical Companies

- Herbal & Ayurvedic Manufacturers

- Research Laboratories & Institutions

- Cosmetic & Personal Care Industry

By Distribution Channel

- Direct B2B Sales

- Herbal Raw Material Exporters

- Specialty Botanical Trading Companies

- Online B2B Ingredient Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global Gloriosa superba market, accounting for approximately 52% share in 2025. The region’s leadership is primarily driven by countries such as India, Sri Lanka, and Thailand, which possess favorable climatic conditions for cultivation and well-established medicinal plant farming practices. India, in particular, stands out as the largest producer, supported by a robust agricultural infrastructure, skilled labor, and strong export capabilities.Cost advantages also play a crucial role, as lower labor and production costs enable Asia-Pacific producers to offer competitive pricing in global markets. The presence of established supply chains and export networks ensures efficient distribution to international buyers. Furthermore, increasing investments in processing and extraction facilities are enhancing the value-added capabilities of regional players. These combined factors make Asia-Pacific not only the largest but also the fastest-growing region in the market.

North America

North America holds approximately 21% of the global market share, driven by strong demand from the pharmaceutical and research sectors in the United States and Canada. The region’s growth is primarily fueled by advanced R&D activities and the increasing adoption of botanical APIs in drug development. Pharmaceutical companies in North America are actively exploring plant-based compounds for new therapeutic applications, particularly in oncology and inflammatory diseases.Strict regulatory standards in the region also contribute to market growth by driving demand for high-quality, standardized, and traceable raw materials. As a result, North American companies rely heavily on imports from Asia-Pacific, where large-scale cultivation ensures consistent supply. Additionally, the growing trend toward natural and plant-based health products is supporting the expansion of nutraceutical applications, further boosting regional demand.

Europe

Europe accounts for approximately 18% of the global market, with key countries including Germany, France, and the United Kingdom leading consumption. The region’s growth is strongly influenced by stringent regulatory frameworks that emphasize quality, safety, and traceability of botanical ingredients. These regulations favor standardized extracts, thereby increasing reliance on certified suppliers, particularly from Asia-Pacific.The rising interest in plant-based pharmaceuticals and natural health products is another significant driver for the European market. Consumers are increasingly seeking alternative therapies and preventive healthcare solutions, which is encouraging pharmaceutical and nutraceutical companies to incorporate botanical ingredients into their products. Additionally, strong research infrastructure and funding support for life sciences are contributing to increased demand from research institutions.

Middle East & Africa

The Middle East & Africa region holds nearly 6% of the global market share, supported by growing adoption of herbal medicine and increasing pharmaceutical imports. Countries such as South Africa and the United Arab Emirates are emerging as key demand centers due to their expanding healthcare infrastructure and rising investments in the pharmaceutical sector.The region’s growth is driven by a combination of factors, including increasing awareness of natural therapies, rising healthcare expenditure, and improving access to medical treatments. Additionally, government initiatives aimed at diversifying healthcare systems and promoting alternative medicine are creating new opportunities for market expansion. Although still developing, the region shows significant potential for future growth.

Latin America

Latin America contributes approximately 3% of global demand, with Brazil and Mexico leading the market. The region’s growth is driven by the expansion of pharmaceutical industries and the increasing popularity of herbal and natural healthcare products. As consumers become more health-conscious, demand for plant-based supplements and treatments is rising, supporting market development.Improving healthcare infrastructure and increasing investments in pharmaceutical manufacturing are also contributing to regional growth. Additionally, the availability of local biodiversity resources provides opportunities for cultivating medicinal plants, although large-scale production remains limited compared to Asia-Pacific. As the region continues to develop its pharmaceutical capabilities, demand for Gloriosa-derived products is expected to grow steadily.

Key Players in the Gloriosa Superba Market

- Indena S.p.A.

- Sabinsa Corporation

- Arjuna Natural Pvt. Ltd.

- Givaudan (Naturex)

- Martin Bauer Group

- Euromed S.A.

- Nexira

- Bio-Botanica Inc.

- Kancor Ingredients Limited

- Natural Remedies Pvt. Ltd.

- Himalaya Wellness Company

- Pharmanza Herbal Pvt. Ltd.

- Alpine Herb Company

- Xi’an Herbking Biotechnology Co.

- Synthite Industries Ltd.