Gentle Digestion Formula Market Size

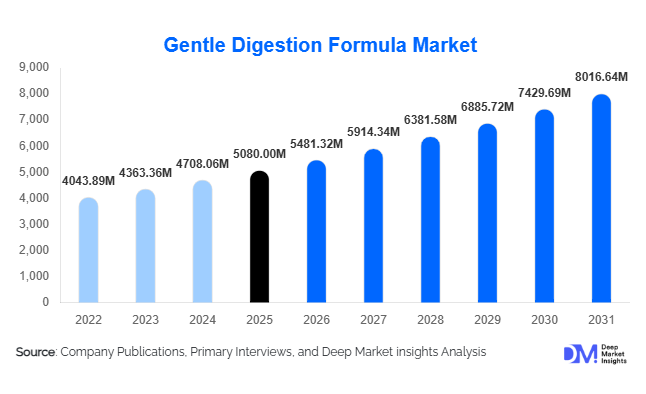

According to Deep Market Insights,the global gentle digestion formula market size was valued at USD 5,080 million in 2025 and is projected to grow from USD 5,481.32 million in 2026 to reach USD 8,016.64 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The market growth is primarily driven by the increasing prevalence of digestive disorders, rising awareness around gut microbiome health, and growing adoption of preventive nutritional supplementation across adult and geriatric populations. Expanding demand for plant-based, allergen-free, and clinically validated probiotic formulations is further accelerating global revenue expansion.

Key Market Insights

- Probiotic-based gentle digestion formulas dominate the global market, accounting for nearly 38% of 2025 revenue, supported by strong clinical backing and high consumer awareness.

- Plant-based and allergen-free formulations are rapidly gaining traction, driven by rising lactose intolerance and vegan dietary preferences worldwide.

- North America leads the global market, contributing approximately 34% of total revenue in 2025, with the United States representing the largest national market.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR, fueled by increasing middle-class income and preventive healthcare adoption.

- Retail pharmacies and drugstores remain the dominant distribution channel, accounting for around 35% of global sales.

- Technological innovation in microencapsulation and multi-strain probiotic blends is improving product efficacy, shelf stability, and consumer confidence.

What are the latest trends in the gentle digestion formula market?

Rise of Personalized Gut Health Solutions

Personalized digestive nutrition is emerging as a major trend in the global market. Companies are increasingly leveraging microbiome research, AI-driven dietary analysis, and at-home gut testing kits to create customized probiotic and enzyme blends. Subscription-based delivery models are strengthening brand loyalty and recurring revenue streams. Consumers are seeking targeted solutions for IBS, lactose intolerance, bloating, and food sensitivities, encouraging manufacturers to develop condition-specific gentle digestion formulations. This shift toward personalization is also supporting premium pricing strategies and differentiation in a competitive supplement landscape.

Plant-Based and Clean-Label Innovation

Demand for plant-based and clean-label digestive formulas is reshaping product development strategies. Manufacturers are increasingly replacing dairy-based carriers with oat, almond, soy, and pea protein bases to cater to vegan and lactose-intolerant consumers. Clean-label claims such as non-GMO, gluten-free, and preservative-free are becoming standard expectations rather than premium differentiators. Botanical ingredients including ginger, peppermint, and fennel extracts are being integrated into formulations to align with consumer preference for natural digestive remedies. This trend is particularly strong in Europe and North America, where consumers prioritize transparency and sustainability.

What are the key drivers in the gentle digestion formula market?

Increasing Prevalence of Digestive Disorders

Rising incidence of digestive health issues such as irritable bowel syndrome (IBS), lactose intolerance, and functional gastrointestinal disorders is a primary growth driver. Urban dietary habits, stress, and processed food consumption are contributing to increased digestive discomfort, encouraging consumers to adopt gentle digestion supplements as preventive and therapeutic support solutions.

Growing Aging Population

The expanding global geriatric population is significantly influencing demand. Reduced natural enzyme production and weakened gut microbiota among elderly individuals increase reliance on enzyme-based and probiotic digestive formulas. This demographic shift is creating stable, long-term demand for clinically validated formulations.

Shift Toward Preventive Healthcare

Consumers are increasingly incorporating supplements into daily routines as part of preventive wellness strategies. Post-pandemic health awareness has strengthened focus on immunity and gut health, reinforcing steady adoption across adult populations.

What are the restraints for the global market?

Regulatory Fragmentation

Regulatory frameworks for probiotics and dietary supplements vary across countries, increasing compliance complexity and time-to-market delays. Strain-specific documentation and labeling requirements pose challenges for global expansion.

Price Sensitivity in Emerging Markets

Premium multi-strain and clinically tested products often carry higher price points, limiting accessibility in price-sensitive markets. This can restrict broader penetration in lower-income demographics.

What are the key opportunities in the gentle digestion formula industry?

Expansion in Emerging Economies

Asia-Pacific and Latin America present significant untapped growth opportunities. Rising disposable incomes, increasing healthcare awareness, and expanding e-commerce penetration are enabling broader access to digestive health supplements. Localization strategies, including region-specific herbal blends and affordable pack sizes, can accelerate adoption.

Integration with Functional Foods & Beverages

Incorporating gentle digestion blends into fortified beverages, nutrition bars, and dairy alternatives presents cross-category growth opportunities. Functional food manufacturers are increasingly integrating probiotics and digestive enzymes to meet consumer demand for convenient wellness solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5080 Million |

| Market Size in 2026 | USD 5481.32 Million |

| Market Size in 2031 | USD 8016.64 Million |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Probiotic-based gentle digestion formulas dominate the global digestive health supplements market, accounting for approximately 38% of total market share in 2025. The leadership of this segment is primarily driven by strong clinical validation supporting probiotic efficacy in maintaining gut microbiota balance, improving digestive comfort, and enhancing immune health. Increasing physician recommendations, widespread consumer familiarity, and growing awareness of the gut–brain axis further reinforce adoption across adult and pediatric populations. The rising prevalence of irritable bowel syndrome (IBS), bloating, and antibiotic-associated digestive disturbances continues to accelerate probiotic demand globally.

Enzyme-based digestive formulas represent a substantial secondary segment, supported by increasing incidences of lactose intolerance and protein digestion sensitivities. Lactase, protease, and amylase supplements are widely consumed by individuals seeking immediate symptom relief from dairy or high-protein diets. Meanwhile, synbiotic formulations that combine probiotics with prebiotics are gaining strong momentum due to their dual-action benefits in enhancing microbial survival and colonization in the gut. Consumers are increasingly drawn to scientifically advanced formulations that promise superior microbiome support. Herbal and botanical digestive blends are expanding steadily, particularly in Europe and Asia-Pacific, where traditional herbal medicine systems and natural remedy preferences are deeply rooted. Ingredients such as ginger, peppermint, fennel, and turmeric are being integrated into modern supplement formats to align with clean-label and plant-based trends.

Formulation Insights

Plant-based formulations account for approximately 34% of the global market in 2025, emerging as the leading formulation category due to rising veganism, sustainability awareness, and consumer preference for naturally sourced ingredients. The growing shift toward plant-forward diets has increased demand for digestive support tailored to fiber-rich and plant-protein-heavy consumption patterns. Manufacturers are innovating with non-GMO, soy-free, and dairy-free probiotic strains to align with evolving dietary lifestyles.

Allergen-free specialty formulas, including lactose-free, gluten-free, and non-dairy variants, are witnessing accelerated growth across pediatric and adult segments. The increasing diagnosis of celiac disease, gluten sensitivity, and food intolerances has significantly strengthened demand for specialized digestive solutions. Additionally, clean-label transparency and free-from certifications are influencing purchase decisions, particularly in developed markets where ingredient scrutiny is high.

Dosage Form Insights

Powdered formulations lead the market with nearly 31% share in 2025, primarily driven by their flexible dosing capabilities and suitability for infants, children, and elderly consumers who may have difficulty swallowing tablets or capsules. Powder formats allow for easy mixing into beverages, infant formula, or food, improving compliance and customization of dosage strength. Their extended shelf stability and suitability for high-potency probiotic strains further support segment leadership.

Capsules and tablets continue to maintain strong adoption among adult consumers due to convenience, portability, and precise dosage control. Delayed-release capsule technologies that ensure targeted intestinal delivery are contributing to sustained demand. Additionally, chewables and gummies are gaining popularity in pediatric and lifestyle-focused segments, reflecting innovation in palatable and user-friendly supplement formats.

Distribution Channel Insights

Retail pharmacies and drugstores dominate distribution, contributing nearly 35% of global sales in 2025. The segment’s leadership is driven by high consumer trust in pharmacists, access to professional guidance, and strong in-store product visibility. Pharmacist recommendations and doctor referrals significantly influence purchasing behavior, particularly for clinically validated probiotic products and specialized digestive formulations.

E-commerce platforms represent the fastest-growing channel, supported by subscription-based models, personalized supplement recommendations, digital health marketing, and broader product availability. The growth of direct-to-consumer brands and online health marketplaces has enhanced accessibility, especially in emerging economies where physical retail penetration may be limited. Online reviews, influencer endorsements, and educational content are playing an increasingly influential role in consumer decision-making.

Age Group Insights

Adults aged 13–59 years account for approximately 46% of global demand in 2025, making them the largest consumer group. This dominance is primarily driven by rising stress levels, irregular dietary habits, increased consumption of processed foods, and sedentary lifestyles that contribute to digestive discomfort. Preventive health trends and growing awareness of gut health’s link to immunity and mental wellness further stimulate demand within this demographic.

The geriatric segment is expanding steadily due to increased digestive sensitivity, slower metabolism, polypharmacy-related gut imbalances, and greater adoption of preventive supplementation. Pediatric demand is also rising as parents prioritize early-life microbiome development and immunity support, particularly in developed markets with strong pediatric health awareness.

Explore more data points, trends and opportunities Download Free Sample Report

Gentle Digestion Formula Market Segmentations

By Product Type

- Probiotic-Based Gentle Digestion Formulas

- Prebiotic-Based Formulas

- Synbiotic Formulas (Probiotic + Prebiotic)

- Enzyme-Based Digestive Formulas

- Herbal/Botanical Digestive Blends

- Low-FODMAP & Hypoallergenic Nutrition Formulas

By Formulation Type

- Dairy-Based Formulas

- Plant-Based Formulas (Soy, Almond, Oat, Pea)

- Allergen-Free & Specialty Medical Formulas

By Dosage Form

- Powdered Formulas

- Ready-to-Drink (RTD) Liquids

- Capsules & Tablets

- Sachets/Stick Packs

- Gummies & Chewables

By Age Group

- Infant (0–2 Years)

- Pediatric (3–12 Years)

- Adult (13–59 Years)

- Geriatric (60+ Years)

By Distribution Channel

- Hospital & Clinical Pharmacies

- Retail Pharmacies & Drugstores

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- E-commerce Platforms

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, making it the leading regional market. The United States contributes nearly 28% of global revenue, supported by high dietary supplement penetration, strong consumer awareness of probiotic benefits, and advanced retail infrastructure. Growth in the region is driven by increasing gastrointestinal disorder prevalence, rising preventive healthcare spending, strong presence of established supplement manufacturers, and widespread availability of clinically researched probiotic strains. Canada demonstrates steady expansion due to regulatory clarity, rising clean-label demand, and growing adoption of natural health products.

Europe

Europe accounts for roughly 27% of the global market in 2025, with Germany, the United Kingdom, and France leading regional consumption. Growth is fueled by strong preference for botanical and clean-label digestive formulations, expanding vegan populations, and heightened focus on preventive healthcare. Stringent regulatory oversight enhances product quality standards and strengthens consumer trust. Increasing aging populations across Western Europe and rising awareness of microbiome research are further contributing to sustained demand.

Asia-Pacific

Asia-Pacific represents about 24% of global revenue and is the fastest-growing region, expanding at over 9% CAGR. China and India serve as major growth engines due to rapid urbanization, expanding middle-class income, rising digestive health awareness, and growing e-commerce penetration. Increasing incidence of gastrointestinal infections and dietary transitions toward processed foods are boosting supplement adoption. Japan remains a mature probiotic market characterized by strong consumer education, established functional food culture, and steady demand for scientifically validated formulations.

Latin America

Latin America contributes approximately 7% of global revenue, led by Brazil and Mexico. Market growth is driven by improving healthcare awareness, rising disposable income, expanding retail pharmacy chains, and increasing demand for affordable digestive supplements. Urban population growth and gradual expansion of organized retail infrastructure are supporting market penetration across major metropolitan areas.

Middle East & Africa

The Middle East & Africa region accounts for nearly 8% of global demand, with the United Arab Emirates and Saudi Arabia leading market expansion. Growth is supported by rising healthcare expenditure, increasing lifestyle-related digestive issues, expanding modern retail channels, and growing imports of premium international supplement brands. Greater awareness of preventive wellness and improved regulatory frameworks in Gulf Cooperation Council countries are further strengthening regional market prospects.

Key Players in the Gentle Digestion Formula Market

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Reckitt Benckiser Group plc

- Pfizer Inc.

- Procter & Gamble Co.

- Amway Corp.

- Herbalife Ltd.

- Glanbia plc

- Bayer AG

- DSM-Firmenich

- Yakult Honsha Co., Ltd.

- BioGaia AB

- Church & Dwight Co., Inc.

- Himalaya Wellness Company