Functional Native Starch Market Size

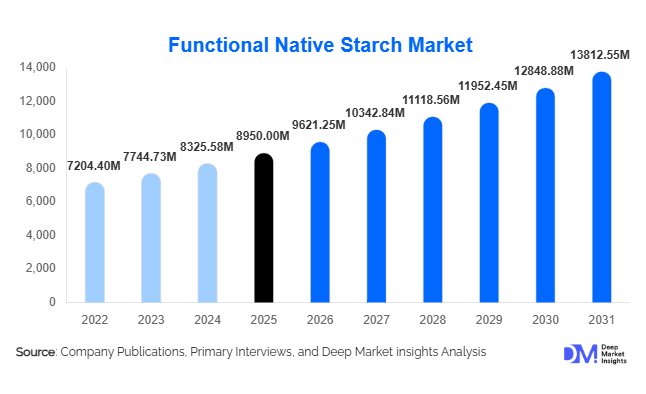

According to Deep Market Insights, the global functional native starch market size was valued at USD 8,950 million in 2025 and is projected to grow from USD 9,621.25 million in 2026 to reach USD 13,812.55 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The functional native starch market growth is primarily driven by rising clean-label ingredient demand, regulatory preference for minimally processed food additives, and expanding applications across processed food, biodegradable packaging, and plant-based formulations.

Key Market Insights

- Food & beverages account for over 62% of global demand, driven by bakery, dairy alternatives, sauces, and convenience foods.

- Corn-based native starch dominates with nearly 45% market share, supported by strong wet milling infrastructure in the U.S., China, and Brazil.

- Asia-Pacific leads global consumption with approximately 32% share, fueled by processed food expansion in China and India.

- Direct B2B sales represent nearly 68% of distribution, reflecting long-term contracts between starch manufacturers and industrial processors.

- Bioplastics and sustainable packaging applications are growing at a 9–10% CAGR, outpacing traditional food uses.

- The top five companies control around 42% of global revenue, indicating moderate market consolidation.

What are the latest trends in the functional native starch market?

Clean-Label Reformulation Accelerating Adoption

Global food manufacturers are reformulating products to eliminate chemically modified starches and artificial additives. Functional native starch, processed through physical methods such as heat-moisture treatment and pregelatinization, offers enhanced performance while retaining clean-label status. Retail audits indicate that over one-third of new packaged food launches in 2025 emphasized natural or minimally processed ingredients. This shift is particularly evident in Europe and North America, where regulatory scrutiny and consumer awareness are strongest. As a result, native starch is increasingly replacing modified starch in sauces, ready meals, and plant-based dairy alternatives.

Expansion into Bioplastics and Sustainable Materials

Growing regulatory restrictions on single-use plastics are opening new growth avenues for starch-based biodegradable materials. Native starch serves as a critical feedstock in compostable films, molded packaging, and bio-based polymers. Southeast Asian cassava starch exporters, particularly Thailand and Vietnam, are strengthening global supply chains to meet rising export demand. Manufacturers are forming partnerships with sustainable packaging companies to diversify revenue streams beyond food applications, positioning starch as a strategic raw material in the circular bioeconomy.

What are the key drivers in the functional native starch market?

Growth of Processed and Convenience Foods

Urbanization and rising disposable incomes are expanding demand for ready-to-eat meals, snacks, and packaged foods. Functional native starch provides thickening, binding, and moisture retention properties essential for product stability. Global processed food output expanded by approximately 6% in 2025, directly increasing starch consumption across industrial food production facilities.

Rising Demand in Plant-Based and Dairy Alternatives

The rapid growth of plant-based beverages, yogurts, and meat alternatives is strengthening demand for rice, tapioca, and potato native starch. These starches improve texture and mouthfeel while supporting allergen-free and gluten-free positioning. The plant-based food industry is expanding at over 8% annually, creating sustained ingredient demand.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in corn and cassava prices, influenced by climate variability and biofuel production, directly impact production costs. Price spikes reduce manufacturer margins and create procurement challenges for long-term contracts.

Competition from Modified Starch and Hydrocolloids

Modified starches and alternative hydrocolloids offer superior resistance to extreme processing conditions such as high shear and low pH environments. In certain industrial applications, these alternatives limit complete substitution by native starch, posing a competitive restraint.

What are the key opportunities in the functional native starch industry?

Emerging Market Processing Expansion

India, Indonesia, Vietnam, Nigeria, and Egypt are witnessing rapid packaged food growth. Investment in agro-processing infrastructure and food parks is increasing the demand for industrial starch inputs. Government-backed initiatives such as “Make in India” and “Made in China 2026” are encouraging domestic ingredient manufacturing capacity expansion.

Vertical Integration in Cassava and Corn Supply Chains

Manufacturers are investing in upstream farming partnerships and integrated wet milling facilities to stabilize raw material costs. Vertical integration improves margins (typically 12–18%) and enhances export competitiveness, particularly in the Asia-Pacific.

Here is your optimized, expanded, and more analytical version of the requested sections. The structure is maintained while strengthening strategic insights, adding clear growth drivers for each region, and reinforcing leading segment drivers in a natural and professional tone.

Source Insights

Corn-based functional native starch continues to lead the global market, accounting for approximately 45% share in 2025. Its dominance is primarily driven by large-scale availability, cost competitiveness, and well-established wet milling infrastructure across major agricultural economies such as the United States, China, and Brazil. The abundance of corn supply ensures pricing stability relative to other botanical sources, making it the preferred option for large-volume food processors. Additionally, continuous investments in yield optimization, contract farming, and vertically integrated supply chains further strengthen corn starch’s leadership position.

Cassava (tapioca) starch holds the second-largest share, supported by strong export-oriented production hubs in Thailand, Vietnam, and Indonesia. Cassava’s non-GMO positioning, gluten-free appeal, and neutral flavor profile make it particularly attractive for clean-label and allergen-free applications in bakery and dairy alternatives. The competitive labor costs and favorable agro-climatic conditions in Southeast Asia reinforce cassava’s supply advantage in global trade.

Application Insights

Food & beverages remain the dominant application segment, accounting for nearly 62% of global market share. The segment’s leadership is driven by expanding processed food consumption, convenience meal demand, and clean-label reformulation initiatives. Bakery and confectionery represent a substantial share within this category, as native starch plays a critical role in moisture retention, crumb structure improvement, viscosity control, and shelf-life extension. Increasing demand for ready-to-eat meals, sauces, soups, and dairy alternatives is further strengthening starch utilization across both developed and emerging markets.

Industrial applications, particularly biodegradable packaging and bio-based adhesives, are the fastest-growing segment, expanding at nearly 10% CAGR. Regulatory bans on single-use plastics, sustainability mandates, and investments in bio-economy infrastructure are accelerating demand for starch-based polymers and compostable materials. This diversification into non-food applications is strategically important for market participants seeking higher-margin opportunities.

Distribution Channel Insights

Direct B2B contracts dominate the functional native starch market with approximately 68% share, as multinational food processors and industrial manufacturers secure long-term supply agreements to mitigate raw material price volatility. These contracts ensure stable procurement volumes, quality consistency, and pricing predictability, particularly in high-demand segments such as bakery, dairy, and convenience foods.

Distributors and specialty ingredient suppliers play a critical role in serving mid-sized and regional food manufacturers that lack direct procurement scale. These intermediaries provide technical formulation support and smaller shipment volumes, enhancing market accessibility. Online B2B procurement platforms are gradually expanding, particularly in emerging markets such as India, Southeast Asia, and Latin America. Digitalization of ingredient sourcing is improving transparency, shortening procurement cycles, and enabling small manufacturers to access diversified starch portfolios.

| By Source | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 32% of the global market in 2025, making it the largest and fastest-growing regional market. China accounts for nearly 18% of worldwide demand, supported by its extensive processed food industry, large-scale corn milling infrastructure, and expanding dairy alternative segment. Government-backed agro-processing initiatives and export competitiveness reinforce China’s production leadership.

India is the fastest-growing major market, expanding at a 9–10% CAGR, driven by rapid urbanization, rising disposable incomes, expansion of organized retail, and significant public investments in food processing parks under industrial development programs. Growing demand for packaged snacks, ready meals, and pharmaceutical manufacturing is further strengthening domestic starch consumption. Thailand and Vietnam serve as leading cassava starch exporters, benefiting from favorable climate conditions, cost-efficient farming, and strong trade linkages with China, Japan, and Europe. The region’s growth is primarily driven by expanding processed food exports, increasing domestic consumption, and rising investments in biodegradable material manufacturing.

North America

North America represents around 28% of global market share, led by the United States, which contributes nearly 24% of total global consumption. Strong domestic corn production, vertically integrated agribusiness giants, and advanced wet milling capabilities ensure supply stability. A major growth driver in the region is the accelerating clean-label reformulation trend across packaged food brands, particularly in bakery, dairy alternatives, and frozen foods. Additionally, rising demand for plant-based meat and dairy substitutes is significantly increasing native starch utilization. Regulatory clarity from food safety authorities and strong R&D investments by ingredient manufacturers further strengthen regional innovation capacity.

Europe

Europe demonstrates steady growth at approximately 6% CAGR, supported by stringent regulatory standards that favor natural and minimally processed ingredients. Germany, France, and the Netherlands are key demand centers due to strong bakery, dairy, and processed food industries. Growth in Europe is primarily driven by strict labeling requirements, sustainability commitments under EU bio-economy strategies, and rising adoption of starch-based biodegradable materials. Additionally, consumer preference for gluten-free and allergen-friendly products supports increased use of potato and specialty starch variants.

Latin America

Brazil and Mexico drive regional demand, supported by robust corn processing industries and expanding processed food exports to North America and Europe. Brazil benefits from strong agricultural output and an integrated agribusiness infrastructure, enabling competitive starch production. Regional growth is further supported by rising domestic consumption of convenience foods, improving food manufacturing capabilities, and increasing participation in global supply chains.

Middle East & Africa

Demand in the Middle East & Africa is expanding steadily due to rapid urbanization, population growth, and increasing reliance on imported processed foods. Nigeria and South Africa are emerging as growth hubs for processed food manufacturing and pharmaceutical production. Growth drivers in the region include rising packaged food imports, expanding supermarket penetration, and investments in local agro-processing facilities. Additionally, Africa’s cassava cultivation potential presents long-term opportunities for regional starch production and export diversification.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Functional Native Starch Market

- Cargill

- Ingredion Incorporated

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Roquette Frères

- Tereos Group

- AGRANA Beteiligungs-AG

- Grain Processing Corporation

- Avebe

- Südzucker AG

- Emsland Group

- Global Bio-Chem Technology Group

- Thai Wah Public Company Limited

- Manildra Group

- Viscofan