Functional Foods and Drinks Market Size

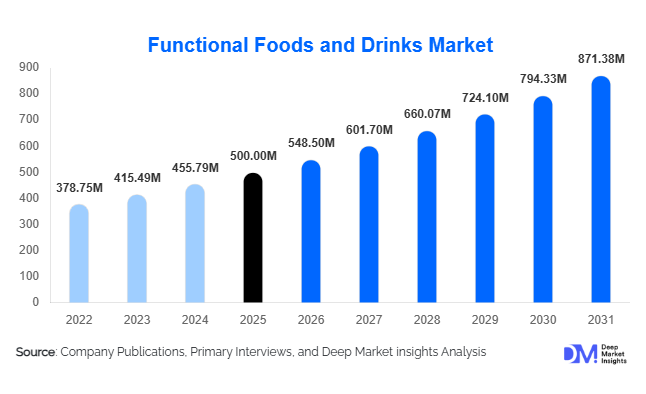

According to Deep Market Insights, the global functional foods and drinks market size was valued at USD 500.0 billion in 2025 and is projected to grow from USD 548.50 billion in 2026 to reach USD 871.38 billion by 2031, expanding at a CAGR of 9.7% during the forecast period (2026–2031). The market growth is primarily driven by increasing consumer awareness of preventive healthcare, rising demand for immunity-boosting products, and the rapid expansion of fortified and functional beverage categories. The integration of bioactive ingredients such as probiotics, vitamins, and plant-based extracts into everyday diets is transforming functional foods and drinks from niche offerings into mainstream consumption staples.

Key Market Insights

- Functional beverages dominate the market, accounting for over 50% share due to convenience and rapid nutrient absorption.

- Probiotics and prebiotics are the leading ingredient segment, driven by increasing awareness of gut health and immunity.

- North America leads the global market, supported by strong innovation, premium product adoption, and high consumer awareness.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable income, and growing health consciousness.

- E-commerce is rapidly transforming distribution channels, contributing significantly to global sales expansion.

- Plant-based and clean-label products are gaining strong traction, especially among younger and environmentally conscious consumers.

What are the latest trends in the functional foods and drinks market?

Rise of Personalized and Preventive Nutrition

The market is witnessing a shift toward personalized nutrition solutions tailored to individual health needs. Consumers are increasingly seeking products aligned with specific health goals such as immunity, gut health, cognitive performance, and weight management. Advances in digital health technologies, wearable devices, and microbiome research are enabling companies to offer customized functional food solutions. Subscription-based models and direct-to-consumer channels are further supporting this trend, allowing brands to build long-term consumer relationships. This movement toward preventive healthcare is significantly reshaping product innovation and marketing strategies.

Expansion of Plant-Based and Clean-Label Products

Consumers are actively shifting toward plant-based functional foods and beverages due to sustainability concerns and dietary preferences. Ingredients such as plant proteins, herbal extracts, and algae-based nutrients are gaining popularity. Clean-label products, free from artificial additives and preservatives, are also becoming a key purchasing factor. Manufacturers are investing in transparent labeling and sustainable sourcing practices to meet evolving consumer expectations. This trend is particularly strong in urban markets and among younger demographics, driving innovation across multiple product categories.

What are the key drivers in the functional foods and drinks market?

Growing Prevalence of Lifestyle Diseases

The increasing incidence of chronic diseases such as obesity, diabetes, and cardiovascular disorders is a major driver of market growth. Consumers are proactively adopting functional foods and drinks as part of their daily diet to manage health risks. Governments and healthcare organizations are also promoting preventive nutrition, further accelerating demand.

Increasing Awareness of Immunity and Gut Health

Post-pandemic consumer behavior has significantly shifted toward immunity-boosting and gut health products. Functional ingredients such as probiotics, vitamins, and antioxidants are witnessing strong demand globally. This has led to increased product launches and innovation in fortified foods and beverages.

Demand for Convenient Nutrition Solutions

Modern lifestyles are driving demand for ready-to-consume and on-the-go nutrition products. Functional beverages, snack bars, and meal replacements are gaining popularity due to their convenience and health benefits. This trend is particularly prominent among working professionals and urban populations.

What are the restraints for the global market?

High Product Costs

Functional foods and drinks often involve premium ingredients and advanced processing technologies, leading to higher product prices. This limits adoption in price-sensitive markets and creates challenges for widespread penetration.

Regulatory and Labeling Challenges

Strict regulations regarding health claims and labeling standards across different regions pose challenges for manufacturers. Compliance with varying regulatory frameworks increases operational complexity and costs, potentially slowing market growth.

What are the key opportunities in the functional foods and drinks industry?

Emerging Market Expansion

Rapid urbanization and rising disposable incomes in emerging economies such as India, China, and Brazil present significant growth opportunities. Increasing awareness of health and wellness is driving demand for functional products in these regions, supported by government initiatives promoting nutrition and food fortification.

Technological Advancements in Food Processing

Innovations in food technology, such as microencapsulation and enhanced nutrient delivery systems, are improving the stability and effectiveness of functional ingredients. These advancements enable manufacturers to develop products with better taste, longer shelf life, and higher bioavailability, enhancing consumer acceptance.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 500.00 Million |

| Market Size in 2026 | USD 548.50 Million |

| Market Size in 2031 | USD 871.38 Million |

| CAGR | 9.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product type landscape of the global functional food and beverage market is strongly dominated by functional beverages, which are projected to hold approximately 52% of the total market share in 2025. This leadership position is primarily driven by shifting consumer lifestyles that increasingly favor convenience, portability, and instant nutritional benefits. Functional beverages, including energy drinks, fortified juices, enhanced waters, and probiotic drinks, have become a staple in modern consumption patterns as they seamlessly integrate into busy daily routines. The leading segment driver for functional beverages is the growing demand for ready-to-drink health solutions that deliver targeted benefits such as energy enhancement, immunity support, and digestive health without requiring preparation.Within this category, energy drinks continue to capture significant demand among young adults and working professionals seeking improved alertness and productivity. Fortified juices are gaining traction among health-conscious consumers looking for natural sources of vitamins, while probiotic beverages are increasingly preferred for their digestive and gut health benefits. The continuous innovation in flavors, formulations, and packaging further enhances consumer appeal, reinforcing the segment’s dominance.Functional foods, although secondary to beverages, maintain a stable and expanding presence in the market. Products such as fortified cereals, dairy-based offerings like yogurt and cheese, and functional snack bars are widely consumed due to their integration into everyday diets. The key growth driver for this segment lies in the ease of incorporating health benefits into traditional meal structures, allowing consumers to improve nutrition without altering eating habits significantly. Additionally, dietary supplements in food form, including protein powders, meal replacements, and fortified snacks, are witnessing rising demand among fitness enthusiasts and individuals pursuing weight management or muscle-building goals. This sub-segment benefits from the increasing popularity of personalized nutrition and lifestyle-based dietary planning.

Ingredient Insights

The ingredient segment is characterized by the dominance of probiotics and prebiotics, which together account for approximately 28% of the total market share. The leading segment driver here is the increasing global awareness of gut health and its direct correlation with overall well-being, including immunity, mental health, and metabolic function. Consumers are actively seeking products that support digestive balance, which has led to widespread incorporation of these ingredients across beverages, dairy products, and dietary supplements.Vitamins and minerals also represent a significant portion of the market, driven by their essential role in addressing nutrient deficiencies and supporting preventive healthcare. Their widespread use in food fortification programs, particularly in emerging economies, has further strengthened their market presence. These micronutrients are commonly added to beverages, cereals, dairy products, and snacks, enabling manufacturers to position products as health-enhancing and functional.Emerging ingredient categories such as plant-based proteins and botanical extracts are experiencing accelerated growth, fueled by evolving consumer preferences toward natural, sustainable, and clean-label products. Plant-based proteins derived from sources like pea, soy, and rice are increasingly utilized in both food and beverage formulations, catering to vegan and flexitarian populations. Botanical extracts, including adaptogens and herbal ingredients, are gaining popularity for their perceived holistic health benefits, such as stress reduction, improved cognitive function, and enhanced immunity. The shift toward transparency, sustainability, and minimally processed ingredients continues to shape innovation within this segment.

Distribution Channel Insights

Distribution channels play a critical role in determining market accessibility and consumer reach, with supermarkets and hypermarkets accounting for nearly 40% of global sales. The leading driver for this segment is the consumer preference for one-stop shopping destinations that offer a wide variety of products under a single roof. These retail formats provide strong visibility for functional food and beverage brands, supported by in-store promotions, product placements, and established consumer trust.Despite the dominance of traditional retail, online retail is emerging as the fastest-growing distribution channel, contributing over 18% of total sales. The primary growth driver for this segment is the increasing penetration of e-commerce platforms and the convenience they offer in terms of home delivery, product comparison, and access to niche or specialized products. Direct-to-consumer models are further accelerating growth, enabling brands to build stronger relationships with consumers and offer personalized product recommendations.Specialty stores and pharmacies also hold an important position in the distribution landscape, particularly for premium and health-focused products. These channels are often perceived as more credible sources for nutritional and functional products, especially those targeting specific health conditions. The presence of knowledgeable staff and curated product assortments enhances consumer confidence and supports the growth of high-value segments such as clinical nutrition and dietary supplements.

Consumer Group Insights

In terms of consumer segmentation, adults represent the largest group, accounting for approximately 55% of total market demand. The leading driver for this segment is the increasing emphasis on preventive healthcare and wellness among working-age populations. Adults are actively seeking products that help manage stress, boost immunity, improve energy levels, and support overall health, making them the primary consumers of functional foods and beverages.Athletes and fitness enthusiasts constitute another significant consumer group, driving demand for high-protein, performance-enhancing, and recovery-focused products. The growing popularity of fitness culture, gym memberships, and sports activities has led to increased consumption of protein supplements, energy drinks, and functional snacks designed to enhance physical performance and endurance.The geriatric population is also emerging as a key contributor to market growth, particularly in the clinical nutrition segment. As aging populations increase globally, there is a rising need for products that address age-related health concerns such as bone health, cardiovascular conditions, and cognitive decline. Functional foods and beverages tailored to these needs are gaining traction, supported by advancements in nutritional science and product formulation.

End-Use Insights

From an end-use perspective, household consumption dominates the market, contributing over 60% of total demand. The leading driver for this segment is the growing integration of functional foods and beverages into daily dietary routines. Consumers are increasingly adopting healthier lifestyles, leading to higher consumption of fortified and functional products within the home environment.The sports nutrition segment is the fastest-growing category, with a CAGR exceeding 11%. This growth is primarily driven by rising fitness awareness, increasing participation in sports and physical activities, and the influence of social media on health and wellness trends. Products such as protein powders, energy bars, and electrolyte drinks are witnessing strong demand among both professional athletes and recreational fitness enthusiasts.Clinical nutrition is another expanding segment, supported by increasing healthcare needs and the prevalence of chronic diseases. Functional products designed for medical or therapeutic purposes are gaining importance, particularly in hospital and elderly care settings. Additionally, export-driven demand remains strong in developed markets, where countries such as the United States, Germany, and Japan lead in the production and export of high-value functional products. These markets benefit from advanced research capabilities, strong regulatory frameworks, and high consumer awareness.

Explore more data points, trends and opportunities Download Free Sample Report

Functional Foods and Drinks Market Segmentations

By Product Type

- Functional Foods

- Functional Beverages

- Dietary Supplements

By Ingredient Type

- Probiotics & Prebiotics

- Proteins & Amino Acids

- Vitamins & Minerals

- Botanicals & Herbal Extracts

- Fibers & Carbohydrates

- Omega Fatty Acids

- Antioxidants

By Functionality

- Digestive Health

- Immunity Boosting

- Heart Health

- Weight Management

- Cognitive Health

- Energy & Endurance

- Bone & Joint Health

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Pharmacies & Drug Stores

By Consumer Group

- Children & Adolescents

- Adults

- Geriatric Population

- Athletes & Fitness Enthusiasts

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, making it the largest regional market. The United States leads the region, supported by a highly developed food and beverage industry, strong innovation capabilities, and high consumer awareness regarding health and wellness. The key drivers for regional growth include increasing demand for premium and personalized nutrition products, widespread adoption of functional beverages, and a strong presence of leading market players investing in research and development. Canada also contributes significantly, driven by rising demand for organic, clean-label, and plant-based products. Additionally, the region benefits from advanced distribution networks and high penetration of e-commerce platforms, further supporting market expansion.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of the global market share and is the fastest-growing region, with a CAGR exceeding 11%. The primary growth drivers include rapid urbanization, rising disposable incomes, and increasing health awareness among consumers. Countries such as China, India, and Japan are at the forefront of this growth, supported by large population bases and evolving dietary habits. The expansion of the middle class and growing interest in preventive healthcare are driving demand for functional foods and beverages. Additionally, traditional dietary practices in the region, which often emphasize natural and herbal ingredients, are aligning well with modern functional product trends, further accelerating market growth.

Europe

Europe holds around 25% of the global market, with key markets including Germany, the United Kingdom, and France. The region’s growth is driven by strong regulatory frameworks that ensure product quality and safety, as well as a high level of consumer awareness regarding nutrition and health. The leading drivers include increasing demand for clean-label, organic, and sustainably sourced products, as well as a growing preference for plant-based and functional ingredients. European consumers are particularly focused on transparency and traceability, prompting manufacturers to adopt sustainable practices and innovative formulations. The presence of established food and beverage companies further supports market development in this region.

Latin America

Latin America accounts for approximately 6% of the global market share, with Brazil and Mexico serving as key contributors. The region is experiencing steady growth driven by increasing health awareness and the expansion of the middle-class population. Rising urbanization and changing dietary habits are encouraging consumers to adopt functional foods and beverages as part of their daily routines. Additionally, the growing retail sector and improving distribution infrastructure are enhancing product accessibility. Local manufacturers are also introducing affordable functional products, making them accessible to a broader consumer base and supporting overall market growth.

Middle East & Africa

The Middle East & Africa region holds around 6% of the global market share, with the United Arab Emirates and South Africa leading demand. The primary growth drivers include rapid urbanization, increasing disposable incomes, and a growing focus on health and wellness. Consumers in the region are becoming more aware of the benefits of functional foods and beverages, leading to increased adoption. The expansion of modern retail formats, including supermarkets and hypermarkets, is improving product availability. Additionally, government initiatives promoting healthier lifestyles and the rising prevalence of lifestyle-related diseases are encouraging consumers to shift toward functional and fortified products, supporting long-term market growth.