Functional Food and Beverage Market Size

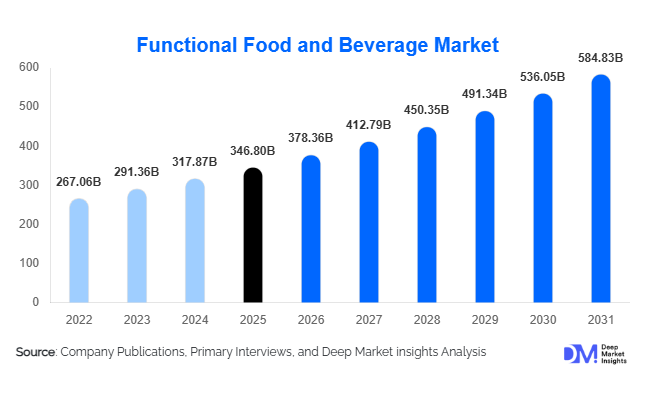

According to Deep Market Insights, the global functional food and beverage market size was valued at USD 346.8 billion in 2025 and is projected to grow from USD 378.36 billion in 2026 to reach USD 5784.83 billion by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer focus on preventive healthcare, increasing demand for nutrient-fortified products, and rapid innovation in probiotics, plant-based nutrition, and personalized wellness solutions. Functional foods and beverages are increasingly positioned as everyday health solutions rather than niche wellness products, supporting sustained global adoption across developed and emerging economies.

Key Market Insights

- Preventive health consumption is reshaping global food habits, with consumers prioritizing immunity, digestive health, and cognitive wellness benefits.

- Functional beverages represent the fastest-growing category, supported by energy drinks, probiotic beverages, and fortified hydration products.

- Asia-Pacific dominates global consumption due to strong functional ingredient traditions and expanding middle-class populations.

- Clean-label and plant-based innovation is accelerating product launches across dairy alternatives and fortified snacks.

- E-commerce and direct-to-consumer models are transforming product accessibility and personalized nutrition offerings.

- Scientific validation and regulatory approvals are becoming critical competitive differentiators among leading brands.

What are the latest trends in the functional food and beverage market?

Personalized Nutrition and Targeted Health Formulations

Functional food and beverage manufacturers are increasingly developing products tailored to specific health outcomes such as gut health, stress management, heart health, and metabolic balance. Advances in nutrigenomics and digital health tracking have enabled companies to introduce customized nutrition solutions aligned with individual lifestyles and biological needs. Subscription-based nutrition platforms are integrating AI-driven recommendations, allowing consumers to select products based on age, activity level, and health goals. This personalization trend is expanding premium product categories and strengthening long-term consumer engagement, particularly in urban markets where health awareness continues to rise.

Plant-Based Functional Innovation

The shift toward plant-based diets has accelerated innovation in fortified plant-derived foods and beverages. Manufacturers are incorporating functional ingredients such as adaptogens, botanical extracts, omega fatty acids, and plant proteins into dairy alternatives, snacks, and ready-to-drink beverages. Consumers increasingly associate plant-based formulations with sustainability and wellness, encouraging brands to reformulate traditional products with added functional benefits. The integration of functional claims alongside sustainability positioning is helping brands command premium pricing while appealing to environmentally conscious consumers.

What are the key drivers in the functional food and beverage market?

Rising Preventive Healthcare Awareness

Growing healthcare costs and lifestyle-related diseases have pushed consumers toward preventive nutrition. Functional foods enriched with probiotics, vitamins, minerals, and bioactive compounds are increasingly perceived as tools for long-term health maintenance. Governments and health organizations globally are promoting dietary improvements, further supporting demand for fortified everyday foods. The COVID-era emphasis on immunity continues to influence purchasing behavior, sustaining growth momentum even after pandemic disruptions.

Expansion of Functional Beverages

Functional beverages have emerged as a major growth engine due to convenience and rapid product innovation. Energy drinks, sports hydration products, kombucha, protein shakes, and fortified waters are gaining traction among younger demographics and working professionals. Beverage formats enable faster nutrient delivery and allow brands to introduce new formulations quickly, driving higher product turnover and market expansion. Innovation in low-sugar and natural ingredient formulations is further expanding consumer acceptance.

Technological Advancements in Food Processing

Advancements in encapsulation technology, fermentation processes, and bioavailability enhancement have improved the stability and effectiveness of functional ingredients. Manufacturers are now able to integrate sensitive nutrients such as probiotics and omega oils into mainstream products without compromising taste or shelf life. These innovations enable large-scale commercialization while maintaining product efficacy, significantly accelerating adoption across mass-market food categories.

What are the restraints for the global market?

Regulatory Complexity and Health Claim Restrictions

Functional foods face stringent regulatory scrutiny regarding health claims, ingredient approvals, and labeling standards. Variations across regions create compliance challenges for multinational companies, increasing product development timelines and certification costs. Scientific substantiation requirements can limit marketing flexibility and delay product launches.

High Product Pricing and Consumer Skepticism

Functional foods often carry premium pricing due to specialized ingredients and research investments. Price-sensitive consumers in developing economies may limit adoption despite growing awareness. Additionally, skepticism toward exaggerated health claims has encouraged consumers to demand transparency and clinical validation, increasing pressure on manufacturers to invest in scientific evidence.

What are the key opportunities in the functional food and beverage industry?

Emerging Market Expansion

Rapid urbanization and rising disposable incomes in Asia, Latin America, and parts of Africa present strong growth opportunities. Consumers in these regions are transitioning from traditional diets toward packaged nutrition products with added health benefits. Localized formulations incorporating traditional ingredients such as turmeric, ginseng, and herbal extracts offer significant potential for market penetration.

Integration of Functional Ingredients into Everyday Staples

Manufacturers are increasingly embedding functional ingredients into daily-consumption foods such as bread, cereals, dairy, and snacks. This strategy expands consumer reach beyond health enthusiasts and positions functional nutrition as part of routine eating habits. Fortified staples are expected to drive volume growth due to high consumption frequency.

Digital Health and Direct-to-Consumer Ecosystems

The convergence of nutrition and digital health platforms is enabling companies to build direct relationships with consumers. Online subscription models, personalized nutrition kits, and wellness apps create recurring revenue opportunities. Data-driven insights allow companies to refine product offerings and enhance customer retention while lowering dependence on traditional retail channels.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 346.80 Billion |

| Market Size in 2026 | USD 378.36 Billion |

| Market Size in 2031 | USD 584.83 Billion |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Functional beverages continue to lead the global functional foods and beverages market, accounting for approximately 34% of total revenue in 2025. Their dominance is driven by convenience, portability, and strong adoption among younger consumers seeking energy, hydration, and immunity benefits. The surge in on-the-go lifestyles, long working hours, and increased awareness of preventive health solutions has further accelerated demand. Functional dairy products follow closely, buoyed by growing popularity of probiotic yogurts, fortified milk, and plant-based alternatives that support digestive health, bone strength, and immunity. Functional bakery and cereals are witnessing steady growth as fiber-enriched and protein-fortified products gain preference among health-conscious consumers, while clean-label trends and fortification initiatives drive innovation. Functional snacks are increasingly replacing traditional snack foods, with consumers favoring nutrient-dense, low-sugar, and protein-rich alternatives. Across all product types, innovation, convenience, scientific validation of health benefits, and premiumization remain key growth drivers.

Ingredient Insights

Probiotics lead the ingredient landscape, contributing nearly 27% of global market share in 2025, fueled by rising awareness of gut health, the microbiome, and its connection to immunity, mental wellness, and overall vitality. Proteins and amino acids are expanding rapidly, driven by mainstream adoption of sports nutrition, high-protein diets, and functional beverages incorporating protein blends. Vitamins and minerals remain essential, widely used across beverages, dairy, cereals, and snacks to address nutrient deficiencies and promote general health. Emerging ingredients such as adaptogens, omega-3 fatty acids, plant extracts, and phytonutrients are driving innovation in immunity, cognitive wellness, stress relief, and cardiovascular health, appealing to consumers seeking holistic benefits beyond basic nutrition.

Health Benefit Insights

Digestive health applications dominate the market with a 29% share, supported by probiotics, prebiotics, and increasing consumer recognition of the gut-health link to overall wellness. Immunity-focused products experienced a significant surge following the COVID-19 pandemic and continue to see strong adoption, particularly in Asia-Pacific and North America. Cognitive health, stress-relief, and heart-health offerings are emerging as high-growth niches, reflecting the growing consumer preference for holistic wellness solutions. Weight management and metabolic health products are gaining traction, driven by rising obesity rates, sedentary lifestyles, and the increasing perception of functional nutrition as a preventive strategy. Personalization of health benefits through tailored formulations is also influencing consumer purchase decisions.

Distribution Channel Insights

Supermarkets and hypermarkets retain the largest share, accounting for approximately 41% of global sales in 2025, due to extensive product availability, trusted quality assurance, and the ability to offer bundled promotions. Convenience stores and modern trade outlets complement reach in urban centers, providing easy access to functional foods for busy consumers. Online retail channels are the fastest-growing segment, propelled by e-commerce platforms, subscription models, and direct-to-consumer strategies. Digital marketing campaigns, influencer collaborations, personalized nutrition apps, and mobile platforms allow brands to connect with health-conscious consumers, enhance engagement, and extend access beyond traditional retail networks, contributing significantly to regional market expansion.

End-Use Insights

Household consumption dominates the functional foods market, representing nearly 68% of total usage, as products become integrated into daily diets for preventive health and wellness. Sports and fitness applications represent the fastest-growing end-use segment, supported by rising gym memberships, adoption of fitness tracking technology, and the popularity of active lifestyles. Clinical nutrition and elderly care segments are also expanding steadily, driven by aging populations, rising healthcare awareness, and demand for specialized medical nutrition products. Export-driven consumption is notable for probiotic dairy and fortified beverages, with Asia-Pacific manufacturers increasingly supplying North American and European markets, leveraging trade agreements and consumer preference for high-quality functional imports.

Explore more data points, trends and opportunities Download Free Sample Report

Functional Food and Beverage Market Segmentations

By Product Type

- Functional Beverages

- Functional Dairy

- Functional Bakery & Cereals

- Functional Snacks

- Plant-Based Functional Foods

By Ingredient Type

- Probiotics

- Proteins & Amino Acids

- Vitamins & Minerals

- Omega Fatty Acids

- Botanical Extracts & Adaptogens

By Health Benefit

- Digestive Health

- Immunity Support

- Cognitive & Mental Health

- Cardiovascular Health

- Weight Management

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Online Retail & D2C Platforms

- Pharmacies & Drug Stores

- Convenience Stores

By End-Use

- Household Consumption

- Sports & Fitness Applications

- Clinical Nutrition & Healthcare

- Institutional & Foodservice Applications

Regional Insights

North America

North America accounted for around 29% of the global functional foods and beverages market in 2025, with the United States and Canada at the forefront. High consumer awareness of functional nutrition, well-established sports nutrition trends, and strong adoption of premium products drive regional leadership. Protein-enriched snacks, functional beverages, plant-based alternatives, and immunity-focused formulations dominate demand. Government health campaigns, preventive nutrition initiatives, and rising interest in lifestyle-related wellness further support growth. Advanced e-commerce infrastructure, direct-to-consumer platforms, and subscription-based models enhance accessibility. Innovation in ingredient combinations, clean-label offerings, and personalized nutrition solutions are major drivers, especially in urban and health-conscious demographics.

Europe

Europe captures nearly 24% of the global market, led by Germany, the U.K., France, and Nordic countries. The region benefits from strict regulatory standards that enhance trust in functional claims, high disposable incomes, and widespread adoption of health-conscious lifestyles. Probiotic dairy, fortified cereals, plant-based alternatives, and clean-label products are preferred. Government-led nutrition initiatives, focus on preventive health, and growing interest in personalized nutrition drive growth. Urbanization, modern retail networks, and a high rate of online shopping expand access to functional foods. Innovation in gut health, immunity support, and cognitive wellness products is particularly strong, with consumers increasingly seeking science-backed solutions and sustainable product options.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing market, accounting for roughly 32% of global consumption in 2025. China, Japan, India, and South Korea lead due to cultural acceptance of functional ingredients, rapid urbanization, rising disposable income, and increasing health awareness. Japan continues to pioneer innovation in beverages, dairy, and snacks, while India exhibits strong growth in fortified beverages, immunity-focused foods, and protein-enriched snacks. Expanding retail chains, e-commerce adoption, and government health programs contribute to rising consumption. Lifestyle-related health concerns, rising incidence of chronic diseases, and active promotion of preventive nutrition drive regional growth. Consumer trends toward functional foods for energy, immunity, and wellness benefits, coupled with growing youth and middle-class populations, create robust demand for both domestic and imported products.

Latin America

Latin America, led by Brazil and Mexico, is witnessing steady growth, driven by urbanization, expanding middle-class populations, and rising health awareness. Functional dairy products, fortified beverages, and protein-enriched snacks are gaining popularity as affordable wellness solutions. Local production and imports cater to diverse consumer preferences, while government nutrition campaigns, obesity prevention programs, and chronic disease awareness initiatives further stimulate demand. Retail expansion through supermarkets, hypermarkets, and modern trade, along with increasing online penetration, enhances access. Innovation in taste, convenience, and nutrient fortification is shaping consumer adoption, particularly among younger, urban populations seeking health-oriented alternatives.

Middle East & Africa

The Middle East and Africa market is witnessing consistent growth, driven by the UAE, Saudi Arabia, and South Africa. Increasing prevalence of lifestyle-related diseases, rising disposable incomes, and government-led nutrition awareness initiatives encourage the consumption of fortified foods and functional beverages. Urbanization, exposure to international health trends, and expanding retail infrastructure further enhance market accessibility. Functional beverages, fortified dairy, and immunity-supporting products are key growth segments. Online retail channels are increasingly important, providing convenience and broader reach in urban and semi-urban areas. Rising health consciousness, combined with demand for premium, nutrient-dense, and ready-to-consume products, is fueling market expansion across both affluent and emerging urban segments.

Key Players in the Functional Food and Beverage Market

- Nestlé S.A.

- Danone S.A.

- PepsiCo Inc.

- The Coca-Cola Company

- Kellogg Company

- General Mills Inc.

- Yakult Honsha Co., Ltd.

- Abbott Laboratories

- Herbalife Nutrition Ltd.

- Glanbia plc

- Arla Foods amba

- Unilever PLC

- Meiji Holdings Co., Ltd.

- Mondelez International Inc.

- Otsuka Holdings Co., Ltd.