Functional Flours Market Size

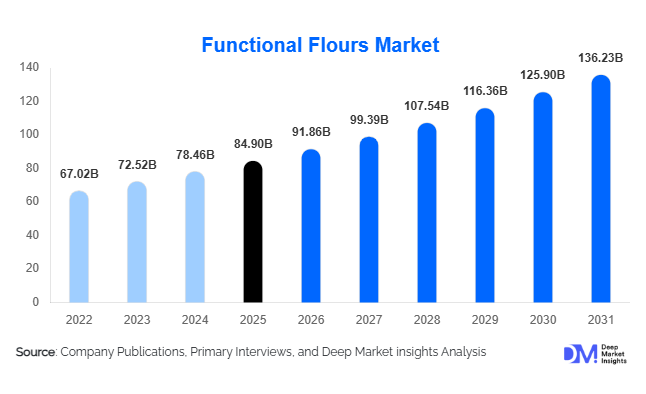

According to Deep Market Insights, the global functional flours market size was valued at USD 84.9 billion in 2025 and is projected to grow from USD 91.86 billion in 2026 to reach USD 136.23 billion by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The functional flours market growth is primarily driven by rising consumer demand for clean-label and fortified food products, increasing adoption of gluten-free and plant-based diets, and expanding applications of specialty flour ingredients across bakery, convenience food, sports nutrition, and processed food industries.

Key Market Insights

- Functional flour demand is increasingly shifting toward protein-enriched and clean-label formulations, particularly across bakery, snacks, and plant-based food applications.

- Pulse-based and gluten-free functional flours are witnessing rapid adoption globally, supported by rising vegan dietary trends and growing gluten intolerance awareness.

- North America dominates the global functional flours market, driven by strong penetration of healthy packaged foods and premium bakery products.

- Asia-Pacific remains the fastest-growing regional market, supported by rapid urbanization, rising processed food consumption, and government food fortification initiatives.

- Food manufacturers are increasingly investing in advanced flour processing technologies, including extrusion, enzymatic treatment, and fermentation-based flour enhancement systems.

- Functional flours are becoming essential ingredients in plant-based meat and dairy alternatives, where they improve texture, binding, moisture retention, and nutritional performance.

functional flours market latest trends

Clean-Label and Plant-Based Product Innovation Accelerating

The functional flours market is witnessing substantial growth in clean-label and plant-based ingredient innovation. Food manufacturers are increasingly replacing synthetic stabilizers and emulsifiers with multifunctional flour ingredients capable of improving texture, shelf life, and nutritional quality naturally. Pulse-based functional flours such as chickpea, lentil, pea, and fava bean flour are gaining traction due to their high protein and fiber content. This trend is particularly strong across North America and Europe, where consumers are demanding minimally processed foods with recognizable ingredients. Manufacturers are also introducing organic, non-GMO, and allergen-free functional flour variants to strengthen premium product positioning. Plant-based meat and dairy producers are heavily incorporating specialty flours to enhance structure, moisture retention, and sensory performance, further expanding market opportunities.

Advanced Processing Technologies Transforming Flour Functionality

Technological innovation is significantly reshaping the functional flours industry. Manufacturers are increasingly adopting extrusion technology, fermentation systems, micronization, and enzymatic modification techniques to improve flour digestibility, water absorption, texture stability, and nutritional retention. Fermented functional flours are gaining popularity in bakery and snack applications due to their ability to improve flavor profiles and shelf stability naturally. AI-supported formulation systems and automated milling technologies are also helping companies optimize ingredient consistency and reduce production waste. These innovations are enabling food companies to develop customized flour blends tailored for specific applications such as sports nutrition, gluten-free products, and protein-fortified convenience foods.

functional flours market drivers

Rising Demand for Health-Focused and Fortified Foods

Growing consumer awareness regarding nutrition and preventive healthcare is one of the primary growth drivers for the functional flours market. Consumers are increasingly seeking foods enriched with protein, fiber, vitamins, and minerals, particularly in urban markets where lifestyle-related disorders such as obesity and diabetes are increasing. Functional flours help food manufacturers improve nutritional profiles without significantly compromising texture or taste. The rising popularity of fortified bakery products, healthy snacks, protein bars, and meal replacements is accelerating demand for specialty flour ingredients globally. Government-supported nutritional fortification programs across Asia, Africa, and Latin America are also strengthening long-term market demand.

Rapid Expansion of Processed and Convenience Foods

The global processed food industry is expanding rapidly due to urbanization, rising disposable incomes, and changing consumer lifestyles. Functional flours are widely used in packaged foods, frozen meals, sauces, ready-to-cook products, and snacks to improve stability, moisture retention, and shelf life. Quick-service restaurants and industrial bakery manufacturers are increasingly integrating specialty flour blends into pizzas, tortillas, bread, and coated snacks to maintain product consistency and operational efficiency. The convenience food sector continues to expand strongly across emerging economies, particularly in India, China, Indonesia, and Brazil, supporting sustained growth for industrial flour applications.

global market restraints

Raw Material Price Volatility

The functional flours market remains highly sensitive to fluctuations in grain and pulse prices. Raw materials such as wheat, corn, chickpea, oats, sorghum, and rice are impacted by climate conditions, trade disruptions, geopolitical instability, and changing agricultural policies. Variability in crop yields and transportation costs creates pricing uncertainty for flour manufacturers and food processors. These fluctuations can compress profit margins, particularly for small and medium-sized ingredient suppliers that lack vertically integrated sourcing capabilities.

High Processing and Technology Costs

Advanced functional flour production requires substantial investments in extrusion equipment, fermentation systems, enzymatic treatment technologies, and precision milling infrastructure. Smaller producers often struggle to scale these advanced processing capabilities due to high capital expenditure requirements and technical complexity. Regulatory compliance related to food safety standards, allergen labeling, organic certification, and nutritional claims further increases operational costs for global manufacturers. These factors collectively create entry barriers and limit rapid expansion among smaller regional players.

functional flours industry key opportunities

Growth of Plant-Based and Alternative Protein Foods

The rapid expansion of the global plant-based food industry presents major opportunities for functional flour manufacturers. Pulse-based flours derived from chickpea, lentil, pea, and quinoa are increasingly used in vegan meat substitutes, dairy alternatives, and protein-enriched snacks due to their strong binding and nutritional properties. Food companies are actively reformulating products to align with consumer preferences for sustainable and protein-rich diets. This trend is expected to create sustained long-term demand for multifunctional flour systems optimized for plant-based food applications.

Emerging Market Food Fortification Programs

Governments across developing economies are increasing investments in food fortification initiatives aimed at reducing nutritional deficiencies. Functional flours enriched with iron, vitamins, minerals, and protein are increasingly being used in school meal programs, staple food production, and public nutrition schemes. Countries such as India, Nigeria, Indonesia, and Vietnam are witnessing rising demand for fortified processed foods due to expanding urban populations and growing middle-class consumption. Manufacturers establishing regional processing facilities in these markets are expected to benefit from strong domestic demand growth and export opportunities.

Product Type Insights

Specialty functional flours dominate the market, accounting for nearly 31% of global revenue in 2025. These products include gluten-free, fiber-enriched, organic, and protein-fortified flour variants widely used across premium bakery, healthy snack, and plant-based food applications. Pre-cooked functional flours are witnessing strong growth in convenience foods and instant meal products due to their rapid hydration and improved texture stability. Composite and multigrain flour blends are increasingly adopted by industrial bakeries and sports nutrition manufacturers seeking enhanced nutritional profiles. Resistant starch and fermented functional flours are also emerging as high-growth product categories due to rising demand for digestive health and clean-label solutions.

Application Insights

Bakery products remain the leading application segment, accounting for approximately 34% of global functional flour demand. Bread, cookies, tortillas, pizza crusts, and pastries increasingly utilize specialty flour ingredients to improve softness, moisture retention, nutritional value, and shelf stability. Convenience foods such as instant soups, frozen meals, ready-to-cook snacks, and coated products represent another major application area due to increasing urban food consumption. Functional flours are also gaining strong traction in plant-based meat and dairy alternatives, where they enhance binding, texture, and protein enrichment. Sports nutrition and clinical nutrition applications are emerging rapidly as manufacturers develop protein-enriched formulations targeted toward fitness-conscious consumers.

Distribution Channel Insights

B2B industrial sales dominate the global functional flours market, accounting for over 60% of total revenue. Large food processors, bakery manufacturers, snack producers, and convenience food companies remain the primary consumers of specialty flour ingredients globally. Ingredient distributors and wholesale channels continue playing a significant role in regional supply chain expansion, particularly in emerging markets. Online B2B procurement platforms are increasingly streamlining ingredient sourcing and improving transparency for industrial buyers. Direct-to-consumer sales and specialty health retail channels are also growing steadily due to rising consumer interest in gluten-free, organic, and protein-rich flour products for home cooking applications.

End-Use Industry Insights

The food processing industry represents the largest end-use segment for functional flours due to growing global demand for packaged and convenience foods. Industrial bakery and confectionery manufacturers are increasingly incorporating functional flour systems into premium baked goods to improve nutritional quality and shelf life. The plant-based food industry is emerging as one of the fastest-growing end-use segments, particularly across North America and Europe. Functional flours are also witnessing rising demand within the nutraceutical and sports nutrition industries, where high-protein and fortified formulations are gaining popularity. Export-driven demand from Asian food manufacturers supplying functional and processed foods to Western markets is further supporting market expansion.

| By Product Type | By Raw Material Source | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for nearly 32% of the global functional flours market in 2025, led primarily by the United States and Canada. Strong demand for gluten-free bakery products, sports nutrition foods, and clean-label packaged foods continues supporting regional growth. The United States alone represented approximately 24% of global market revenue due to high penetration of premium processed foods and strong innovation in plant-based product development. Consumers across the region increasingly prioritize organic, fortified, and protein-enriched food ingredients, encouraging food manufacturers to expand specialty flour portfolios.

Europe

Europe represented approximately 27% of global market demand in 2025, supported by strong bakery industries and strict food quality regulations. Germany remains the largest regional market due to extensive industrial bakery production and growing demand for fortified flour ingredients. The United Kingdom and France are experiencing rising adoption of gluten-free and vegan foods, while Italy continues witnessing strong demand from premium bakery and pasta applications. European food manufacturers are heavily investing in clean-label ingredient innovation and sustainable grain sourcing practices.

Asia-Pacific

Asia-Pacific is projected to register the fastest CAGR of over 9.5% during the forecast period. China dominates regional demand due to rapid urbanization, increasing processed food consumption, and expanding food fortification programs. India is emerging as a major high-growth market supported by rising middle-class incomes, increasing convenience food adoption, and government nutritional initiatives. Japan and South Korea are driving demand for functional ingredients in elderly nutrition, convenience foods, and premium bakery applications. Expanding food processing industries across Southeast Asia are also accelerating regional growth.

Latin America

Latin America is witnessing moderate but steadily growing demand for functional flours, led by Brazil and Mexico. Brazil’s expanding bakery and snack food sectors are increasing consumption of fortified and texture-enhancing flour ingredients. Mexico continues to experience rising demand for specialty corn-based functional flours used in tortillas, processed snacks, and convenience food applications. Regional food manufacturers are increasingly investing in local flour processing capacity to reduce import dependence and improve supply chain resilience.

Middle East & Africa

The Middle East & Africa market is gradually expanding due to rising food processing investments and increasing nutritional awareness. Saudi Arabia and the UAE are investing heavily in food security and local manufacturing initiatives, supporting regional demand for fortified flour ingredients. South Africa remains the leading African market due to its developed packaged food industry and growing health-conscious consumer base. Nigeria is projected to become one of the fastest-growing African markets as urbanization, population growth, and processed food demand continue increasing.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Functional Flours Market

- Archer Daniels Midland Company

- Cargill Incorporated

- Ingredion Incorporated

- Associated British Foods plc

- General Mills Inc.

- Bühler Group

- The Scoular Company

- SunOpta Inc.

- AGRANA Beteiligungs-AG

- Bunge Global SA

- Parrish and Heimbecker Limited

- Limagrain Ingredients

- The Hain Celestial Group Inc.

- Ardent Mills LLC

- Conagra Brands Inc.