Fruit Wine Market Size

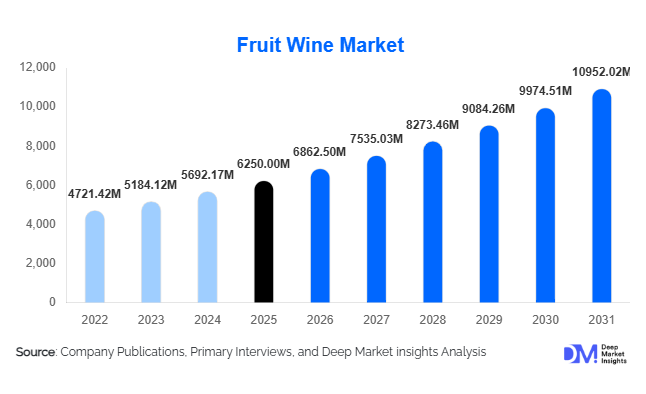

According to Deep Market Insights, the global fruit wine market size was valued at USD 6,250 million in 2025 and is projected to grow from USD 6,862.50 million in 2026 to reach USD 10,952.02 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The fruit wine market growth is primarily driven by rising consumer preference for flavored alcoholic beverages, increasing demand for low-alcohol and health-perceived drinks, and growing innovation in craft and artisanal wine production globally.

Key Market Insights

- Fruit wine is gaining traction as a healthier alternative to traditional grape wine, driven by its natural ingredients, antioxidant properties, and lower alcohol content.

- Premium and craft fruit wines are expanding rapidly, supported by artisanal production and unique regional fruit varieties.

- North America dominates the global market, backed by strong craft beverage culture and high consumer awareness.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable income, and changing alcohol consumption patterns.

- Online retail and direct-to-consumer channels are transforming distribution, enabling niche brands to reach global audiences.

- Innovative packaging formats, such as canned and ready-to-drink fruit wines, are attracting younger consumers.

What are the latest trends in the fruit wine market?

Rise of Functional and Health-Oriented Fruit Wines

Consumers are increasingly seeking beverages that offer health benefits alongside taste, driving demand for fruit wines enriched with antioxidants, vitamins, and natural ingredients. Berry-based wines, particularly those derived from blueberries and strawberries, are gaining popularity due to their perceived health advantages. Manufacturers are introducing organic, low-sugar, and preservative-free variants to cater to health-conscious consumers. This trend is also influencing premiumization, as consumers are willing to pay higher prices for clean-label and functional alcoholic beverages. Additionally, the integration of probiotic elements and botanical infusions is emerging as a niche but growing segment within the fruit wine category.

Growth of Craft and Localized Production

The craft beverage movement is significantly influencing the fruit wine market, with small-scale producers leveraging locally sourced fruits to create unique and region-specific offerings. This trend is particularly strong in North America and Europe, where consumers value authenticity and artisanal production methods. Local wineries are experimenting with exotic fruits such as mango, lychee, and passion fruit to differentiate their products. Government support for agro-processing and farm-based production is further encouraging localized manufacturing. This trend not only enhances product diversity but also supports rural economies and sustainable agricultural practices.

What are the key drivers in the fruit wine market?

Increasing Demand for Flavored Alcoholic Beverages

The shift in consumer preferences toward flavored and innovative alcoholic drinks is a major driver of the fruit wine market. Younger consumers, particularly millennials and Gen Z, are exploring alternatives to traditional wines, favoring beverages with unique taste profiles and lower bitterness. Fruit wines offer a wide variety of flavors, making them appealing for social occasions and casual consumption. This trend is further supported by marketing strategies that emphasize lifestyle, experimentation, and personalization.

Expansion of Hospitality and Tourism Sectors

The growing hospitality industry is boosting demand for fruit wines, as hotels, restaurants, and resorts increasingly include them in their beverage offerings. Fruit wines are often featured in curated menus, wine-tasting experiences, and local tourism promotions. Regions known for specific fruits are leveraging fruit wine production as part of their tourism strategy, enhancing regional branding and attracting visitors. This integration with tourism is creating new consumption channels and expanding market visibility.

What are the restraints for the global market?

Lack of Standardized Regulations

The absence of uniform regulations for fruit wine classification and labeling across countries poses challenges for global trade. Differences in alcohol laws, taxation, and quality standards create barriers for manufacturers seeking international expansion. Compliance with varying regulatory frameworks increases operational complexity and costs, limiting market scalability.

Storage and Shelf-Life Limitations

Fruit wines are often more sensitive to environmental conditions compared to traditional grape wines, leading to shorter shelf life and higher storage requirements. This affects distribution efficiency, particularly in regions with inadequate cold chain infrastructure. These limitations can increase logistics costs and impact product quality, posing a restraint to market growth.

What are the key opportunities in the fruit wine industry?

Expansion into Emerging Markets

Emerging economies in Asia-Pacific and Africa present significant growth opportunities for fruit wine producers. Rising middle-class populations, increasing urbanization, and changing social norms around alcohol consumption are driving demand in countries such as India, China, and Vietnam. Fruit wine, being perceived as lighter and more approachable, is well-positioned to attract new consumers. Strategic partnerships with local distributors and investment in regional production facilities can help companies capitalize on this growing demand.

Innovation in Packaging and Distribution

Advancements in packaging formats, including canned wines and single-serve options, are creating new growth avenues. These formats cater to convenience-driven consumers and are particularly popular among younger demographics. Additionally, the rise of e-commerce and direct-to-consumer sales channels is enabling brands to expand their reach and improve margins. Digital marketing and subscription-based models are further enhancing customer engagement and brand loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6250.00 Million |

| Market Size in 2026 | USD 6862.50 Million |

| Market Size in 2031 | USD 10952.02 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The fruit wine market exhibits a diverse product landscape, with still fruit wine continuing to dominate and accounting for approximately 46% of the total market share. This dominance can be attributed to its affordability, ease of production, and deep-rooted presence in traditional consumption patterns across multiple regions. Still fruit wines are widely preferred due to their balanced flavor profiles and accessibility to a broader consumer base, including both new and experienced wine drinkers. Their relatively lower production costs compared to sparkling or fortified variants also enable manufacturers to offer competitive pricing, further strengthening their position in mass-market segments.Sparkling fruit wines are gaining strong traction, particularly in premium and celebratory consumption segments. These wines are increasingly associated with social gatherings, weddings, and festive occasions, where consumers seek visually appealing and refreshing beverage options. The rising popularity of sparkling variants is also driven by younger consumers who are more open to experimentation and are influenced by lifestyle trends promoted through social media. Premiumization strategies adopted by producers, including attractive packaging and unique flavor combinations, are further boosting the adoption of sparkling fruit wines.Fortified and dessert fruit wines, although representing a smaller share of the market, cater to niche segments that prioritize richer flavors and higher alcohol content. These wines are particularly popular among consumers seeking indulgent and specialty beverages. Their use in culinary applications, such as pairing with desserts or enhancing recipes, is also contributing to their steady demand. Continuous advancements in fermentation technology and flavor enhancement are expanding the scope of these niche segments, enabling producers to tap into high-margin opportunities and diversify their product portfolios.

Application (End-Use) Insights

Household consumption remains the dominant application segment in the fruit wine market, contributing nearly 58% of the total demand. This segment’s leadership is primarily driven by the growing trend of at-home consumption, which has gained significant momentum in recent years. Consumers are increasingly opting to enjoy alcoholic beverages in the comfort of their homes, influenced by convenience, cost savings, and the availability of a wide range of products through retail and online channels. The rise of home-based social gatherings and casual consumption occasions has further strengthened this segment.The leading driver for household consumption is the increasing preference for convenient and ready-to-drink beverages that align with modern lifestyles. Fruit wines, with their approachable taste profiles and versatility, are well-suited for both casual drinking and pairing with meals. Additionally, the growing awareness of fruit-based beverages as a relatively healthier alternative compared to synthetic or high-calorie alcoholic drinks is encouraging more consumers to incorporate fruit wines into their regular consumption habits. Packaging innovations such as smaller bottles and single-serve formats are also enhancing convenience, further driving household demand.Industrial applications, although relatively niche, are gaining attention as fruit wines are increasingly used in culinary preparations, food processing, and gourmet product development. Their unique flavor profiles make them suitable for use in sauces, marinades, and desserts, adding depth and complexity to various dishes. Additionally, the rising demand for artisanal and specialty food products is creating new opportunities for fruit wine integration in the food industry. Export-driven demand is also contributing to overall market growth, particularly for specialty and premium fruit wines in developed markets such as Japan and Germany, where consumers are willing to pay a premium for unique and high-quality products.

Distribution Channel Insights

Off-trade channels dominate the fruit wine market, accounting for approximately 65% of total sales. This segment includes supermarkets, hypermarkets, specialty liquor stores, and online retail platforms, all of which play a crucial role in ensuring product accessibility and visibility. The widespread presence of organized retail chains and the increasing penetration of e-commerce platforms are key factors driving the dominance of off-trade channels.On-trade channels, including restaurants, bars, and hotels, continue to play a significant role in shaping consumer perceptions and promoting premium products. These channels provide an opportunity for consumers to experience fruit wines in curated settings, often accompanied by expert recommendations and food pairings. The role of on-trade channels in brand building and premium positioning cannot be overstated, as they help create awareness and drive trial among new consumers.Direct-to-consumer (DTC) sales are gaining momentum as wineries increasingly leverage digital platforms to connect with their customers. By offering exclusive products, personalized experiences, and subscription-based models, producers are able to build stronger relationships with their target audience. This approach not only enhances customer loyalty but also provides valuable insights into consumer preferences, enabling companies to tailor their offerings and marketing strategies more effectively.

Packaging Insights

Glass bottles continue to dominate the fruit wine packaging segment, accounting for over 60% of the market share. Their dominance is largely driven by their premium appeal, durability, and ability to preserve the quality and flavor of the wine over extended periods. Glass packaging is often associated with authenticity and tradition, making it the preferred choice for both producers and consumers, particularly in the premium segment.However, alternative packaging formats such as cans and bag-in-box solutions are rapidly gaining popularity, especially among younger consumers and those seeking convenience and portability. Canned fruit wines are emerging as a trendy option for outdoor activities, casual gatherings, and on-the-go consumption. Their lightweight nature, ease of use, and recyclability make them an attractive alternative to traditional packaging.Sustainability is becoming an increasingly important consideration in packaging decisions, with both consumers and regulators placing greater emphasis on environmentally friendly solutions. As a result, manufacturers are exploring innovative materials and designs that reduce environmental impact while maintaining product quality. The adoption of recyclable and biodegradable packaging materials, along with efforts to reduce carbon footprints, is expected to shape the future of the fruit wine packaging segment.

Explore more data points, trends and opportunities Download Free Sample Report

Fruit Wine Market Segmentations

By Fruit Type

- Apple Wine

- Berry Wine

- Tropical Fruit Wine

- Stone Fruit Wine

- Citrus Fruit Wine

- Other Fruit Wines

By Product Type

- Still Fruit Wine

- Sparkling Fruit Wine

- Fortified Fruit Wine

- Dessert Fruit Wine

By Distribution Channel

- On-Trade

- Off-Trade

- Online Retail

Regional Insights

North America

North America holds approximately 32% of the global fruit wine market share, making it one of the leading regions in terms of consumption and innovation. The United States plays a pivotal role in driving regional demand, supported by a well-established craft beverage culture and a high level of consumer awareness. The region’s dynamic market environment encourages experimentation and product innovation, enabling producers to introduce new flavors and formats that cater to evolving consumer preferences.Canada is also witnessing steady growth, driven by increasing local production and a growing appreciation for specialty wines. The region benefits from advanced distribution networks, strong retail infrastructure, and a supportive regulatory environment, all of which contribute to market development. The increasing adoption of e-commerce and direct-to-consumer sales channels is further enhancing accessibility and driving growth across the region.

Europe

Europe accounts for around 29% of the global fruit wine market, with countries such as Germany, the United Kingdom, and Poland serving as key contributors. The region’s rich wine heritage and established consumption culture create a favorable environment for the adoption of fruit wines. European consumers are generally more open to experimenting with new flavors and beverage categories, which supports the growth of this market segment.Additionally, the region’s well-developed tourism industry plays a significant role in promoting fruit wines, as visitors are often introduced to local specialties and artisanal products. The presence of established distribution channels and a strong retail network further supports market growth, enabling producers to reach a wide audience across multiple countries.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for fruit wine, with a compound annual growth rate exceeding 12%. This rapid growth is driven by a combination of rising disposable incomes, urbanization, and changing consumption patterns. Countries such as China and India are emerging as major growth markets, supported by their large population bases and increasing exposure to global beverage trends.Japan represents a more mature market within the region, characterized by steady demand for premium and high-quality fruit wines. The country’s emphasis on craftsmanship and quality aligns well with the artisanal nature of many fruit wine products. Additionally, the increasing influence of Western culture and dining habits is contributing to the adoption of fruit wines across the region.

Latin America

Latin America is experiencing moderate growth in the fruit wine market, with countries such as Brazil and Chile leading the way. The region’s abundant fruit production provides a strong foundation for local wine manufacturing, enabling producers to create a diverse range of products using locally sourced ingredients.Additionally, the region’s growing middle class and improving economic conditions are contributing to increased spending on premium and specialty beverages. This trend is encouraging producers to invest in product development and branding, thereby strengthening their presence in the market.

Middle East & Africa

The Middle East & Africa region is gradually expanding in the fruit wine market, with South Africa serving as a key contributor due to its well-established wine industry. The country’s favorable climate and strong agricultural base support the production of high-quality fruit wines, enabling it to compete in both domestic and international markets.However, regulatory constraints and cultural factors in certain countries may limit market penetration. Despite these challenges, the region presents significant growth opportunities, particularly as urbanization and economic development continue to progress. Increasing investments in retail infrastructure and the gradual relaxation of regulations in some areas are expected to support future market expansion.

Key Players in the Fruit Wine Market

- Arbor Mist Winery

- Linganore Winecellars

- Island Grove Wine Company

- Wild Berry Wines

- St. Julian Winery

- Oliver Winery

- Chaucers Wine Company

- Tropical Winery

- San Sebastian Winery

- Door Peninsula Winery

- Nashoba Valley Winery

- Cedar Creek Winery

- Four Seasons Wines

- Hillcrest Vineyard

- Château Joliet