Fruit Jam, Jelly and Preserves Market Size

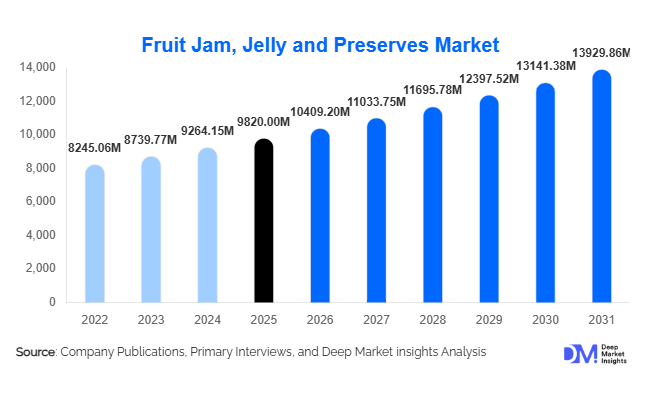

According to Deep Market Insights, the global fruit jam, jelly and preserves market size was valued at USD 9,820 million in 2025 and is projected to grow from USD 10,409.20 million in 2026 to reach USD 13,929.86 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). Market expansion is primarily supported by rising consumption of convenient breakfast foods, increasing demand for fruit-based spreads with natural ingredients, and growing penetration of premium and organic preserves across developed and emerging economies. The industry is undergoing gradual transformation as consumers shift toward clean-label, reduced-sugar, and functional fruit spreads, encouraging manufacturers to innovate across flavors, formulations, and packaging formats.

Key Market Insights

- Premium and artisanal fruit preserves are gaining momentum as consumers increasingly prefer natural and minimally processed food products.

- Low-sugar and no-added-sugar variants are expanding rapidly, driven by global health awareness and diabetes management concerns.

- Europe dominates global consumption due to strong breakfast culture and established fruit-processing industries.

- Asia-Pacific is the fastest-growing regional market, supported by urbanization and Westernized eating habits.

- Private-label brands are strengthening retail competition, particularly across supermarkets and hypermarkets.

- Packaging innovation, including squeeze bottles and single-serve formats, is improving convenience and reducing food waste.

What are the latest trends in the fruit jam, jelly and preserves market?

Shift Toward Clean-Label and Natural Ingredients

Consumers globally are moving away from artificial additives and high-fructose sweeteners toward natural fruit spreads containing recognizable ingredients. Manufacturers are reformulating products using real fruit pulp, natural pectin, and alternative sweeteners such as stevia and fruit concentrates. Organic certifications and transparent labeling are becoming strong purchase drivers, particularly in North America and Europe. Premiumization is evident as brands highlight origin-specific fruits such as Mediterranean figs, Alpine berries, and tropical mango varieties. This trend is pushing producers toward shorter ingredient lists while maintaining taste and shelf stability through improved processing technologies.

Flavor Innovation and Exotic Fruit Expansion

Traditional flavors such as strawberry and mixed fruit continue to dominate, but demand for exotic and regional fruit variants is accelerating. Consumers are increasingly experimenting with flavors such as blueberry-lavender, pineapple-chili, dragon fruit, and passionfruit blends. Emerging economies are contributing significantly through local fruit diversification, enabling manufacturers to localize product portfolios. Limited-edition seasonal launches and gourmet pairings with cheese and bakery products are expanding consumption occasions beyond breakfast, positioning fruit preserves as versatile culinary ingredients.

What are the key drivers in the fruit jam, jelly and preserves market?

Rising Demand for Convenient Breakfast Solutions

Urban lifestyles and dual-income households are driving demand for ready-to-consume breakfast products. Fruit spreads remain a staple accompaniment to bread, pancakes, waffles, and bakery items, supporting consistent consumption across households and foodservice channels. Growth in packaged bakery products directly stimulates demand for jams and preserves as complementary products.

Expansion of Health-Oriented Product Lines

Manufacturers are increasingly introducing reduced-sugar, fortified, and functional variants enriched with vitamins, antioxidants, and superfruits. Consumers seeking healthier indulgence options are supporting premium pricing strategies. The rise of flexitarian and plant-based diets further enhances demand for fruit-based spreads as alternatives to dairy-based toppings.

E-commerce and Modern Retail Penetration

Online grocery platforms and organized retail chains have significantly expanded product visibility. Digital channels allow niche and artisanal brands to reach global audiences, accelerating innovation and competition. Subscription-based grocery deliveries and direct-to-consumer models are reshaping purchasing patterns.

What are the restraints for the global market?

Volatility in Fruit Raw Material Prices

Seasonal fluctuations, climate variability, and agricultural supply disruptions significantly affect fruit availability and pricing. Rising costs of berries and tropical fruits directly impact manufacturer margins, forcing periodic price adjustments.

Health Concerns Around Sugar Content

Despite innovation, traditional jam products remain associated with high sugar content. Increasing regulatory scrutiny and consumer preference for low-calorie diets may limit growth of conventional products unless reformulation efforts continue.

What are the key opportunities in the fruit jam, jelly and preserves industry?

Premium and Organic Product Expansion

The premium food segment presents strong growth opportunities as consumers increasingly value authenticity and quality sourcing. Organic fruit preserves and small-batch artisanal offerings command higher margins and attract health-conscious urban consumers. Expansion into specialty retail and gourmet food channels provides new revenue streams for manufacturers.

Emerging Market Consumption Growth

Rapid urbanization across Asia-Pacific, Latin America, and parts of Africa is introducing Western-style breakfast consumption patterns. Increasing disposable incomes and retail modernization enable higher penetration of packaged spreads. Local fruit sourcing also reduces costs and encourages regional product innovation tailored to cultural taste preferences.

Functional and Nutritional Innovations

Integration of functional ingredients such as chia seeds, probiotics, and antioxidant-rich berries is creating differentiation opportunities. Brands positioning fruit spreads as wellness-oriented foods are capturing younger demographics and fitness-focused consumers. This innovation is expanding usage occasions beyond traditional breakfast applications into snacks and desserts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9820 Million |

| Market Size in 2026 | USD 10409.20 Million |

| Market Size in 2031 | USD 13929.86 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global fruit jam market demonstrates strong product diversification, with fruit jams continuing to dominate overall consumption patterns and accounting for nearly 46% of the global market share in 2025. The leadership of this segment is primarily driven by its universal household acceptance, affordability, and compatibility with a wide range of bakery and breakfast products such as bread, pancakes, pastries, and desserts. Increasing demand for convenient breakfast solutions and ready-to-spread products further strengthens the leading position of fruit jams. In addition, continuous flavor innovation, fortified variants, and reduced-sugar formulations are expanding consumer appeal across both developed and emerging markets. Jellies represent approximately 28% of the market, supported particularly by strong consumer preference in North America where smooth texture, longer shelf stability, and ease of spreading align with mass retail consumption habits. Meanwhile, preserves and marmalades collectively account for nearly 26% share and are witnessing steady expansion within premium and artisanal categories. Their higher fruit content, perceived authenticity, and clean-label positioning are attracting health-conscious consumers willing to pay premium prices. Market trends increasingly indicate gradual consumer migration toward preserves as shoppers prioritize natural ingredients, higher fruit inclusion, and minimally processed food products.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels, contributing nearly 52% of global sales, primarily due to strong product visibility, diversified brand portfolios, and expanding private-label offerings that enhance price competitiveness. Large retail chains also enable bulk purchasing behavior and promotional pricing strategies, supporting high-volume sales. The leading growth driver within distribution is the rapid expansion of organized retail ecosystems and integrated supply chains that ensure consistent product availability. Online retail is emerging as the fastest-growing channel, expanding at more than 8% annually as digital grocery adoption accelerates worldwide. Increasing smartphone penetration, improved last-mile delivery infrastructure, and subscription-based grocery services are reshaping purchasing behavior, particularly among urban consumers. Convenience stores maintain stable demand in densely populated cities where impulse buying and smaller pack sizes drive turnover. At the same time, specialty gourmet stores are gaining strategic importance as premium fruit preserves and organic spreads expand, enabling brands to position differentiated, high-margin products targeting affluent consumers.

Application Insights

Household consumption continues to represent the dominant application segment, accounting for approximately 63% of total global demand, supported by consistent breakfast consumption habits and the growing preference for quick meal solutions. The leading driver for this segment is the increasing demand for convenient, ready-to-use spreads that require minimal preparation time while offering flavor variety. Rising dual-income households and busy urban lifestyles are reinforcing at-home consumption of packaged breakfast products. The foodservice sector is experiencing accelerated growth as cafés, bakeries, and quick-service restaurants increasingly incorporate fruit spreads into sandwiches, desserts, waffles, and breakfast platters to enhance menu differentiation. Industrial applications are also expanding steadily, supported by growth in commercial bakery and confectionery manufacturing where fruit fillings and toppings are widely used in packaged snacks, cookies, and pastries. Expansion of global packaged food production and private-label bakery manufacturing continues to strengthen industrial demand.

End-Use Industry Insights

The bakery industry remains the largest end-use sector, contributing nearly 40% of total demand, with its leadership primarily driven by sustained global consumption of bread, cakes, and pastries. Rising urban populations and increasing consumption of packaged baked goods are directly boosting utilization of fruit spreads as fillings, toppings, and flavor enhancers. The global packaged bakery industry is expanding at over 5% annually, creating stable downstream demand for jam manufacturers. Foodservice establishments, including hotels, cafés, and restaurant chains, represent one of the fastest-growing end-use industries as breakfast menu diversification and premium dessert offerings expand worldwide. Additionally, export-oriented demand is gaining momentum as European and Asian producers ship premium preserves to North America and the Middle East, where imported gourmet food products command higher margins and cater to premium retail segments. Increasing tourism activity and hospitality sector expansion further support long-term demand growth.

Explore more data points, trends and opportunities Download Free Sample Report

Fruit Jam, Jelly and Preserves Market Segmentations

By Product Type

- Fruit Jams

- Fruit Jellies

- Fruit Preserves & Marmalades

By Application

- Household Consumption

- Bakery Industry

- Foodservice

- Industrial

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail / E-commerce

- Convenience Stores

- Specialty & Gourmet Stores

Regional Insights

Europe

Europe holds the largest regional share at approximately 34% of the global market in 2025, led by Germany, France, the United Kingdom, and Italy. The region benefits from deeply rooted breakfast consumption traditions and strong cultural preference for fruit-based spreads. Regional growth is supported by high fruit production capacity, advanced food processing infrastructure, and well-established artisanal preserve manufacturing industries. Increasing consumer demand for organic, clean-label, and locally sourced products is accelerating premium segment expansion across Western Europe. Sustainability initiatives, strict food quality standards, and innovation in reduced-sugar formulations are further driving product upgrades and market maturity.

North America

North America accounts for nearly 27% market share, with the United States representing the largest contributor due to long-standing peanut butter and jelly consumption culture that ensures stable baseline demand. Regional growth is driven by product innovation in low-sugar, functional, and fortified spreads aligned with health-conscious consumer trends. Canada is witnessing increasing adoption of organic and natural fruit spreads supported by clean-label preferences. Packaging innovation, including squeeze bottles, resealable pouches, and single-serve formats, enhances convenience and supports retail expansion. Strong private-label penetration and advanced retail distribution networks further reinforce market stability.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 7% CAGR, supported by rapid urbanization, rising disposable incomes, and evolving dietary habits. China, India, Japan, and Australia are major contributors to regional expansion. Growth is primarily driven by increasing adoption of Western-style breakfast patterns, expansion of modern retail chains, and growing demand for convenient packaged foods among younger consumers. Localization of flavors plays a crucial role in regional growth, with mango, pineapple, strawberry, and mixed-fruit variants gaining popularity across India and Southeast Asia. Government initiatives promoting food processing industries and improvements in cold-chain logistics are also enabling domestic production capacity expansion.

Middle East & Africa

The Middle East demonstrates steady growth driven by rising demand for imported premium spreads, particularly in the UAE and Saudi Arabia, where high disposable incomes and expanding expatriate populations influence Western consumption patterns. Growth in organized retail and hospitality sectors further supports demand across hotels and foodservice establishments. In Africa, gradual market expansion is supported by improving retail infrastructure, urban population growth, and increasing investment in local fruit processing industries. Countries such as South Africa and Kenya are strengthening domestic production capabilities through agro-processing initiatives aimed at reducing food imports and increasing value-added agricultural output.

Latin America

Latin America continues to show stable growth led by Brazil, Mexico, and Argentina, supported by abundant fruit availability and expanding processed food consumption. Regional growth drivers include rising investment in fruit processing facilities, increasing export competitiveness, and strong agricultural supply chains that enable cost-effective production. Local manufacturers are expanding berry-based and tropical fruit preserve exports to global markets, benefiting from favorable climatic conditions and growing international demand for natural fruit products. Expansion of modern retail formats and increasing middle-class consumption are further strengthening domestic demand.

Key Players in the Fruit Jam, Jelly and Preserves Market

- The J.M. Smucker Company

- Hero Group

- Andros Group

- Bonne Maman

- Kraft Heinz Company

- Ferrero Group

- Wilkin & Sons Ltd.

- Darbo AG

- Orkla ASA

- B&G Foods Inc.

- Premier Foods plc

- Conagra Brands Inc.

- St. Dalfour SAS

- F. Duerr & Sons Ltd.

- Rigoni di Asiago Srl