Frozen Yoghurt Market Size

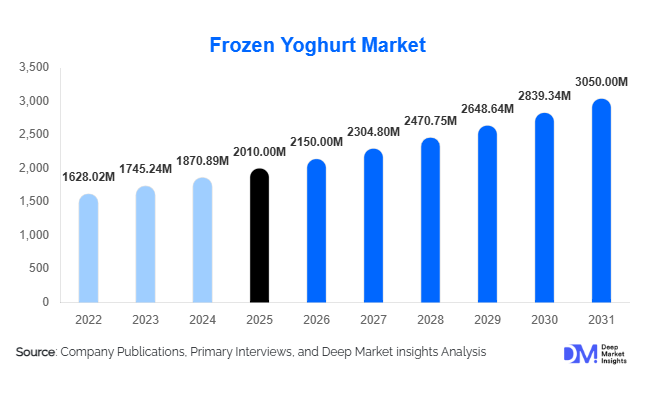

According to Deep Market Insights, the global frozen yoghurt market size was valued at USD 2,010 million in 2025 and is projected to grow from USD 2,150 million in 2026 to reach USD 3,050 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The frozen yoghurt market growth is primarily driven by increasing consumer demand for healthier dessert alternatives, rising awareness of probiotic benefits, and continuous innovation in flavors and plant-based offerings.

Key Market Insights

- Frozen yoghurt is increasingly positioned as a “better-for-you dessert,” gaining traction among health-conscious consumers seeking low-fat and probiotic-rich indulgence.

- Plant-based frozen yoghurt is witnessing rapid growth, driven by rising veganism and lactose intolerance awareness globally.

- North America dominates the global market due to strong presence of frozen yoghurt chains and high consumer awareness.

- Asia-Pacific is the fastest-growing region, supported by urbanization, rising disposable incomes, and western dietary influence.

- Foodservice channels lead consumption, particularly through QSRs and dessert chains offering soft-serve formats.

- Flavor innovation and premiumization trends are driving repeat purchases and higher margins across developed markets.

What are the latest trends in the frozen yoghurt market?

Rise of Plant-Based and Functional Frozen Yoghurt

The frozen yoghurt market is undergoing a significant transformation with the emergence of plant-based and functional products. Consumers are increasingly seeking dairy-free alternatives made from almond, coconut, soy, and oat milk, particularly in North America and Europe. These products not only cater to vegan consumers but also appeal to individuals with lactose intolerance and dietary restrictions. Additionally, manufacturers are incorporating functional ingredients such as probiotics, vitamins, and low-sugar formulations to enhance nutritional value. This trend is positioning frozen yoghurt as both a dessert and a functional snack, expanding its appeal beyond traditional consumption occasions.

Premiumization and Experiential Retail Expansion

Premium frozen yoghurt offerings are gaining momentum as consumers show willingness to pay higher prices for artisanal quality, unique flavors, and customized experiences. Self-serve outlets, gourmet toppings, and interactive retail formats are becoming key differentiators. Brands are also leveraging digital technologies such as mobile ordering, loyalty programs, and AI-driven personalization to enhance customer engagement. This experiential approach is particularly appealing to millennials and urban consumers, driving higher footfall and repeat visits in foodservice channels.

What are the key drivers in the frozen yoghurt market?

Growing Health Consciousness

One of the primary drivers of the frozen yoghurt market is the increasing shift toward healthier eating habits. Consumers are actively reducing their intake of high-fat and high-calorie desserts, opting instead for alternatives that offer nutritional benefits. Frozen yoghurt, with its lower fat content and probiotic properties, aligns well with these preferences. This trend is particularly strong among millennials and urban populations, who prioritize wellness and balanced diets.

Expansion of Organized Retail and Foodservice Chains

The rapid expansion of supermarkets, hypermarkets, and branded dessert chains has significantly improved product accessibility. Frozen yoghurt chains and QSRs are expanding their footprint globally, particularly in emerging markets. These outlets promote impulse buying and provide consumers with a wide variety of flavors and formats, contributing to increased consumption. Franchise-based models are further accelerating market penetration.

What are the restraints for the global market?

High Competition from Traditional Desserts

Frozen yoghurt faces intense competition from established dessert categories such as ice cream and gelato. These alternatives often benefit from stronger brand loyalty, wider flavor portfolios, and deeper market penetration. As a result, frozen yoghurt brands must continuously innovate to maintain consumer interest and market share.

Dependence on Cold Chain Infrastructure

The frozen yoghurt market is highly dependent on efficient cold chain logistics for storage and transportation. In developing regions, inadequate infrastructure can lead to increased operational costs and limited product availability. This poses a significant challenge for market expansion, particularly in rural and semi-urban areas.

What are the key opportunities in the frozen yoghurt industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and the Middle East present significant growth opportunities. Rising disposable incomes, urbanization, and increasing exposure to western food trends are driving demand for frozen yoghurt. Localization of flavors and pricing strategies can further enhance market penetration in these regions.

Innovation in Product Formats and Flavors

Continuous innovation in flavors and formats, including frozen yoghurt bars, bites, and seasonal offerings, provides opportunities for differentiation. Limited-edition flavors and region-specific variants can attract new customers and encourage repeat purchases. Brands investing in R&D are likely to gain a competitive edge.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2010 Million |

| Market Size in 2026 | USD 2150 Million |

| Market Size in 2031 | USD 3050 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen yoghurt market is characterized by a diverse range of product types catering to varying consumer preferences, dietary requirements, and price sensitivities. Among these, regular frozen yoghurt continues to dominate the market, accounting for approximately 38% of the global share in 2025. This dominance is primarily attributed to its affordability, widespread availability, and strong consumer familiarity. Regular frozen yoghurt is extensively distributed across both retail and foodservice channels, making it easily accessible to a broad demographic. Its balanced flavor profile, which combines sweetness with mild tartness, appeals to a wide audience, including children, young adults, and families. Additionally, manufacturers continue to innovate within this segment by introducing new flavors, toppings, and packaging formats, further strengthening its market position. The leading driver for this segment remains its cost-effectiveness combined with mass-market appeal, enabling it to maintain a strong foothold even as premium alternatives emerge.Greek frozen yoghurt represents another important segment, gaining traction due to its higher protein content and premium positioning. This segment appeals strongly to health-conscious consumers and fitness enthusiasts who seek indulgent yet nutritious dessert options. Greek frozen yoghurt is often marketed as a guilt-free treat, offering a creamy texture and rich taste while delivering added functional benefits such as protein enrichment and probiotics. The leading driver here is the increasing consumer inclination toward high-protein diets and functional foods that support active lifestyles. As a result, this segment is witnessing strong adoption in both developed and emerging markets, particularly in urban areas where health and wellness trends are more pronounced.

Application Insights

In terms of application, the frozen yoghurt market is segmented into foodservice and retail consumption, with foodservice applications leading the market by contributing approximately 52% of total demand in 2025. This dominance is primarily driven by the extensive presence of quick-service restaurants (QSRs), dessert chains, and cafés that offer frozen yoghurt as a customizable and experiential product. The leading driver for this segment is the strong consumer preference for out-of-home dessert experiences, where customization, variety, and instant gratification play a crucial role. Soft-serve formats, self-service kiosks, and a wide range of toppings allow consumers to personalize their desserts, enhancing engagement and satisfaction.Household consumption is also gaining traction as consumers adopt more home-centric lifestyles and explore new dessert options within the comfort of their homes. The expansion of e-commerce and rapid delivery services has made it easier for consumers to access a wide range of frozen yoghurt products without visiting physical stores. As a result, the application landscape is becoming more diversified, with both foodservice and retail channels playing complementary roles in driving overall market growth.

Distribution Channel Insights

The distribution landscape of the frozen yoghurt market is evolving in response to changing consumer shopping behaviors and technological advancements. Supermarkets and hypermarkets currently dominate the retail distribution segment, accounting for a significant share of overall sales. The leading driver for this channel is its extensive reach and ability to offer a wide variety of products under one roof. Consumers prefer these outlets for their convenience, competitive pricing, and the opportunity to compare different brands and product types in a single visit.Specialty stores and convenience outlets also play a significant role, particularly in urban and semi-urban areas. These outlets cater to niche markets by offering premium, artisanal, and health-focused frozen yoghurt products. The leading driver for this segment is the growing demand for unique and high-quality offerings that are not typically available in mass-market channels. Convenience stores, in particular, benefit from their strategic locations and extended operating hours, making them an ideal choice for impulse purchases and on-the-go consumption.Overall, the distribution channel landscape is becoming increasingly dynamic, with traditional and digital channels coexisting and complementing each other to meet diverse consumer needs.

End-Use Insights

The frozen yoghurt market is segmented by end-use into commercial and household applications, with the commercial segment leading the market and accounting for approximately 55% of total demand in 2025. This dominance is primarily driven by the strong presence of dessert chains, QSRs, and foodservice outlets that rely on frozen yoghurt as a key menu item. The leading driver for this segment is the high demand for experiential and customizable dessert options in commercial settings. Businesses in this segment benefit from higher foot traffic, repeat customers, and the ability to introduce innovative offerings that cater to evolving consumer preferences.The household segment, while smaller in comparison, is experiencing steady growth. The leading driver for this segment is the increasing consumer preference for at-home consumption, particularly in the wake of changing lifestyles and greater emphasis on convenience. Packaged frozen yoghurt products are becoming more accessible through retail and online channels, enabling consumers to enjoy their favorite desserts without leaving their homes. Innovations in packaging and portion sizes are also catering to different household needs, from single servings to family packs.Emerging applications in fitness nutrition and functional foods are further expanding the end-use potential of frozen yoghurt. Products enriched with probiotics, vitamins, and protein are gaining popularity among health-conscious consumers, creating new opportunities for manufacturers to differentiate their offerings and capture additional market share.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Yoghurt Market Segmentations

By Product Type

- Regular Frozen Yoghurt

- Low-Fat Frozen Yoghurt

- Non-Fat Frozen Yoghurt

- Greek Frozen Yoghurt

- Lactose-Free Frozen Yoghurt

- Plant-Based Frozen Yoghurt

By Flavor

- Plain/Natural

- Fruit-Based Flavors

- Chocolate-Based Flavors

- Vanilla

- Exotic/Innovative Flavors

By Distribution Channel

- Foodservice

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

Regional Insights

North America

North America holds the largest share of the global frozen yoghurt market, accounting for approximately 35% in 2025. The United States is the primary contributor, supported by a well-established foodservice industry, high consumer awareness, and a strong culture of dessert consumption. One of the key growth drivers in this region is the increasing demand for low-calorie and healthier dessert alternatives, which has positioned frozen yoghurt as a preferred choice over traditional ice cream. The presence of numerous frozen yoghurt chains and franchises further strengthens market penetration and accessibility.Another significant driver is the region’s advanced retail infrastructure, which ensures widespread availability of both premium and mass-market products. In addition, continuous product innovation, including the introduction of plant-based and functional variants, is attracting a diverse consumer base. Canada also contributes to regional growth, driven by rising health consciousness and increasing adoption of premium and dairy-free products. The combination of strong consumer demand, technological advancements, and robust distribution networks makes North America a mature yet highly dynamic market.

Europe

Europe accounts for approximately 25% of the global frozen yoghurt market, with key countries including the United Kingdom, Germany, and France leading the way. The region is characterized by a strong preference for organic, low-fat, and clean-label products, which aligns well with the positioning of frozen yoghurt as a healthier dessert option. One of the primary growth drivers in Europe is the increasing regulatory support for sustainable and transparent food production practices. This has encouraged manufacturers to adopt eco-friendly packaging and natural ingredients, thereby enhancing consumer trust and brand loyalty.Another important driver is the growing popularity of plant-based diets, which has led to increased demand for dairy-free frozen yoghurt products. The region’s well-developed retail and foodservice sectors also contribute to market growth by providing diverse consumption channels. Additionally, cultural preferences for artisanal and premium products are driving innovation and differentiation within the market. As a result, Europe continues to be a significant contributor to global market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the frozen yoghurt market, with a projected CAGR of approximately 9% during the forecast period. Key markets such as China and India are driving this growth, supported by rapid urbanization, rising disposable incomes, and changing dietary habits. One of the leading growth drivers in this region is the increasing adoption of Western food trends, particularly among younger consumers who are more open to experimenting with new flavors and formats.Another critical driver is the expansion of modern retail infrastructure and e-commerce platforms, which has improved product accessibility across urban and semi-urban areas. In addition, the growing middle-class population and increasing health awareness are boosting demand for healthier dessert alternatives. Japan, as a mature market, continues to drive innovation through premium and unique flavor offerings, catering to sophisticated consumer preferences. Overall, the Asia-Pacific region presents significant growth opportunities for both domestic and international players.

Latin America

Latin America is experiencing moderate growth in the frozen yoghurt market, with Brazil and Mexico emerging as key contributors. One of the primary growth drivers in this region is the increasing penetration of organized retail, which has enhanced product availability and visibility. The region’s young and dynamic population is also contributing to rising demand for trendy and customizable dessert options.Another important driver is the growing influence of global food trends, which is encouraging consumers to explore new and innovative products. Urbanization and rising disposable incomes are further supporting market growth by enabling consumers to spend more on premium and imported products. While challenges such as economic volatility and limited cold chain infrastructure persist, ongoing investments in logistics and distribution are expected to improve market conditions over time.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth in the frozen yoghurt market, driven by high disposable incomes and a strong preference for premium dessert products in countries such as the UAE and Saudi Arabia. One of the key growth drivers in this region is the expanding hospitality and tourism industry, which has led to increased demand for high-quality dessert offerings in hotels, restaurants, and cafés.Another significant driver is the growing expatriate population, which brings diverse culinary preferences and contributes to the popularity of international food trends. While imported frozen yoghurt products currently dominate the market, local production is gradually increasing as manufacturers recognize the region’s growth potential. Improvements in cold chain infrastructure and distribution networks are also supporting market expansion by ensuring product quality and availability. As a result, the Middle East & Africa region is emerging as a promising market with considerable untapped opportunities.

Key Players in the Frozen Yoghurt Market

- Nestlé

- Danone

- Unilever

- General Mills

- Yogen Früz

- Menchie’s Frozen Yogurt

- Pinkberry

- Red Mango

- TCBY

- Yogurtland

- Orange Leaf

- 16 Handles

- Sweet Frog

- Stonyfield Farm

- Noosa Yoghurt