Frozen Vegetables Market Size

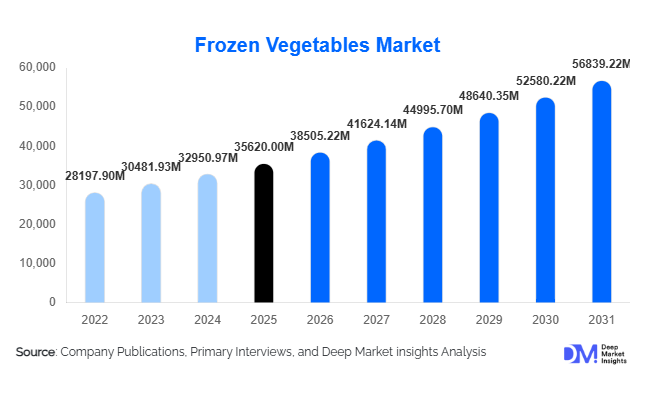

According to Deep Market Insights, the global frozen vegetables market size was valued at USD 35,620 million in 2025 and is projected to grow from USD 38,505.22 million in 2026 to reach USD 56,839.22 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The frozen vegetables market growth is primarily driven by rising consumer demand for convenient and nutritious food solutions, expansion of cold-chain infrastructure, and increasing adoption of frozen ingredients across foodservice and processed food industries. Improvements in Individually Quick Frozen (IQF) technology have enhanced product quality, enabling frozen vegetables to retain texture, flavor, and nutritional value comparable to fresh produce.

Key Market Insights

- Convenience-led consumption patterns are accelerating frozen vegetable adoption, particularly among urban households and dual-income families.

- Foodservice operators are increasing reliance on frozen vegetables due to standardized quality, reduced waste, and operational efficiency.

- Europe dominates the global market, supported by mature cold-chain logistics and high consumer acceptance of frozen foods.

- Asia-Pacific is the fastest-growing region, driven by retail modernization and government investments in food processing infrastructure.

- IQF technology accounts for the majority of production, enabling portion control and improved shelf stability.

- Sustainability benefits, including reduced food waste and longer shelf life, are strengthening consumer perception of frozen vegetables globally.

What are the latest trends in the frozen vegetables market?

Premium and Organic Frozen Vegetable Expansion

Consumer preferences are shifting toward organic, clean-label, and sustainably sourced food products, leading to rapid expansion of premium frozen vegetable categories. Retailers are increasingly allocating freezer shelf space to pesticide-free and traceable vegetable offerings. Organic frozen vegetables command higher margins compared to conventional variants and appeal strongly to health-conscious consumers in North America and Europe. Brands are introducing nutrient-focused vegetable blends, antioxidant-rich mixes, and ready-to-cook gourmet combinations designed for modern cooking habits. Sustainability certifications and eco-friendly packaging formats are also becoming major differentiators among leading manufacturers.

Technology-Driven Freezing and Supply Chain Optimization

Technological innovation is reshaping frozen vegetable production and distribution. Individually Quick Frozen (IQF) processing enables vegetables to be frozen immediately after harvest, preserving nutritional integrity while allowing flexible portion usage. Automation, AI-driven sorting, and digital supply-chain tracking systems are improving efficiency and reducing operational costs. Smart cold-chain monitoring technologies now allow real-time temperature tracking during transportation, ensuring food safety compliance and minimizing spoilage losses. These advancements are enabling manufacturers to expand export capabilities and maintain consistent quality across global markets.

What are the key drivers in the frozen vegetables market?

Growing Demand for Convenient Meal Solutions

Changing lifestyles and increasing workforce participation have driven demand for ready-to-cook ingredients that reduce meal preparation time. Frozen vegetables eliminate washing, peeling, and cutting processes while offering year-round availability. This convenience factor has significantly boosted household consumption, particularly in urban regions where time efficiency is a major purchasing driver. Expansion of modern retail formats and online grocery platforms further supports accessibility and product visibility.

Expansion of Foodservice and Processed Food Industries

The rapid growth of quick-service restaurants, cloud kitchens, and ready-meal manufacturers has increased demand for standardized vegetable inputs. Frozen vegetables provide consistency in taste, texture, and supply regardless of seasonal agricultural fluctuations. Restaurants benefit from reduced labor costs and predictable pricing, while food manufacturers rely on frozen vegetables for soups, frozen meals, and plant-based food formulations. The global expansion of foodservice chains across Asia and the Middle East continues to strengthen demand.

What are the restraints for the global market?

High Cold Chain Infrastructure Costs

The frozen vegetables industry depends heavily on temperature-controlled logistics, which require significant investments in refrigerated storage, transportation, and energy consumption. In developing economies, unreliable power supply and infrastructure gaps increase operational expenses, limiting penetration into rural markets. These cost challenges can affect pricing competitiveness compared to fresh produce.

Preference for Fresh Produce in Traditional Markets

Consumer perception remains a barrier in several emerging economies where fresh vegetables are culturally preferred. Misconceptions about nutritional quality and freshness continue to slow adoption rates. Manufacturers must invest in consumer education campaigns and product positioning strategies to overcome these behavioral challenges and expand market reach.

What are the key opportunities in the frozen vegetables industry?

Growth in Plant-Based and Ready Meal Applications

The global shift toward plant-based diets presents significant opportunities for frozen vegetable manufacturers. Ready-to-eat meals, vegan food products, and meal kits increasingly rely on frozen vegetables as standardized raw materials. Partnerships between frozen food producers and plant-based brands are enabling entry into premium, high-growth segments with improved profit margins and brand differentiation.

Emerging Market Cold-Chain Development

Government investments in cold storage infrastructure across Asia-Pacific, Latin America, and Africa are opening new growth avenues. Countries such as India and Vietnam are rapidly expanding food processing capabilities, enabling export-oriented frozen vegetable production. Improved logistics networks reduce post-harvest losses while allowing manufacturers to access global markets with higher-value processed agricultural products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 35620 Million |

| Market Size in 2026 | USD 38505.22 Million |

| Market Size in 2031 | USD 56839.22 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Frozen mixed vegetables continue to represent the leading product category in the global frozen vegetables market, accounting for nearly 22% of total market share in 2025. The dominance of this segment is primarily driven by increasing consumer preference for convenient, ready-to-cook food solutions that reduce preparation time while maintaining nutritional value. Mixed vegetable products combine commonly consumed vegetables such as peas, corn, carrots, broccoli, beans, and spinach, enabling consumers to prepare complete meals without extensive ingredient preparation. The growing adoption of dual-income household lifestyles, rising urbanization, and demand for efficient meal planning solutions are further accelerating segment expansion.A key growth driver for the leading mixed vegetable segment is its adaptability across global cuisines and food formats, including stir-fries, soups, curries, rice dishes, frozen ready meals, and institutional catering applications. Food manufacturers increasingly develop customized vegetable blends tailored for regional cooking preferences and functional applications, which enhances product differentiation and repeat consumer purchases. Additionally, rising awareness of balanced diets and vegetable intake is encouraging consumers to incorporate frozen vegetables as consistent year-round alternatives to seasonal fresh produce. Continuous innovation in packaging formats, portion-controlled packs, and resealable solutions further strengthens the segment’s market leadership by minimizing food waste and improving storage convenience.

Processing Technology Insights

Individually Quick Frozen (IQF) technology dominates the processing landscape, accounting for approximately 68% share of global frozen vegetable production. The leadership of IQF technology is supported by its ability to preserve the natural texture, color, flavor, and nutritional integrity of vegetables immediately after harvesting. Unlike conventional block freezing methods, IQF ensures individual freezing of each vegetable piece, allowing consumers and foodservice operators to use precise quantities without thawing entire packages. This operational flexibility serves as the primary driver behind the widespread adoption of IQF processing.The leading technology segment is further supported by growing demand from quick-service restaurants, institutional kitchens, and ready-meal manufacturers that require standardized ingredient quality and consistent cooking performance. Advances in cryogenic freezing systems, automation, and energy-efficient refrigeration technologies are improving production throughput while reducing operational costs for processors. Sustainability initiatives aimed at lowering energy consumption and minimizing post-harvest losses are also encouraging manufacturers to upgrade freezing infrastructure. As global supply chains increasingly prioritize shelf-life stability and export efficiency, IQF technology continues to strengthen its position as the preferred processing method across developed and emerging markets.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for nearly 48% of global frozen vegetable sales. The leadership of this segment is primarily driven by strong retail infrastructure, expanding frozen food aisles, and increasing availability of private-label frozen vegetable offerings at competitive price points. Large-format retail stores provide consumers with wide product assortments, promotional pricing strategies, and reliable cold-chain storage, which collectively reinforce purchasing confidence and product accessibility.The leading retail channel is supported by rising consumer preference for one-stop grocery shopping experiences, particularly in urban areas where time efficiency plays a critical role in purchasing behavior. Meanwhile, online grocery platforms are emerging as a complementary growth avenue as advancements in last-mile cold logistics enable safe delivery of temperature-sensitive products. E-commerce adoption accelerated consumer familiarity with frozen foods, encouraging repeat purchases through subscription models and digital promotions. Wholesale distributors continue to play a vital supporting role by supplying restaurants, catering companies, and institutional buyers, ensuring uninterrupted product availability for large-scale food preparation environments.

End-Use Insights

Household consumption represents the largest end-use segment, contributing approximately 52% of total global market demand. The leading position of the household segment is driven by increasing reliance on convenient meal preparation solutions, extended product shelf life, and reduced food wastage compared to fresh vegetables. Consumers increasingly view frozen vegetables as nutritionally comparable to fresh produce due to rapid freezing immediately after harvest, which preserves vitamins and minerals. Rising health awareness, growing home cooking trends, and demand for cost-effective food storage options continue to strengthen household adoption worldwide.Although households dominate current demand, the foodservice industry is emerging as the fastest-growing application area. Expansion of quick-service restaurants, cloud kitchens, and ready-to-eat meal providers is significantly increasing bulk consumption of frozen vegetables. Commercial kitchens benefit from standardized portioning, labor cost reduction, and consistent ingredient availability throughout the year. Additionally, processed food manufacturers increasingly integrate frozen vegetables into packaged meals, soups, snacks, and frozen entrees, supporting industrial demand growth and expanding overall market penetration.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Vegetables Market Segmentations

By Product Type

- Frozen Peas

- Frozen Corn

- Frozen Broccoli

- Frozen Spinach

- Frozen Mixed Vegetables

- Frozen Beans

- Frozen Carrots

- Other Frozen Vegetables

By Processing Technology

- Individually Quick Frozen

- Blast Freezing

- Belt Freezing

- Cryogenic Freezing

By End Use

- Household/Retail Consumption

- Foodservice

- Food Processing Industry

- Institutional Catering

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & E-commerce

- Wholesale & Foodservice Distributors

- Direct B2B Supply

Regional Insights

North America

North America accounts for roughly 27% of the global frozen vegetables market, led by strong consumption across the United States and Canada. Regional growth is primarily driven by high household freezer penetration, well-established cold-chain logistics infrastructure, and consumer preference for convenience-oriented food products. Busy lifestyles and increasing participation of working professionals in urban areas encourage reliance on frozen foods that reduce meal preparation time while ensuring consistent quality. The region also benefits from advanced agricultural mechanization and large-scale vegetable processing facilities that support stable domestic production.Additional regional growth drivers include rising demand for organic frozen vegetables, plant-based diets, and clean-label food products. Retailers are expanding premium and value-added offerings such as seasoned vegetables and ready-to-cook meal kits, enhancing consumer engagement. Strong presence of quick-service restaurant chains and institutional foodservice providers further stimulates commercial demand, while technological innovation in packaging and sustainability initiatives contributes to long-term market expansion.

Europe

Europe holds the largest regional share at approximately 34% in 2025, supported by strong consumption across Belgium, Germany, France, and the Netherlands. The region’s leadership is reinforced by highly integrated agricultural supply chains and advanced freezing infrastructure, enabling efficient farm-to-processing operations. Belgium serves as a major processing and export hub, supplying frozen vegetables across international markets due to its favorable agricultural productivity and logistical connectivity.Regional growth is driven by widespread consumer acceptance of frozen vegetables as nutritionally equivalent to fresh produce, supported by strong awareness of food waste reduction and sustainability. European consumers increasingly prioritize environmentally responsible food choices, encouraging manufacturers to adopt energy-efficient freezing technologies and recyclable packaging solutions. High demand for plant-based diets, convenience meals, and private-label retail products continues to support stable long-term growth across both Western and Eastern European markets.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 9% CAGR, supported by rapid urbanization, rising disposable incomes, and evolving dietary patterns. China leads regional production capacity due to large-scale vegetable cultivation and expanding export-oriented processing industries. India is witnessing accelerated growth driven by government support for food processing infrastructure, increasing cold storage investments, and expansion of organized retail chains.Regional growth drivers also include increasing adoption of modern retail formats, growing middle-class populations, and rising demand for convenience foods among younger consumers. Japan and South Korea maintain mature frozen food markets characterized by high urban density and strong acceptance of ready-to-cook meals. The expansion of e-commerce grocery platforms and improvements in cold-chain logistics across Southeast Asia are further enabling deeper market penetration, positioning Asia-Pacific as a key future growth engine for the global frozen vegetables industry.

Latin America

Latin America accounts for nearly 8% of global demand, led by Brazil and Mexico. Market expansion in the region is supported by retail modernization, increasing supermarket penetration, and growing investments in domestic vegetable processing capabilities. Urban population growth and changing dietary habits are encouraging consumers to adopt frozen food products as practical alternatives to fresh produce with shorter shelf life.Regional growth is further driven by expanding foodservice industries, rising participation of women in the workforce, and increasing exposure to international cuisines that incorporate frozen ingredients. Export-oriented agricultural production is strengthening regional processing industries, while improvements in refrigeration infrastructure and logistics networks are gradually enhancing distribution efficiency across emerging economies.

Middle East & Africa

The Middle East & Africa region accounts for about 7% of global market share, supported primarily by strong import demand in countries such as the United Arab Emirates and Saudi Arabia. Limited domestic agricultural production due to climatic constraints increases reliance on imported frozen vegetables, ensuring consistent demand throughout the year. Expanding retail infrastructure and rising disposable incomes are encouraging wider consumer adoption of frozen food products.Regional growth is strongly linked to the expansion of hospitality, tourism, and large-scale catering industries, which depend heavily on frozen ingredients for operational efficiency and food safety. Rapid urban development, increasing expatriate populations, and rising consumption of international cuisines are further supporting market expansion. Investments in cold storage facilities and logistics modernization across Gulf Cooperation Council countries and parts of Africa are expected to improve supply stability and accelerate long-term market growth.

Key Players in the Frozen Vegetables Market

- Nomad Foods Ltd.

- Conagra Brands Inc.

- McCain Foods Limited

- Lamb Weston Holdings Inc.

- Bonduelle Group

- Greenyard NV

- Birds Eye Limited

- Ardo Group

- J.R. Simplot Company

- Dole Food Company

- B&G Foods Inc.

- Ajinomoto Co., Inc.

- General Mills Inc.

- Iceland Foods Ltd.

- Kerry Group plc