Frozen Prepared Foods Market Size

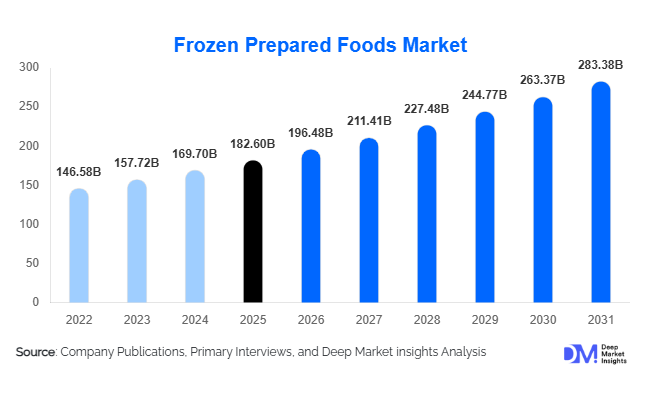

According to Deep Market Insights, the global frozen prepared foods market size was valued at USD 182.6 billion in 2025 and is projected to grow from USD 196.48 billion in 2026 to reach USD 283.38 billion by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The frozen prepared foods market growth is primarily driven by rising urbanization, increasing dual-income households, rapid adoption of convenience foods, and technological advancements in freezing and cold-chain logistics that enhance product quality and shelf life.

Key Market Insights

- Convenience-driven consumption patterns are accelerating demand for ready meals, frozen snacks, and heat-and-eat solutions globally.

- Health-oriented frozen offerings, including plant-based, organic, and low-calorie meals, are reshaping product innovation strategies.

- North America dominates global demand due to mature retail infrastructure and strong frozen food penetration.

- Asia-Pacific is the fastest-growing region, supported by expanding middle-class populations and rapid modern retail expansion.

- E-commerce grocery platforms are strengthening frozen product accessibility through improved last-mile cold-chain delivery.

- Advanced freezing technologies, such as IQF (Individually Quick Frozen), are improving texture retention and consumer acceptance.

What are the latest trends in the frozen prepared foods market?

Premiumization and Health-Focused Frozen Meals

Consumers increasingly perceive frozen foods as nutritionally viable alternatives to fresh meals due to improvements in freezing technologies and ingredient sourcing. Manufacturers are expanding premium ready-meal portfolios featuring clean labels, high-protein formulations, gluten-free options, and plant-based proteins. Functional nutrition, portion control, and calorie-conscious meals are gaining traction among urban professionals and younger consumers. Brands are incorporating global cuisines, organic ingredients, and minimally processed recipes to reposition frozen foods from budget staples to lifestyle products. This premiumization trend allows companies to achieve higher margins while attracting health-conscious consumers who previously avoided frozen categories.

Digital Retail Expansion and Direct-to-Consumer Models

The rapid growth of online grocery platforms has transformed frozen food distribution. Retailers and manufacturers are investing heavily in temperature-controlled logistics, smart packaging, and predictive inventory management to maintain product integrity during delivery. Subscription-based meal kits and direct-to-consumer frozen meal brands are emerging strongly, particularly in North America and Europe. AI-enabled demand forecasting and automated warehouses are improving operational efficiency while reducing food waste. Digital engagement through apps and personalized recommendations is also influencing purchasing behavior, enabling brands to tailor product offerings based on dietary preferences and consumption patterns.

What are the key drivers in the frozen prepared foods market?

Urbanization and Changing Lifestyles

Rapid urban expansion and increasing workforce participation have significantly reduced time available for traditional meal preparation. Frozen prepared foods offer convenience, consistency, and extended shelf life, making them highly attractive to urban households. Rising demand for quick meal solutions among students, professionals, and nuclear families continues to support steady market growth globally.

Advancements in Freezing and Cold Chain Infrastructure

Technological innovations such as blast freezing, cryogenic freezing, and improved packaging solutions preserve nutritional value and taste, overcoming earlier quality perceptions associated with frozen foods. Investments in refrigerated transport and cold storage infrastructure—particularly in emerging economies—are enabling deeper market penetration into tier-2 and tier-3 cities.

Expansion of Modern Retail and Foodservice Channels

Supermarkets, hypermarkets, and quick-service restaurants increasingly rely on frozen prepared foods for operational efficiency and waste reduction. Foodservice operators prefer frozen inputs due to standardized quality and reduced preparation time, driving large-scale procurement globally.

What are the restraints for the global market?

Cold Chain Dependency and Energy Costs

The frozen prepared foods industry depends heavily on uninterrupted refrigeration across production, storage, and transportation stages. Rising electricity prices and infrastructure limitations in developing regions increase operational costs and restrict penetration in rural markets.

Consumer Perception in Emerging Markets

Despite improvements in quality, certain markets still associate frozen foods with preservatives or reduced freshness. Cultural preferences for freshly cooked meals in regions such as South Asia and parts of Africa remain barriers to faster adoption.

What are the key opportunities in the frozen prepared foods industry?

Plant-Based and Alternative Protein Expansion

The growth of plant-based diets presents a significant opportunity for frozen prepared foods manufacturers. Frozen vegan meals, meat alternatives, and protein-rich vegetarian offerings are witnessing rapid adoption in Europe and North America. Companies entering this segment benefit from premium pricing and expanding health-conscious demographics.

Emerging Market Penetration Through Cold Chain Investments

Countries across Southeast Asia, India, Brazil, and the Middle East are investing heavily in refrigerated logistics infrastructure. Government incentives supporting food processing industries are enabling manufacturers to establish local production hubs, lowering costs and improving accessibility.

Foodservice and Institutional Demand Growth

Hotels, airlines, hospitals, and corporate cafeterias increasingly rely on frozen prepared foods to manage labor shortages and ensure consistent food quality. Institutional demand is expanding faster than retail demand in several regions, creating scalable business opportunities for suppliers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 182.60 Billion |

| Market Size in 2026 | USD 196.48 Billion |

| Market Size in 2031 | USD 283.38 Billion |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen prepared foods market is characterized by diverse product offerings, with frozen ready meals leading the landscape. These meals accounted for approximately 28% of the global market share in 2025, primarily driven by the increasing demand for convenient, single-serve meal options among busy working professionals and urban households seeking time-saving solutions. The rise in dual-income families and the adoption of on-the-go lifestyles has further reinforced the popularity of ready meals. Frozen snacks and appetizers hold nearly 22% market share, supported by their growing role in social gatherings, casual entertaining, and quick snacking habits across urban centers. Consumers are increasingly seeking innovative flavors and convenient packaging, fueling demand in this segment. Frozen pizzas, contributing around 15% of the market, continue to perform strongly, especially in North America and Europe, where cultural affinity and frequent consumption patterns sustain growth. Frozen meat-based prepared dishes represent roughly 18% of the market, driven by foodservice adoption, particularly in institutional catering, quick-service restaurants, and hospitality sectors that prioritize standardized menu offerings and efficient meal preparation. The frozen plant-based meals segment, currently at 7%, is the fastest-growing category, benefiting from the global shift toward healthier diets, flexitarian eating patterns, and environmental sustainability considerations. Additionally, frozen ethnic and international cuisine meals, accounting for about 10%, reflect consumers’ evolving palates and a growing interest in global flavors, further supported by travel-inspired consumption trends and multicultural urban populations.

Application Insights

Retail household consumption remains the dominant application segment, contributing over 60% of total demand. This growth is underpinned by the rapid expansion of supermarkets, hypermarkets, and online grocery platforms, as well as the increasing penetration of modern retail formats in emerging economies. Rising consumer awareness regarding convenience, coupled with time-constrained lifestyles, reinforces retail demand. Foodservice applications account for approximately 30% of the market, with quick-service restaurants, institutional catering, and hotel chains adopting frozen prepared foods to optimize kitchen efficiency, reduce labor costs, and ensure menu consistency. Emerging applications such as airline catering and hospitality are experiencing annual growth exceeding 8%, as operators increasingly prefer standardized frozen meal solutions to enhance operational efficiency. Furthermore, export-driven demand is on the rise, particularly from developed markets importing frozen meals from Asia and Eastern Europe, leveraging cost advantages, advanced production technologies, and compliance with international food safety standards. The continued growth of organized retail, cloud kitchens, and meal subscription services is expanding the diversity of applications, creating a robust ecosystem for frozen prepared foods globally.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape, accounting for nearly 48% of global sales. Their extensive cold-chain infrastructure, large product variety, and consumer preference for one-stop shopping facilitate this dominance. Convenience stores, representing about 14% of the market, are particularly prominent in densely populated urban centers of Asia-Pacific, catering to impulse buying and on-the-go consumption. Online grocery platforms are the fastest-growing channel, experiencing over 12% annual growth, driven by improved cold-chain logistics, increased digital adoption, and the convenience of home delivery. Direct-to-consumer subscription models and private-label retail brands are gaining traction, enhancing brand loyalty, offering competitive pricing, and providing customized meal options to cater to specific consumer preferences.

End-Use Industry Insights

Household consumption remains the primary end-use sector; however, the foodservice industry is witnessing rapid adoption of frozen prepared foods due to labor shortages, rising operational costs, and the need for standardized menu offerings. Quick-service restaurants, institutional kitchens, and healthcare facilities are increasingly leveraging frozen foods to reduce preparation time while maintaining quality and consistency. The global foodservice sector, valued above USD 4 trillion, provides a substantial growth platform for frozen meals. Export-oriented production hubs in Poland, Thailand, China, and India are strategically supplying Western markets, capitalizing on cost efficiencies and large-scale manufacturing capabilities. Emerging end-use applications include ready-to-eat nutrition meals for fitness-conscious consumers and medically tailored frozen diets for hospitals, nursing homes, and clinics, reflecting the expanding scope of health-oriented frozen food consumption.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Prepared Foods Market Segmentations

By Product Type

- Ready-to-Eat Frozen Meals

- Frozen Snacks & Appetizers

- Frozen Pizza & Bakery Products

- Frozen Meat & Seafood Prepared Meals

- Frozen Plant-Based & Vegan Meals

- Frozen Breakfast Foods

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Quick Commerce

- Foodservice & Institutional Distribution

- Specialty & Premium Retail Stores

By End-Use

- Household Consumption

- Foodservice Industry

- Institutional Buyers

Regional Insights

North America

North America accounted for approximately 34% of the global frozen prepared foods market in 2025, with the United States alone contributing nearly 28% of global demand. Market growth is driven by high freezer ownership, robust retail infrastructure, and a long-standing culture of convenience food consumption. Innovations in ready-to-eat and plant-based frozen meals, coupled with growing consumer interest in health-conscious and premium products, further propel market expansion. Canada is witnessing steady growth due to increased penetration of private-label products, rising demand for organic and clean-label frozen foods, and continued investment in modern retail formats. Additionally, regional trends such as increased snacking occasions, multicultural food preferences, and convenience-driven urban lifestyles serve as key growth drivers.

Europe

Europe held around 27% market share, led by the U.K., Germany, France, and Italy. European growth is fueled by high consumer awareness of food quality, preference for premium and organic frozen meals, and strong adoption of plant-based alternatives. Regulatory frameworks emphasizing food safety, sustainability, and eco-friendly packaging have encouraged manufacturers to innovate in recyclable and clean-label packaging. The rise of modern retail formats, coupled with busy urban lifestyles and an increasing appetite for international cuisines, also supports regional expansion. Additionally, initiatives to promote healthy and convenient meal solutions in households and the foodservice sector are further bolstering demand.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR. China, Japan, South Korea, and India are major demand centers. Urbanization and rising disposable incomes in China are driving large-scale adoption of frozen prepared foods, while growing e-commerce penetration and modern retail expansion accelerate reach. India is witnessing growth due to enhanced cold storage infrastructure, organized retail proliferation, and increasing awareness of convenience meals among the urban middle class. Japan remains a mature market with high per-capita frozen food consumption, where innovation in ready-to-eat meals, health-oriented products, and premium offerings sustains demand. Regional growth is further supported by changing lifestyles, increased dual-income households, and evolving taste preferences across metropolitan areas.

Middle East & Africa

The Middle East & Africa market is experiencing notable expansion, driven by rising expatriate populations, rapid urbanization, and the expansion of supermarket chains in countries such as the UAE, Saudi Arabia, and South Africa. Imports dominate supply in Gulf nations due to limited domestic production, while local manufacturing is gradually growing to cater to regional demand. Increased consumer exposure to Western eating habits, the growth of modern retail, and the rising popularity of convenient, ready-to-eat meals among working populations are significant growth drivers. Additionally, tourism and hospitality expansion in the region are contributing to rising foodservice applications.

Latin America

Brazil and Mexico lead demand in Latin America, supported by urbanization, modern retail growth, and increasing consumer preference for convenient meal solutions. Rising disposable incomes, busy urban lifestyles, and evolving dietary habits among younger consumers are accelerating adoption. The expansion of supermarkets, hypermarkets, and online grocery platforms facilitates wider product availability, while the growth of foodservice channels, including quick-service restaurants and delivery platforms, supports the regional market. Cultural shifts toward Western eating patterns, combined with the popularity of frozen snacks and ready meals, further enhance market prospects.Governments worldwide are investing heavily in food processing infrastructure and cold-chain modernization. Initiatives such as “Make in India” and China’s food manufacturing modernization programs are encouraging domestic frozen food production. Private companies are expanding automated processing facilities, robotics-enabled packaging lines, and energy-efficient freezing systems. Large multinational manufacturers are allocating significant capital toward capacity expansion and sustainable refrigeration technologies to reduce operational costs and emissions.

Key Players in the Frozen Prepared Foods Market

- Nestlé S.A.

- Conagra Brands Inc.

- General Mills Inc.

- Tyson Foods Inc.

- Kraft Heinz Company

- Unilever PLC

- McCain Foods Limited

- Ajinomoto Co., Inc.

- Nomad Foods Ltd.

- Bellisio Foods Inc.

- Maple Leaf Foods Inc.

- Grupo Bimbo S.A.B. de C.V.

- JBS S.A.

- Fleury Michon

- CP Foods (Charoen Pokphand Foods)