Frozen Pastry Additives Market Size

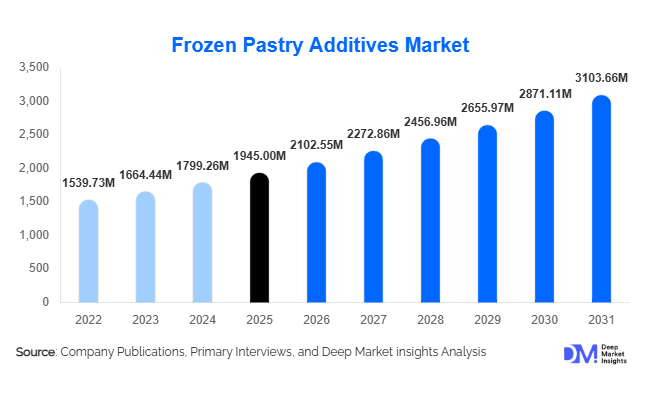

According to Deep Market Insights, the global frozen pastry additives market size was valued at USD 1,945 million in 2026 and is projected to grow from USD 2,102.55 million in 2026 to reach USD 3,103.66 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for ready-to-bake products, expansion of industrial bakeries, rising adoption of enzyme-based and clean-label additive systems, and growth in frozen pastry consumption across emerging markets.

Key Market Insights

- Industrial bakeries dominate additive consumption, as frozen dough preparation requires consistent texture, lamination stability, and extended shelf life.

- Europe and North America lead the market, driven by mature frozen bakery infrastructure, technological adoption, and strong consumer demand for premium pastries.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, westernized diets, and expansion of modern retail and QSR channels.

- Enzyme-based and multifunctional additive blends are gaining traction, enabling clean-label formulations and improved dough performance.

- Frozen pastry types such as croissants and laminated pastries account for the largest additive usage due to complex layering and higher per-unit ingredient demand.

- Distribution is increasingly direct B2B, allowing suppliers to offer technical support and customized formulations to large industrial bakeries.

What are the latest trends in the frozen pastry additives market?

Clean-Label and Enzyme-Based Formulations

Manufacturers are increasingly replacing traditional chemical emulsifiers and preservatives with enzyme-driven and natural ingredient systems. Clean-label formulations appeal to consumer preference for recognizable ingredients while maintaining dough strength, volume, and freeze-thaw stability. Enzyme-based additives are also contributing to reduced waste and improved shelf-life, positioning manufacturers for premium pricing and long-term contracts with multinational bakeries.

Technological Integration in Dough Processing

Advanced additive systems are being integrated into automated industrial dough lines to ensure consistent lamination, gas retention, and texture. Powder and liquid additive blends compatible with automated dosing and high-speed mixers are increasingly adopted. Digital formulation platforms, predictive shelf-life models, and real-time quality monitoring tools are enhancing performance reliability, particularly for multinational bakeries and QSR chains.

What are the key drivers in the frozen pastry additives market?

Rising Demand for Frozen Convenience Foods

Urbanization and busy lifestyles are driving consumer preference for ready-to-bake frozen pastries. Industrial bakeries and retail frozen bakeries rely heavily on functional additives to maintain product quality during storage and distribution, directly fueling market growth.

Expansion of Global Café and QSR Chains

Global café chains and quick service restaurants require standardized product performance across multiple outlets. This has increased reliance on high-quality additives for consistent dough performance, shelf life, and taste, supporting the adoption of enzyme and emulsifier blends.

What are the restraints for the global market?

Regulatory Pressure and Clean-Label Requirements

Strict regulations and consumer demand for natural ingredients challenge manufacturers to reformulate traditional additive systems. R&D costs and compliance burdens can slow adoption among smaller bakeries.

Volatility in Raw Material Prices

Fluctuating prices of vegetable oils, fermentation substrates, and specialty enzymes affect production costs, impacting pricing and margin stability for additive manufacturers.

What are the key opportunities in the frozen pastry additives market?

Emerging Markets and Frozen Bakery Expansion

Asia-Pacific, Latin America, and the Middle East are witnessing rapid adoption of frozen pastry products. Growth in modern retail, cold-chain logistics, and café expansion provides new opportunities for additive suppliers targeting industrial bakeries and QSR chains.

High-Performance Multifunctional Additives

There is strong demand for blends that combine emulsification, freeze-thaw stability, and clean-label properties. Suppliers offering customizable solutions to improve lamination, texture, and shelf-life can gain competitive advantage and long-term contracts with global bakery brands.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1945 Million |

| Market Size in 2026 | USD 2102.55 Million |

| Market Size in 2031 | USD 3103.66 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The frozen pastry additives market is primarily driven by emulsifiers, which represent the leading product category due to their essential role in improving dough machinability, lamination efficiency, and final product volume stability. Emulsifiers enhance fat dispersion and gluten structure, enabling consistent layering in laminated pastries such as croissants, puff pastries, and Danish products, particularly under industrial-scale processing conditions. The growing adoption of automated production lines has further strengthened demand for emulsifier systems that ensure uniform dough performance across high-throughput manufacturing environments. The leading segment driver for emulsifiers is the increasing need for standardized product quality and reduced production variability in large-scale frozen bakery operations.Enzymes and preservative systems are gaining significant traction as manufacturers increasingly shift toward clean-label and enzyme-based formulation strategies. Enzymatic solutions improve dough extensibility, fermentation tolerance, and shelf-life without relying heavily on synthetic additives, aligning with evolving consumer expectations for transparency and natural ingredients. Meanwhile, preservative systems remain important for maintaining microbiological stability during extended frozen storage and long-distance distribution.Powder additives continue to dominate the formulation format landscape due to their superior shelf stability, ease of storage, and compatibility with automated dosing systems. Powder formats allow precise ingredient incorporation, reduce handling complexity, and integrate seamlessly into both dry-mix and hybrid liquid systems. The leading growth driver for powder additives is their operational efficiency within industrial bakeries seeking scalable and cost-effective production solutions.

Application Insights

Industrial dough preparation represents the leading application segment, supported by the growing industrialization of bakery production worldwide. Additives are primarily incorporated during this stage to ensure uniform ingredient dispersion, optimized gluten development, and predictable fermentation behavior. The leading segment driver is the rising demand for process consistency across centralized manufacturing facilities supplying multiple retail and foodservice channels. As frozen pastry supply chains expand, manufacturers increasingly rely on additive systems that stabilize dough properties before freezing.Freeze-thaw stability enhancement has emerged as a critical application area as global frozen pastry distribution networks continue to expand. Additives designed to protect yeast viability, moisture retention, and structural integrity help maintain product quality through repeated temperature fluctuations during transportation and storage. This application is gaining importance due to the rapid globalization of frozen bakery trade and cross-border distribution.Texture and flavor stabilization remains a key focus area, particularly for premium laminated and filled pastries where sensory quality strongly influences consumer purchasing decisions. Additives help maintain flakiness, softness, and flavor retention after baking, ensuring consistent consumer experiences across retail and foodservice formats. The increasing premiumization of frozen bakery products acts as the primary driver supporting growth in this segment.

Distribution Channel Insights

Direct business-to-business (B2B) contracts dominate distribution channels, as additive manufacturers increasingly position themselves as technical solution providers rather than commodity suppliers. Through direct partnerships with industrial bakeries and multinational food producers, suppliers offer formulation expertise, customized additive blends, and ongoing process optimization support. The leading driver for this channel is the growing complexity of frozen pastry formulations, which requires close collaboration between ingredient suppliers and bakery manufacturers.Ingredient distributors and specialty bakery suppliers play an important complementary role, particularly in emerging markets where smaller bakeries rely on regional distribution networks for sourcing technical ingredients. These intermediaries help bridge accessibility gaps and enable market penetration beyond large industrial customers.Digital procurement platforms and online ingredient sourcing channels are gradually emerging as transformative distribution models. These platforms improve supply chain transparency, facilitate faster sourcing decisions, and enhance traceability requirements increasingly demanded by multinational food companies. Growth in digital sourcing is supported by the broader digitalization of food manufacturing procurement systems.

End-Use Insights

Industrial bakeries account for the largest share of global additive consumption, representing nearly half of total demand due to their reliance on standardized formulations and high-volume frozen dough production. The leading segment driver is the ongoing consolidation of bakery manufacturing into centralized industrial facilities that prioritize efficiency, consistency, and extended product shelf life.Quick-service restaurants (QSRs) and retail frozen bakery brands represent rapidly expanding end-use segments, supported by rising consumer demand for convenience foods and ready-to-bake pastry solutions. QSR operators increasingly adopt frozen dough formats to reduce labor dependency while ensuring uniform product quality across locations. In-store supermarket bakeries are also expanding adoption as retailers focus on fresh-baked experiences supported by frozen semi-finished products.Emerging applications include airline catering services, automated bakery vending solutions, and export-oriented frozen pastry production hubs located primarily in Europe and North America. These new consumption channels are creating incremental demand for multifunctional additive systems capable of maintaining performance across diverse preparation environments.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Pastry Additives Market Segmentations

By Additive Type

- Emulsifiers

- Enzymes

- Preservatives & Shelf-Life Extenders

- Texture & Structure Improvers

- Flavor & Aroma Enhancers

- Color & Appearance Enhancers

- Functional Additive Blends

By Functionality

- Dough Strengthening

- Freeze-Thaw Stability Enhancement

- Shelf-Life Extension

- Volume Improvement & Aeration

- Texture Softening & Moisture Retention

- Flavor Stabilization

By Pastry Type

- Croissants & Laminated Pastries

- Danish & Sweet Pastries

- Puff Pastries

- Filled Frozen Pastries

- Ready-to-Bake Artisan Pastries

By Form

- Powder Additives

- Liquid Additives

- Paste/Gel Systems

By End-Use Industry

- Industrial Bakeries

- Quick Service Restaurants

- Retail Frozen Bakery Brands

- Foodservice & HoReCa

- In-Store Supermarket Bakeries

By Distribution Channel

- Direct B2B Supply Contracts

- Ingredient Distributors

- Specialty Bakery Ingredient Suppliers

Regional Insights

North America

North America represents a mature yet innovation-driven market, led by the United States, where large-scale industrial bakeries, established QSR chains, and in-store retail bakery formats drive consistent additive consumption. The region accounted for approximately 27% of global market share in 2025. Growth is supported by strong demand for extended shelf-life products, labor cost optimization through frozen dough adoption, and increasing investment in automation technologies. Additional regional growth drivers include rising consumption of convenience bakery products, expansion of premium frozen pastry offerings, and continuous product innovation by ingredient manufacturers focused on clean-label and enzyme-based solutions. Moderate but stable growth is expected during the 2026–2031 forecast period as manufacturers prioritize efficiency and product differentiation.

Europe

Europe remains the dominant global market, accounting for nearly 34% of consumption in 2025, supported by deep-rooted pastry traditions and advanced frozen bakery infrastructure. Countries such as France, Germany, and Italy lead regional demand due to strong artisanal heritage combined with highly industrialized export-oriented bakery production. Regional growth is driven by widespread adoption of frozen dough technology, strong intra-European trade, and increasing demand for premium laminated pastries across retail and foodservice sectors. Sustainability initiatives and regulatory emphasis on ingredient transparency are further encouraging adoption of enzyme-based and clean-label additive systems. Although the market is mature, steady demand growth continues due to innovation in premium and specialty pastry segments.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, led by China and India, with projected growth rates of approximately 10–11% CAGR. Rapid urbanization, expansion of café culture, and rising disposable incomes are accelerating consumption of Western-style baked goods. The expansion of modern retail chains, convenience stores, and international QSR brands is driving large-scale adoption of frozen bakery formats. Regional growth is further supported by investments in industrial bakery infrastructure, increasing cold-chain logistics capabilities, and growing demand for multifunctional enzyme systems that improve dough tolerance under varying climatic conditions. Localization of frozen pastry production is emerging as a key driver, reducing reliance on imports and boosting additive consumption.

Latin America

Latin America’s market is led by Brazil and Mexico, where expanding urban populations and modern retail development are increasing frozen bakery penetration. Growth is driven by the modernization of traditional bakeries transitioning toward semi-industrial production models and the expansion of QSR chains across major metropolitan areas. Rising imports of frozen pastries and increasing adoption of standardized formulations are encouraging additive usage. Improvements in cold storage infrastructure and growing consumer demand for convenient ready-to-bake products further support regional market expansion.

Middle East & Africa

The Middle East & Africa region is experiencing gradual but steady growth, with demand concentrated in high-income markets such as the UAE and Saudi Arabia. Growth drivers include strong reliance on imported frozen pastries, expanding hospitality and tourism sectors, and increasing adoption of Western-style bakery products. In Africa, emerging production hubs in countries such as South Africa and Kenya are supporting intra-regional frozen pastry distribution networks, which in turn drive additive demand. Expanding supermarket penetration, urban population growth, and improving cold-chain logistics infrastructure are expected to accelerate long-term market development across the region.

Key Players in the Frozen Pastry Additives Market

- Kerry Group

- IFF (International Flavors & Fragrances)

- Lesaffre

- DSM-Firmenich

- Corbion

- Puratos Group

- AB Mauri

- Lallemand Inc.

- Novozymes

- Archer Daniels Midland (ADM)

- Bakels Group

- Tate & Lyle

- Palsgaard A/S

- SternEnzym

- Oriental Yeast Co., Ltd.