Frozen Pastries Market Size

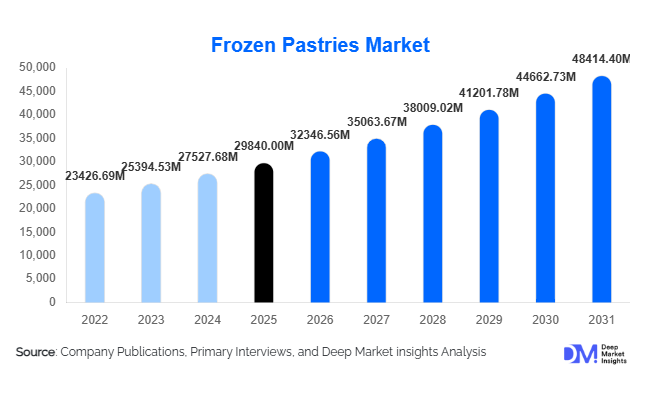

According to Deep Market Insights, the global frozen pastries market size was valued at USD 29,840 million in 2025 and is projected to grow from USD 32,346.56 million in 2026 to reach USD 48,414.40 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The frozen pastries market growth is driven by rising demand for convenient bakery products, expansion of quick-service restaurant (QSR) chains, increasing adoption of frozen bakery solutions in foodservice operations, and changing consumer lifestyles favoring ready-to-bake and ready-to-eat formats.

Urbanization, dual-income households, and evolving breakfast consumption habits are accelerating demand globally. Frozen pastries offer extended shelf life, reduced food waste, and operational efficiency for retailers and foodservice providers, making them increasingly preferred over freshly prepared alternatives. Technological improvements in freezing techniques such as blast freezing and individually quick frozen (IQF) processing have enhanced product texture and quality, enabling manufacturers to deliver premium bakery experiences with minimal preparation time.

Key Market Insights

- Convenience-driven consumption patterns are boosting demand for ready-to-bake croissants, puff pastries, and Danish products across retail and foodservice channels.

- Foodservice and QSR chains account for a major demand share, supported by standardized baking processes and reduced labor requirements.

- Europe dominates global production and consumption, led by strong bakery traditions and advanced cold-chain infrastructure.

- Asia-Pacific is the fastest-growing region, fueled by urbanization and westernization of eating habits.

- Private-label frozen bakery products are expanding rapidly through supermarkets and hypermarkets.

- Technological innovation in freezing and dough fermentation is improving product quality and supporting premiumization.

What are the latest trends in the frozen pastries market?

Premiumization and Artisan-Style Frozen Products

Consumers increasingly expect bakery-quality experiences at home, pushing manufacturers toward artisan-style frozen pastries featuring clean-label ingredients, butter-based laminations, and traditional European recipes. Premium frozen croissants, pain au chocolat, and specialty Danish pastries are gaining traction across retail shelves. Brands are investing in slow-fermentation dough technologies and natural ingredients to replicate freshly baked textures. This trend supports higher margins while expanding appeal among premium consumers seeking café-quality products without bakery visits.

Expansion of Ready-to-Bake Formats

Ready-to-bake frozen pastries are rapidly growing as retailers and foodservice operators seek operational efficiency. Supermarkets increasingly provide in-store baking solutions using frozen dough, ensuring fresh aroma and quality while minimizing wastage. Foodservice chains benefit from consistent portion control and simplified kitchen operations. Consumers also prefer bake-at-home products that deliver freshness while allowing customization. Growth in air fryer usage and compact home ovens further strengthens adoption of this segment globally.

What are the key drivers in the frozen pastries market?

Growth of Quick-Service Restaurants and Café Chains

The rapid expansion of QSRs, coffee chains, and bakery cafés globally is a major growth driver. Frozen pastries enable standardized product quality across locations while reducing dependence on skilled bakers. Global café chains increasingly rely on frozen laminated dough products to maintain operational scalability. Expansion of franchise models in emerging markets significantly increases bulk procurement of frozen bakery goods.

Rising Demand for Convenience Foods

Busy lifestyles and increasing workforce participation have accelerated demand for convenient meal solutions. Frozen pastries offer minimal preparation time and extended storage flexibility, making them ideal for breakfast and snack occasions. Consumers increasingly prefer products that balance convenience with indulgence, positioning frozen pastries as a hybrid between ready meals and premium bakery products.

Advancements in Cold Chain Infrastructure

Improved cold storage logistics and frozen distribution networks have enabled deeper penetration into emerging markets. Investments in refrigerated transport and retail freezer capacity are supporting wider availability of frozen bakery products across supermarkets, convenience stores, and online grocery platforms.

What are the restraints for the global market?

Perception of Frozen Foods as Less Fresh

Despite technological advancements, some consumers still associate frozen foods with lower freshness compared to freshly baked products. This perception limits adoption in certain developing markets where traditional bakeries remain dominant.

Volatility in Raw Material Prices

Fluctuating prices of wheat, butter, dairy fats, and energy significantly impact production costs. Laminated pastries require high butter content, making manufacturers sensitive to dairy price volatility, which pressures profit margins and pricing strategies.

What are the key opportunities in the frozen pastries industry?

Emerging Market Retail Expansion

Modern retail expansion across Asia, the Middle East, and Latin America presents significant opportunities. Growing supermarket penetration increases freezer availability, enabling frozen pastry brands to reach new consumers. Urban middle-class populations are increasingly adopting Western breakfast habits, creating sustained demand growth.

Plant-Based and Health-Oriented Innovation

The introduction of vegan pastries, gluten-reduced formulations, and reduced-sugar variants provides opportunities for differentiation. Manufacturers investing in alternative fats and functional ingredients are attracting health-conscious consumers without sacrificing taste or texture.

Foodservice Automation and Centralized Baking

Centralized production models using frozen dough allow foodservice operators to scale efficiently. Hotels, airlines, and institutional catering increasingly adopt frozen pastry solutions to reduce labor dependency and improve consistency. Automation-compatible pastry formats represent a major growth avenue for suppliers.

Product Type Insights

The global frozen pastries market demonstrates strong product diversification; however, croissants continue to represent the dominant product category, accounting for approximately 28% of total market revenue in 2025. Their leadership is primarily supported by widespread global familiarity, consistent demand across cafés and quick-service restaurants, and their suitability for frozen storage without significant quality degradation. The layered lamination structure of croissants allows manufacturers to maintain texture and flavor integrity after freezing and reheating, making them highly preferred within foodservice environments that require operational efficiency and product consistency. Additionally, the growing popularity of breakfast-on-the-go culture and premium coffee consumption has significantly strengthened croissant demand across both developed and emerging economies.Puff pastries follow closely due to their exceptional versatility across both sweet and savory applications. Foodservice operators increasingly rely on puff pastry formats for menu innovation, enabling rapid preparation of snacks, appetizers, and desserts while minimizing labor intensity. Danish pastries are witnessing accelerated adoption within premium retail and artisanal bakery segments as consumers increasingly seek indulgent and specialty bakery experiences. Rising disposable incomes and consumer willingness to pay for premium frozen bakery products are supporting category expansion, particularly in urban markets.Frozen tarts and specialty pastries are gaining traction within dessert-focused menus across hotels, cafés, and institutional catering operations, where standardized presentation and portion control are essential. Meanwhile, ready-to-proof dough formats are emerging as the fastest-growing product segment, driven by retailers’ emphasis on in-store baking experiences that combine the convenience of frozen logistics with the perception of freshly baked goods. The leading segment driver across product categories remains operational efficiency combined with consistent product quality, enabling bakery operators to reduce skilled labor dependency while maintaining premium product standards.

Application Insights

Foodservice applications dominate the frozen pastries market, accounting for nearly 54% of total demand in 2025, supported by rapid expansion of quick-service restaurants, café chains, and hospitality establishments worldwide. Frozen pastries enable standardized preparation, reduced food waste, and faster service turnaround, making them highly suitable for high-volume foodservice operations. The leading driver for this segment is the increasing need for scalable and labor-efficient bakery solutions amid rising workforce costs and operational complexity.Retail household consumption continues to expand steadily as consumers increasingly adopt convenient meal and snack solutions compatible with busy lifestyles. The growing penetration of home ovens, air fryers, and frozen-ready appliances has enabled consumers to recreate bakery-style experiences at home. Additionally, the pandemic-driven shift toward home cooking established lasting behavioral changes that continue to support frozen bakery product adoption.Institutional catering represents an emerging but strategically important application segment, including airline catering, educational institutions, hospitals, and corporate cafeterias. Large-scale catering providers prefer frozen pastries due to their extended shelf life, standardized quality, and predictable inventory management. Increasing global air travel recovery and expansion of corporate dining programs are expected to strengthen long-term demand within this segment.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel, accounting for approximately 42% of global sales, supported by expanding frozen food aisles and aggressive private-label product development. Retailers increasingly prioritize frozen bakery offerings to enhance margins while providing consumers with affordable premium alternatives. The leading driver within this segment is the modernization of retail infrastructure combined with consumer trust in organized retail supply chains that ensure product safety and freshness.Foodservice distributors continue to play a critical role in market expansion by enabling bulk procurement and efficient logistics for restaurants, hotels, and institutional buyers. Their integrated cold-chain capabilities allow manufacturers to scale distribution across multiple regions while maintaining product integrity.Online grocery platforms represent the fastest-growing distribution channel, fueled by rapid e-commerce adoption and advancements in last-mile cold-chain delivery systems. Digital platforms allow brands to expand geographic reach while offering wider product assortments and subscription-based purchasing models. Increasing consumer preference for convenience and contactless purchasing is accelerating the digital transformation of frozen food retail globally.

End-Use Insights

Quick-service restaurants constitute the largest end-use segment, contributing nearly 38% of total demand due to standardized menus, high customer turnover, and continuous product availability requirements. Frozen pastries enable QSR operators to deliver consistent taste profiles across multiple outlets while minimizing preparation time and operational variability. The leading segment driver is the global expansion of organized foodservice chains seeking scalable and cost-efficient bakery solutions.Hotels and cafés are rapidly increasing adoption of premium frozen pastries as they aim to enhance menu variety without expanding in-house baking infrastructure. Luxury hospitality operators increasingly rely on frozen premium pastry imports to maintain consistent quality standards across locations. Household consumption is also rising steadily as consumers prioritize convenient breakfast and snack solutions aligned with modern lifestyles.Export-oriented demand is gaining importance as European manufacturers expand shipments to Asia and the Middle East, regions experiencing rising bakery consumption driven by urbanization and evolving dietary preferences. International trade in frozen pastries benefits from extended shelf life and improved global cold-chain logistics, enabling cross-border market expansion.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

Europe

Europe maintains the largest share of the global frozen pastries market, accounting for approximately 36% in 2025, supported by a deeply rooted bakery culture and advanced manufacturing capabilities. Countries such as France, Germany, Italy, and the United Kingdom lead regional consumption and production, benefiting from well-established bakery traditions and strong export networks. France alone contributes nearly 9% of global demand, driven by high domestic croissant consumption and significant international exports.Regional growth is further driven by continuous technological innovation in freezing and dough lamination processes, enabling premium product preservation and large-scale industrial production. Strong private-label penetration across European retail chains, increasing demand for artisanal-style frozen products, and sustainability-focused packaging innovations are supporting market maturity. Additionally, labor shortages within traditional bakeries are accelerating adoption of frozen solutions that reduce dependence on skilled bakers while maintaining authentic product quality.

North America

North America accounts for approximately 27% of global market share, led primarily by the United States and Canada. The region benefits from a highly developed retail ecosystem and strong consumer preference for convenience-oriented foods. Expansion of café culture, specialty coffee chains, and breakfast-focused quick-service restaurants continues to stimulate frozen pastry demand.Regional growth drivers include rising dual-income households, increasing reliance on ready-to-bake foods, and strong penetration of household freezers enabling bulk purchasing behavior. Private-label innovation across major supermarket chains has intensified competition while improving affordability for consumers. Furthermore, investments in automated bakery manufacturing and advanced cold-chain logistics are enhancing production efficiency and expanding product availability across urban and suburban markets.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market and is projected to expand at a CAGR exceeding 10% through 2031. Key markets including China, Japan, South Korea, and India are witnessing rapid adoption of Western-style bakery products among urban consumers. Rising middle-class populations, increasing disposable incomes, and evolving breakfast consumption habits are significantly reshaping regional food preferences.Growth is strongly supported by aggressive expansion of international café chains and local bakery franchises across metropolitan areas. Modern retail development and e-commerce grocery platforms are improving frozen product accessibility, while investments in domestic cold-chain infrastructure are reducing distribution constraints. Additionally, younger consumers’ preference for premium convenience foods and exposure to global culinary trends through social media are accelerating frozen pastry penetration across emerging Asian economies.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, led by the UAE, Saudi Arabia, and South Africa. Expansion of tourism and hospitality sectors plays a central role in driving demand, as hotels, resorts, and airline catering services increasingly rely on frozen pastries to maintain consistent quality and operational efficiency.Regional growth drivers include rising expatriate populations, increasing premium food consumption, and rapid development of modern retail infrastructure. Governments investing in tourism diversification and aviation expansion are indirectly supporting frozen bakery demand through institutional catering channels. Furthermore, harsh climatic conditions make frozen logistics particularly advantageous compared to fresh bakery distribution, reinforcing long-term adoption across the region.

Latin America

Latin America, led by Brazil and Mexico, continues to demonstrate growing demand for frozen pastries supported by urbanization and expansion of organized retail chains. Increasing consumer exposure to international bakery formats and café culture is gradually reshaping traditional consumption patterns.Regional growth is driven by improving cold-chain logistics, rising imports of European frozen bakery products, and expanding supermarket penetration in urban centers. Economic modernization and increasing participation of women in the workforce are contributing to higher demand for convenient ready-to-bake foods. Additionally, foodservice sector recovery and franchise expansion across major cities are strengthening long-term market opportunities for frozen pastry manufacturers.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Frozen Pastries Market

- Grupo Bimbo

- Aryzta AG

- Lantmännen Unibake

- General Mills

- Conagra Brands

- Vandemoortele

- Europastry S.A.

- Bridor (LeDuff Group)

- Flowers Foods

- Nestlé S.A.

- Premier Foods

- McCain Foods (Bakery division)

- Delifrance

- Dawn Foods

- Rich Products Corporation