Frozen Orange Juice Concentrate Market Size

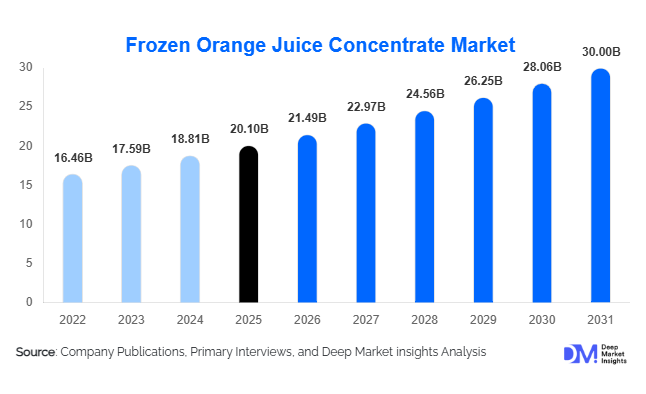

According to Deep Market Insights,the global frozen orange juice concentrate market size was valued at USD 20.1 billion in 2025 and is projected to grow from USD 21.49 billion in 2026 to reach USD 30.00 billion by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for long-shelf-life citrus beverages, rising industrial use in beverage processing, and expanding retail and e-commerce distribution channels for frozen juice products.

Key Market Insights

- Frozen orange juice concentrate remains the preferred form of citrus-based beverages for industrial manufacturers and retail consumers due to cost efficiency, convenience, and long shelf life.

- North America and Europe dominate the market, supported by advanced processing infrastructure, widespread consumption, and mature cold-chain logistics.

- Asia-Pacific is emerging as the fastest-growing region, driven by rising urbanization, growing middle-class incomes, and increasing retail penetration in countries such as China and India.

- Retail and industrial applications both support market expansion, with retail consumption capturing significant household demand and industrial use in soft drinks, juice blends, and foodservice growing steadily.

- Technological advancements in freezing, cold storage, and supply chain optimization are improving product quality, reducing losses, and enhancing market reach.

- Value-added and fortified concentrates, including low-sugar, vitamin-enriched, and functional juice variants, are gaining popularity and driving premium product adoption globally.

What are the latest trends in the frozen orange juice concentrate market?

Functional and Fortified Juice Products

Manufacturers are increasingly offering frozen orange juice concentrates fortified with additional vitamins, minerals, and functional ingredients to meet rising consumer health consciousness. Low-sugar and reduced-calorie variants are being positioned as healthier alternatives to traditional frozen concentrates, catering to diet-conscious and premium segments. This trend is especially prominent in North America and Europe, where consumers prioritize nutritional content and clean-label products.

Industrial and Foodservice Integration

Frozen orange juice concentrate is widely used in foodservice and beverage processing sectors due to its cost-efficiency and long shelf life. Beverage manufacturers are incorporating concentrates into soft drinks, smoothies, and blended beverages, ensuring consistency of taste and reducing production complexity. Restaurants, cafes, and institutional foodservice operations also favor concentrates for bulk usage, which strengthens steady demand across commercial channels.

What are the key drivers in the frozen orange juice concentrate market?

Rising Global Citrus Consumption

Increasing awareness of citrus health benefits, particularly vitamin C content, has driven global orange juice consumption. Households and industrial buyers are leveraging frozen concentrates as a reliable source of citrus beverages, especially in regions with limited fresh orange availability. This consistent demand underpins growth in both retail and industrial segments.

Convenience and Shelf-Life Advantages

Frozen concentrates provide logistical and storage benefits over fresh juice, reducing spoilage and inventory risk. Their concentrated form lowers storage volume and shipping costs, making them attractive for global distribution. These features are particularly valuable in emerging markets where cold-chain infrastructure is developing.

Expansion of Retail and Online Channels

Growing supermarket and hypermarket presence, along with e-commerce grocery platforms, has increased product accessibility to end consumers. Digital platforms allow for direct-to-consumer sales, promoting premium and fortified variants. This trend has helped frozen orange juice concentrates penetrate younger, tech-savvy demographics seeking convenience and healthy beverage options.

What are the restraints for the global market?

Raw Material and Crop Volatility

Orange production is highly sensitive to climate conditions, diseases such as citrus greening, and seasonal variability, particularly in key suppliers like Brazil and Florida. Supply fluctuations and price volatility can negatively impact concentrate availability and profit margins for manufacturers.

Consumer Shift Toward Fresh and Cold-Pressed Juices

Increasing health awareness has driven some consumers to prefer fresh-squeezed or cold-pressed juices over frozen concentrates. This trend is more pronounced in premium urban markets, potentially limiting growth among health-conscious segments.

What are the key opportunities in the frozen orange juice concentrate market?

Emerging Market Expansion

Countries in Asia-Pacific, including China and India, offer significant growth potential due to rising urbanization, expanding retail networks, and growing middle-class incomes. Localized marketing, supply chain expansion, and strategic partnerships can help manufacturers capture new demand in these high-growth regions.

Value-Added and Functional Product Launches

Developing fortified, low-sugar, and functional frozen orange juice concentrates presents opportunities to capture health-conscious consumers globally. Innovation in formulations, flavor blends, and nutritional enhancements can differentiate brands and enable premium pricing strategies.

Partnerships with Industrial and Foodservice Channels

Collaborating with beverage manufacturers, cafes, and institutional buyers ensures steady volume sales and recurring revenue streams. This also allows companies to innovate in blended beverages, smoothies, and ready-to-drink products, expanding the applications of frozen orange juice concentrates.

Product Type Insights

Pure orange juice concentrate continues to dominate the global frozen concentrate market, representing approximately 45–50% of the segment. Its leading position is driven by widespread adoption in industrial beverage processing, high retail demand, and its versatility in juice blends, soft drinks, and functional beverages. Mixed fruit blends with orange as the primary base are gaining traction, appealing to consumers seeking flavor variety and nutritional benefits. Additionally, fortified and functional variants, enriched with vitamins or minerals, are witnessing rapid growth in health-conscious and premium markets, catering to the rising consumer preference for nutrient-dense beverages.

Application Insights

Retail consumption remains the largest application segment, accounting for nearly 45–50% of market demand. Households prefer frozen concentrates for home-prepared juices due to their convenience, cost-effectiveness, and extended shelf life. Industrial beverage processing follows closely, fueled by demand from soft drinks, juice blends, and foodservice operations. Emerging applications, including smoothies, sports drinks, and functional beverages, are expected to drive incremental growth over the forecast period as manufacturers innovate to meet the preferences of health-focused and younger consumer demographics.

Distribution Channel Insights

Offline retail channels, such as supermarkets and hypermarkets, dominate sales, capturing approximately 60–65% of the market share due to product visibility, consumer trust, and established distribution networks. Meanwhile, online platforms are witnessing accelerated growth, offering direct-to-consumer access, broader product assortments, and premium or specialty variants. E-commerce is particularly impactful in urban and high-income regions, supporting the adoption of fortified and functional concentrates and enabling manufacturers to reach niche consumer segments more efficiently.

| By Product Type | By Form | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds the largest regional share, approximately 30–32%, with the United States leading global demand. Growth is driven by high per-capita juice consumption, sophisticated processing infrastructure, and widespread retail and e-commerce penetration. Health-conscious trends have further fueled the adoption of fortified and functional concentrates. Industrial use remains strong, particularly in beverage manufacturing and foodservice sectors, while household demand continues to grow due to convenience and brand trust. Expansion of premium and organic juice variants is expected to support sustained regional growth.

Europe

Europe accounts for around 25% of the market, with Germany, the United Kingdom, and France as key contributors. Growth is underpinned by high consumer health awareness, strong demand for premium juices, and well-developed cold-chain logistics. Both retail and industrial applications are significant, with fortified, low-sugar, and functional concentrates seeing increasing adoption. Rising interest in natural and sustainably sourced products, coupled with regulatory support for fortified beverages, continues to drive market expansion across European countries.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with China, India, and Japan leading demand. Rapid urbanization, rising disposable incomes, and expansion of organized retail channels are primary growth drivers. The retail segment dominates due to increasing consumer preference for convenient, ready-to-use juice products, while industrial applications are expanding as local beverage manufacturing and foodservice sectors develop. Consumer trends toward healthier lifestyles and functional beverages, combined with rising awareness of imported and premium products, are fueling sustained regional growth.

Latin America

Latin America’s market is primarily driven by Brazil and Mexico, where domestic citrus production supports both retail and industrial consumption. Industrial applications dominate, particularly for frozen orange juice concentrates used in beverages and export markets. Growth is supported by well-established processing infrastructure, strong agricultural output, and increasing investment in value-added products. Retail adoption, while limited compared to industrial use, is gradually rising due to urbanization and expanding supermarket networks in major cities.

Middle East & Africa

Demand in the Middle East is concentrated in high-income countries such as the UAE and Saudi Arabia, driven by premium and health-focused consumer preferences, as well as a growing foodservice sector. In Africa, countries like South Africa and Egypt serve mainly as supply hubs, leveraging robust citrus production to feed both domestic processing and international exports. Growth in the region is supported by expanding modern retail chains, rising awareness of fortified beverages, and increasing investment in cold-chain infrastructure to support year-round product availability.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Frozen Orange Juice Concentrate Market

- Companhia de Bebidas das Americas (Ambev)

- Tropicana Products, Inc.

- Minute Maid (The Coca-Cola Company)

- Citrosuco S.A.

- Louis Dreyfus Company

- Simplot Australia Pty Ltd

- Funkaplast GmbH

- Ardo Group

- Florida’s Natural Growers

- Sunkist Growers, Inc.

- Refresco Group

- Parmalat S.p.A.

- Ocean Spray Cranberries, Inc.

- Del Monte Foods, Inc.

- Sun Pacific