Frozen Novelty Market Size

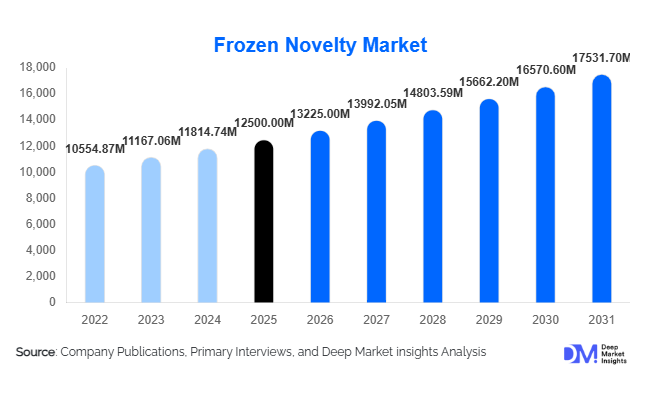

According to Deep Market Insights, the global frozen novelty market size was valued at USD 12,500 million in 2026 and is projected to grow from USD 13,225.00 million in 2027 to reach USD 17,531.70 million by 2031, expanding at a CAGR of 5.8% during the forecast period (2026-2031). The frozen novelty market growth is primarily driven by rising demand for convenient indulgent snacks, rapid expansion of premium frozen dessert offerings, and increasing consumer preference for functional and plant-based frozen treats across global retail channels.

Key Market Insights

- Frozen novelties are shifting from seasonal treats to year-round snacks, driven by urban consumption patterns and improved cold chain distribution.

- Premium and artisanal ice cream bars are gaining strong traction due to rising willingness to pay for indulgent, high-quality desserts.

- Asia-Pacific dominates consumption growth, supported by rising disposable income and rapid retail expansion.

- Plant-based frozen novelties are emerging as a high-growth category due to increasing vegan and lactose-free demand.

- E-commerce and quick commerce platforms are reshaping distribution, enabling faster delivery of frozen desserts.

- North America remains the most mature market, with high per-capita consumption and strong brand loyalty.

What are the latest trends in the frozen novelty market?

Rise of Plant-Based and Functional Frozen Novelties

Consumers are increasingly shifting toward plant-based frozen desserts made from almond, oat, and coconut bases. Functional frozen novelties enriched with protein, probiotics, and low-sugar formulations are gaining traction among health-conscious consumers. Manufacturers are innovating with clean-label ingredients, keto-friendly formulations, and allergen-free products to cater to expanding dietary preferences. This trend is particularly strong in North America and Europe, where wellness-oriented consumption is shaping product innovation strategies.

Expansion of Premium and Experiential Dessert Formats

The market is witnessing strong growth in premium frozen novelties such as layered ice cream bars, filled cones, and gourmet popsicles. Consumers are increasingly seeking experiential desserts with exotic flavors, multi-texture formats, and indulgent coatings. Social media influence and food aesthetics are also driving demand for visually appealing frozen novelties. Brands are investing in artisanal positioning, limited-edition flavors, and collaboration-based product launches to strengthen consumer engagement.

What are the key drivers in the frozen novelty market?

Rising Demand for On-the-Go Convenience Foods

The fast-paced urban lifestyle is significantly driving demand for portable and ready-to-eat frozen desserts. Ice cream bars, popsicles, and single-serve novelties are increasingly preferred as impulse snacks. Expansion of convenience stores and quick commerce platforms has further strengthened accessibility, especially in densely populated urban regions. This trend is particularly strong among working professionals and younger consumers.

Growing Premiumization of Frozen Desserts

Consumers are increasingly willing to pay premium prices for high-quality ingredients, exotic flavors, and innovative textures. This has led to rapid expansion of artisanal and gourmet frozen novelty segments. Premium branding, sustainable sourcing, and limited-edition offerings are enhancing product differentiation and boosting margins across global markets.

Increasing Demand for Health-Oriented Frozen Products

Health-conscious consumers are driving demand for low-sugar, high-protein, and dairy-free frozen novelties. Functional ingredients such as probiotics and natural sweeteners are being widely adopted. This shift is expanding the consumer base beyond traditional indulgence buyers to fitness-focused and dietary-restricted populations.

What are the restraints for the global market?

High Cold Chain and Logistics Costs

Frozen novelty products require continuous cold storage and temperature-controlled logistics, making distribution highly expensive. This significantly impacts profitability, especially in developing economies where cold chain infrastructure is still evolving. Energy costs and transportation inefficiencies further add to operational challenges.

Regulatory Pressure on Sugar and Food Composition

Increasing global regulations on sugar content, labeling transparency, and artificial additives are creating compliance challenges for manufacturers. Companies are required to reformulate products, which increases R&D costs and may slow down product launches in highly regulated markets such as Europe and North America.

What are the key opportunities in the frozen novelty industry?

Growth of Plant-Based and Clean Label Innovation

There is a strong opportunity for manufacturers to expand plant-based frozen novelty offerings. Increasing vegan population and lactose intolerance cases are driving demand for dairy-free alternatives. Companies investing in oat, almond, and coconut-based innovations are expected to capture premium market segments and enhance brand loyalty.

Expansion in Emerging Markets

Rapid urbanization and rising disposable incomes in Asia-Pacific, Latin America, and the Middle East are creating significant growth opportunities. Expansion of modern retail formats and cold chain infrastructure is improving product accessibility, enabling global brands to penetrate untapped markets effectively.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12500.00 Million |

| Market Size in 2026 | USD 13225.00 Million |

| Market Size in 2031 | USD 17531.70 Million |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ice cream bars continue to dominate the global frozen novelty market, maintaining their leading position due to strong brand recognition, deep product penetration across retail shelves, and their highly convenient on-the-go consumption format. Their portability, portion control appeal, and widespread availability across both developed and emerging markets have reinforced their leadership. The segment is further strengthened by continuous flavor innovation, coating enhancements such as chocolate drizzles, nut inclusions, and layered fillings that elevate sensory appeal and consumer engagement. Manufacturers are also leveraging premiumization strategies, introducing artisanal ingredients, organic dairy bases, and exotic flavors to cater to evolving consumer expectations in urban markets.Ice cream sandwiches and frozen cones are emerging as fast-growing premium categories, driven by indulgent consumption behavior and rising willingness among consumers to experiment with texture-rich frozen desserts. These products benefit from innovation in biscuit bases, waffle cones, layered fillings, and hybrid dessert formats that combine multiple taste experiences. Their growth is particularly supported by urban millennials seeking novelty-driven consumption experiences and visually appealing dessert options that perform well on social media platforms.Frozen yogurt novelties are experiencing accelerated expansion, largely driven by increasing health consciousness and growing awareness of probiotic benefits. Consumers are actively shifting toward low-fat, gut-health-oriented alternatives, positioning frozen yogurt as a functional indulgence category. The segment’s growth is reinforced by rising adoption in fitness-focused consumer groups and its strong association with digestive wellness, which continues to drive repeat purchases and premium positioning in retail outlets.Fruit-based frozen novelties are gaining substantial traction as clean-label and natural ingredient trends reshape consumer preferences. This segment’s expansion is supported by the increasing demand for vegan-friendly, dairy-free, and minimally processed frozen desserts. The leading driver for this category is the strong global shift toward plant-based diets and the avoidance of artificial additives, making fruit-based novelties a preferred choice among health-conscious and environmentally aware consumers.

Application Insights

Household consumption remains the dominant application segment in the frozen novelty market, supported by strong retail penetration, increasing availability of diversified product assortments, and the growing culture of at-home snacking. The leading driver for this segment is the shift in consumer behavior toward home-based indulgence experiences, particularly after global lifestyle changes that have reinforced in-home consumption habits. Rising disposable incomes and increased purchasing frequency in family households further strengthen this segment’s dominance.Foodservice applications are witnessing rapid growth as quick service restaurants, cafes, and dessert chains increasingly integrate frozen novelties into their menus. The primary driver of this expansion is the rising demand for experiential dining and customizable dessert offerings that enhance customer engagement. Foodservice providers are actively innovating with frozen dessert-based beverages, layered sundaes, and hybrid offerings to attract younger consumers and increase average order value.Institutional demand, including schools, universities, and corporate cafeterias, is steadily increasing due to structured food programs and rising emphasis on providing diversified snack options. The growth in this segment is driven by large-scale procurement systems and the inclusion of frozen novelties as part of standardized meal offerings. Additionally, nutritional reformulation efforts are enabling wider adoption in institutions focused on balanced dietary programs.Export-driven demand is also expanding significantly as manufacturers scale international distribution networks. The leading driver for this segment is globalization of food preferences combined with improving cold chain logistics, enabling seamless cross-border trade. North American and European producers are increasingly targeting high-growth emerging markets in Asia-Pacific and the Middle East, where demand for branded frozen desserts is rapidly increasing.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the distribution landscape due to their extensive product assortment, strong brand visibility, and ability to support bulk purchasing behavior. The primary driver of this channel’s leadership is consumer preference for one-stop shopping experiences where frozen novelties are readily accessible alongside other grocery essentials. Organized retail expansion in emerging economies further strengthens this segment’s dominance.Convenience stores are experiencing strong growth momentum driven by impulse purchasing behavior and increasing urbanization. Their strategic placement in high-footfall areas such as transit stations and residential neighborhoods makes them a key driver for on-the-go consumption patterns. The segment benefits from quick purchase decisions and frequent repeat buying cycles, especially among younger consumers.Online retail and quick commerce platforms represent the fastest-growing distribution channel in the frozen novelty market. The leading driver of this segment is digital transformation in grocery shopping combined with rapid delivery infrastructure that supports cold chain integrity. Consumers increasingly value convenience, variety, and doorstep delivery, which has significantly accelerated online penetration in urban markets.Foodservice distribution channels are also expanding, supported by partnerships between manufacturers and cafes, dessert chains, and quick service restaurants. The primary growth driver is the rising trend of experiential dining, where frozen novelties are integrated into innovative menu offerings that enhance brand differentiation and customer loyalty.

Consumer Type Insights

Household consumers account for the largest share of demand, driven by consistent retail purchases and family-oriented consumption behavior. The dominant driver in this segment is the integration of frozen novelties into everyday snacking routines, supported by increasing affordability and wide product availability across retail formats.Young consumers represent a key growth segment, strongly influenced by social media trends, visual appeal, and innovative product formats. Their consumption behavior is driven by experiential preferences and a high inclination toward trying new flavors and limited-edition products. This demographic significantly influences product innovation cycles across the industry.Health-conscious consumers are increasingly shifting toward low-calorie, sugar-free, and functional frozen novelties. The main driver for this segment is rising awareness of nutritional content and lifestyle-related dietary choices, leading to increased demand for frozen yogurt and fruit-based alternatives.Premium consumers are driving demand for artisanal and gourmet frozen desserts characterized by high-quality ingredients, unique flavor profiles, and luxury positioning. This segment is primarily driven by rising disposable incomes and growing preference for indulgent yet high-quality food experiences.Institutional buyers contribute stable and predictable demand through bulk procurement for organized food programs. Their growth is driven by structured procurement systems and the inclusion of frozen novelties in standardized dietary offerings across educational and corporate environments.

Age Group Insights

The 18-30 age group is one of the most influential consumer segments, driven by impulse purchasing behavior, digital engagement, and strong responsiveness to innovative product launches. Their consumption is shaped by lifestyle trends, social media influence, and preference for visually appealing frozen novelties that offer novelty and experimentation.The 31-50 age group represents the largest consumption base in the market, supported by higher disposable incomes and stable household purchasing patterns. The key driver for this segment is the balance between indulgence and family-oriented consumption, with frequent purchases driven by both personal and household needs.Older demographics show increasing interest in premium and health-oriented frozen novelties. The primary driver for this segment is the growing focus on wellness, dietary control, and preference for reduced-sugar or functional dessert options that align with healthier aging lifestyles.Children remain a core target segment, particularly for flavored popsicles and ice cream bars. Their consumption is driven by taste preferences, attractive packaging, and strong brand marketing strategies aimed at younger audiences, making them a consistent demand generator across global markets.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Novelty Market Segmentations

By Product Type

- Ice Cream Bars

- Popsicles / Frozen Fruit Sticks

- Ice Cream Sandwiches

- Frozen Cones

- Frozen Yogurt Novelties

- Fruit-Based Frozen Novelties

- Specialty & Indulgent Dairy Novelties

By Ingredient Base

- Dairy-Based Frozen Novelties

- Plant-Based / Non-Dairy Frozen Novelties

- Functional Low-Sugar / High-Protein Novelties

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Quick Commerce

- Foodservice

- Vending & Automated Retail

By Packaging Type

- Single-Serve Packaging

- Multi-Pack Family Packs

- Bulk Foodservice Packs

By End Use

- Household / Retail Consumption

- Foodservice & HoReCa

- Institutional Buyers

Regional Insights

North America

North America accounts for a significant share of the global frozen novelty market, supported by high per-capita consumption, strong brand penetration, and well-established cold chain infrastructure. The leading driver of growth in this region is the mature yet highly innovative dessert culture, where consumers consistently seek premium, functional, and indulgent frozen products. The United States dominates the region due to strong demand for ice cream bars, sandwiches, and protein-enriched frozen desserts, while Canada demonstrates steady expansion supported by increasing health-conscious consumption and demand for organic formulations. The region is also witnessing strong growth in plant-based frozen novelties, driven by rising vegan and lactose-free dietary preferences.

Europe

Europe holds a substantial share of the market, with strong contributions from Germany, the United Kingdom, France, and Italy. The key driver in this region is the strong emphasis on premiumization, sustainability, and clean-label product innovation. Consumers are increasingly prioritizing organic ingredients, reduced sugar content, and environmentally responsible packaging. The region’s growth is also supported by strict food quality regulations that encourage product transparency and innovation. Demand for artisanal frozen desserts and gourmet offerings continues to rise, particularly in urban centers where experiential consumption is highly valued.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, expanding retail infrastructure, and increasing disposable incomes. The primary growth driver is the rising middle-class population combined with changing dietary habits and increased exposure to global food trends. China and India are the largest contributors due to massive population bases and expanding cold chain networks, while Japan and Australia represent mature but stable premium markets. The region is also witnessing strong digital retail penetration, significantly boosting online frozen dessert sales.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico, where increasing urban consumption and retail expansion are driving demand. The key driver in this region is the strong preference for affordable indulgence products such as popsicles and ice cream bars, which are widely accessible across income groups. Growing branded product penetration and expansion of modern retail formats are further supporting market development. Climate conditions also play a significant role in sustaining consistent demand throughout the year.

Middle East & Africa

The Middle East and Africa region is witnessing consistent growth driven by hot climatic conditions, rising tourism activity, and expanding retail infrastructure. The leading driver is the increasing demand for refreshing and indulgent frozen desserts in high-temperature environments, particularly in urban centers. The United Arab Emirates and South Africa are key markets, showing rising demand for premium and imported frozen novelties. Growth is further supported by increasing investments in cold chain logistics and the expansion of modern supermarket networks, enabling better product accessibility across the region.