Frozen Meat And Poultry Market Size

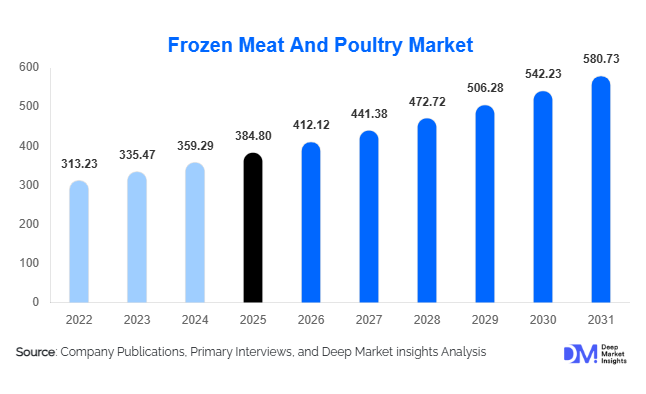

According to Deep Market Insights, the global frozen meat and poultry market size was valued at USD 384.8 billion in 2025 and is projected to grow from USD 412.12 billion in 2026 to reach USD 580.73 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The frozen meat and poultry market growth is primarily driven by rising global protein consumption, increasing demand for convenience foods, rapid expansion of cold-chain logistics infrastructure, and growing penetration of organized retail and foodservice channels worldwide.

Key Market Insights

- Frozen poultry products continue to dominate global consumption, supported by affordability, high protein content, and extensive use in quick-service restaurants and ready-to-cook meal applications.

- Processed frozen meat products are witnessing accelerated demand, driven by changing urban lifestyles, increasing working populations, and growing preference for convenience-oriented food solutions.

- North America dominates the global market, supported by advanced cold-chain infrastructure, high per capita meat consumption, and strong foodservice industry penetration.

- Asia-Pacific remains the fastest-growing region, led by rising disposable incomes, rapid urbanization, expanding organized retail, and increasing adoption of frozen foods in China, India, and Southeast Asia.

- Halal-certified, antibiotic-free, and organic frozen meat products are emerging as high-growth premium categories, reflecting changing consumer preferences toward healthier and ethically sourced protein products.

- Technological advancements in IQF freezing, automated processing systems, AI-enabled cold-chain monitoring, and smart packaging are significantly improving product quality, shelf life, and supply chain efficiency.

What are the latest trends in the frozen meat and poultry market?

Premium and Clean-Label Frozen Meat Products Gaining Popularity

Consumers globally are increasingly demanding premium frozen meat and poultry products that emphasize food safety, transparency, and health-conscious ingredients. Organic poultry, antibiotic-free chicken, hormone-free beef, and halal-certified frozen meat products are witnessing substantial growth across developed and emerging markets. Premiumization trends are particularly strong in North America, Europe, and the Middle East, where consumers are willing to pay higher prices for traceable and ethically sourced products. Manufacturers are introducing clean-label processed meat products with reduced preservatives, natural marinades, and sustainable packaging to strengthen consumer trust and brand loyalty. Demand for premium frozen ready-to-cook meals and gourmet meat offerings is also expanding rapidly through online grocery channels and specialty retail stores.

Technology-Driven Cold Chain and Processing Modernization

The frozen meat and poultry industry is increasingly adopting advanced freezing and supply chain technologies to improve operational efficiency and maintain product quality. Individually Quick Frozen (IQF) technology, cryogenic freezing systems, robotic meat processing lines, and IoT-enabled refrigerated transportation are becoming standard across large-scale processing facilities. AI-powered inventory forecasting and temperature-monitoring systems are reducing food wastage and improving supply chain transparency. Blockchain-based traceability systems are also gaining traction, enabling consumers and regulators to track product origin, processing conditions, and logistics movement. Online grocery platforms are integrating smart cold-chain delivery networks to support rapid expansion of frozen meat e-commerce sales globally.

What are the key drivers in the frozen meat and poultry market?

Growing Demand for Convenience Foods

The increasing pace of urban lifestyles and rising participation of working populations are major factors driving frozen meat and poultry consumption globally. Consumers increasingly prefer ready-to-cook and ready-to-eat meat products that minimize meal preparation time while maintaining nutritional value and longer shelf life. Frozen chicken nuggets, patties, sausages, marinated meat products, and processed poultry items have become highly popular among urban households. Growth in dual-income families and rising freezer ownership are further supporting retail consumption of frozen protein products. Convenience-oriented food consumption patterns are particularly strong in North America, Europe, and rapidly urbanizing Asian economies.

Expansion of Quick-Service Restaurants and Foodservice Chains

The rapid global expansion of quick-service restaurants (QSRs), cloud kitchens, institutional catering, and hospitality industries is significantly boosting demand for frozen poultry and processed meat products. Frozen meat products provide standardized quality, inventory stability, and longer storage life, making them essential inputs for foodservice operations. Major fast-food chains increasingly depend on centralized frozen meat supply systems to ensure operational consistency across international markets. Emerging economies are witnessing rising consumption of western-style fast food, further accelerating frozen chicken and processed meat demand across Asia Pacific, Latin America, and the Middle East.

What are the restraints for the global market?

Volatility in Livestock and Feed Prices

The frozen meat and poultry market remains highly sensitive to fluctuations in feed grain prices, livestock availability, and disease outbreaks. Corn and soybean meal prices directly influence poultry and meat production costs, creating margin pressure for processors and exporters. Outbreaks such as avian influenza and swine fever can disrupt global supply chains, reduce export volumes, and create temporary shortages. Energy price fluctuations also impact cold storage and refrigerated transportation costs, increasing operational expenses across the value chain.

Health Concerns and Regulatory Compliance Challenges

Growing consumer preference for fresh and minimally processed foods remains a challenge for frozen meat manufacturers in some developed regions. Certain consumers continue to associate frozen processed meat products with preservatives, sodium content, and lower nutritional quality. In addition, food safety regulations related to labeling, traceability, storage temperatures, and export certifications continue to tighten globally. Compliance with sustainability regulations, animal welfare standards, and environmentally friendly packaging requirements is increasing operational complexity and capital expenditure requirements for industry participants.

What are the key opportunities in the frozen meat and poultry industry?

Expansion of Cold-Chain Infrastructure in Emerging Economies

Rapid investment in refrigerated logistics and cold storage infrastructure across emerging markets presents a major opportunity for frozen meat and poultry manufacturers. Countries such as India, Indonesia, Vietnam, Brazil, and South Africa are investing heavily in food preservation systems to reduce post-harvest losses and improve food security. Government-supported cold-chain development initiatives are enabling wider penetration of frozen products into tier-2 and tier-3 cities. This infrastructure modernization is expected to significantly increase consumption of frozen meat products across previously underserved regions.

Growth of Online Grocery and Direct-to-Consumer Platforms

The rapid expansion of online grocery platforms and direct-to-consumer frozen food delivery services is transforming frozen meat distribution globally. E-commerce platforms are improving product accessibility through advanced last-mile refrigerated delivery systems and subscription-based meal services. Consumers increasingly prefer doorstep delivery of frozen poultry and processed meat products due to convenience and competitive pricing. Partnerships between frozen food manufacturers and digital retail platforms are creating opportunities for product innovation, premium branding, and consumer personalization. AI-powered recommendation systems and data-driven consumer insights are further supporting growth in online frozen meat sales.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 384.80 |

| Market Size in 2026 | USD 412.12 |

| Market Size in 2031 | USD 580.73 |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Frozen chicken continues to dominate the global frozen meat and poultry market, maintaining its position as the most widely consumed and commercially viable protein category. Its leadership is primarily driven by a combination of affordability, widespread cultural acceptance, ease of portioning, and adaptability across multiple culinary formats. The rising global population, coupled with increasing protein consumption in developing economies, has further reinforced frozen chicken’s dominance. In addition, the expansion of quick-service restaurants and institutional foodservice chains has significantly increased bulk procurement of frozen chicken products due to their consistency, long shelf life, and operational efficiency in large-scale kitchens.Processed chicken products such as nuggets, wings, patties, tenders, and marinated cuts represent one of the fastest-growing subsegments within the frozen poultry category. The key growth driver for processed chicken is the accelerating demand for convenience-oriented, ready-to-cook, and ready-to-eat meal solutions, particularly among urban working populations and younger consumers. In North America and Asia-Pacific, lifestyle changes, increasing disposable incomes, and rising dual-income households are contributing to strong demand for pre-seasoned and value-added poultry products. Foodservice expansion and aggressive menu innovation by global restaurant chains further reinforce this trend.Processed frozen meat products, including sausages, kebabs, burgers, and meatballs, are witnessing accelerated global growth. The key driver for this segment is the increasing penetration of ready-to-eat and ready-to-heat food culture, especially in fast-paced urban environments. Growth is also strongly supported by advancements in food processing technologies that enhance taste, texture, and shelf stability, making processed frozen meats more appealing to both retail and institutional buyers. Rising demand for standardized food quality in quick-service restaurants further strengthens this segment’s market position.

Application Insights

The ready-to-cook segment represents the largest application category in the frozen meat and poultry market, primarily driven by the growing demand for convenience foods among urban consumers. The increasing number of working professionals, shrinking cooking time, and expansion of nuclear households are key structural drivers behind this segment’s dominance. Ready-to-cook frozen meat products offer flexibility, time efficiency, and reduced preparation complexity, making them a preferred choice in both developed and emerging markets.Frozen meat ingredients used in processed food manufacturing form a critical component of the global food supply chain. These ingredients are widely utilized in the production of packaged meals, frozen pizzas, sandwiches, snacks, and instant food products. The primary driver of growth in this segment is the expansion of the packaged food industry, supported by increasing urbanization and rising demand for shelf-stable protein-based food products. Food manufacturers rely heavily on frozen meat due to its consistency, cost efficiency, and extended usability in production cycles.Emerging application areas such as high-protein dietary meals, fitness-oriented frozen foods, and ethnic cuisine-based frozen products are gaining traction globally. The primary driver for these segments is the rising awareness of nutrition, protein-rich diets, and global culinary diversification. Products such as frozen kebabs, dumplings, and marinated specialty meats are increasingly popular in international retail chains, driven by multicultural consumption patterns and expanding global food tourism influences.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels for frozen meat and poultry products globally. Their leadership is driven by extensive cold storage infrastructure, wide product assortment, and strong consumer trust in organized retail environments. These outlets provide consumers with the ability to compare multiple brands and product types, which strengthens their role as primary purchasing destinations for frozen protein products. The expansion of organized retail in emerging economies further reinforces this dominance.Online retail and e-commerce platforms represent the fastest-growing distribution channel in the frozen meat market. The primary driver of growth is the rapid adoption of digital grocery shopping, supported by improvements in cold-chain logistics and last-mile delivery systems. Consumers increasingly prefer online platforms due to convenience, wider product selection, and home delivery services. Subscription-based meat delivery models and mobile grocery applications are further accelerating digital transformation in this segment.Foodservice distributors remain essential for supplying bulk frozen meat products to restaurants, hotels, institutional catering services, and airline catering operators. The key driver in this segment is the centralized procurement systems adopted by large foodservice organizations, which require consistent quality, bulk supply efficiency, and strict adherence to food safety standards. The expansion of global hospitality and tourism industries further strengthens demand through this channel.Direct-to-consumer delivery models and app-based frozen meat platforms are emerging as innovative distribution channels. Their growth is driven by changing consumer behavior, increasing digital penetration, and demand for personalized food shopping experiences. These platforms are reshaping traditional supply chains by offering curated product selections and flexible delivery schedules.

End-Use Insights

Household consumption remains the largest end-use segment in the frozen meat and poultry market. The primary drivers include increasing freezer ownership, rising urbanization, and shifting dietary habits toward protein-rich and convenience-oriented foods. Modern consumers increasingly rely on frozen meat products to manage time constraints while maintaining dietary diversity, making this segment a foundational pillar of market demand.Quick-service restaurants represent the fastest-growing end-use category, driven by global expansion of fast-food chains and increasing consumer preference for affordable dining options. The scalability, consistency, and operational efficiency offered by frozen meat products make them indispensable to QSR operations. The rise of food delivery platforms further amplifies demand in this segment.Institutional catering services, including hospitals, educational institutions, military food supply systems, and corporate cafeterias, contribute significantly to stable and predictable demand. The key driver is centralized procurement systems that prioritize cost efficiency, long shelf life, and nutritional consistency. These institutions rely heavily on frozen meat to ensure large-scale meal preparation with minimal waste.Cloud kitchens and online food delivery platforms are emerging as high-growth end-use segments. Their expansion is driven by the rise of digital food ordering ecosystems and consumer demand for quick, restaurant-quality meals at home. These platforms rely heavily on frozen meat for menu standardization and operational efficiency in high-volume delivery environments.

Technology Insights

Individually Quick Frozen (IQF) technology remains the dominant freezing method in the industry due to its ability to preserve product integrity, texture, and nutritional value. The primary driver for IQF adoption is its superior ability to prevent ice crystal formation, ensuring high-quality frozen meat products that closely resemble fresh alternatives upon thawing.Cryogenic freezing systems are increasingly utilized for premium meat products requiring ultra-fast freezing processes. The key driver for this technology is its ability to maintain cellular structure and reduce moisture loss, thereby enhancing product quality for high-value export markets and gourmet food segments.Automation in meat processing, including robotic cutting systems, automated packaging lines, and AI-powered quality inspection technologies, is transforming operational efficiency. The main driver for adoption is the need to reduce labor dependency, improve precision, and enhance throughput in large-scale processing facilities.Smart cold storage systems integrated with IoT sensors are becoming increasingly important for maintaining optimal temperature conditions throughout the supply chain. The key driver is the growing emphasis on reducing spoilage, improving traceability, and ensuring compliance with international food safety regulations.Blockchain-based traceability solutions are emerging as critical technologies for enhancing transparency in meat supply chains. The primary driver is increasing regulatory pressure and consumer demand for traceable, ethically sourced, and safe food products, particularly in export-driven markets.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Meat And Poultry Market Segmentations

By Product Type

- Frozen Beef

- Frozen Pork

- Frozen Chicken

- Frozen Turkey

- Frozen Lamb & Mutton

- Frozen Processed Meat Products

- Frozen Processed Poultry Products

By Processing Type

- Raw Frozen

- Pre-Cooked Frozen

- Marinated Frozen

- Breaded & Coated Frozen

- Processed Frozen Meat & Poultry

By Freezing Technology

- Individually Quick Frozen

- Blast Freezing

- Cryogenic Freezing

- Plate Freezing

- Conventional Freezing

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Meat Stores

- Online Retail & E-Commerce

- Foodservice Distributors

- Wholesale Clubs

By End Use

- Household/Retail Consumption

- Quick Service Restaurants

- Hotels & Restaurants

- Institutional Catering

- Food Processing Industry

- Airlines & Rail Catering

Regional Insights

North America

North America accounts for approximately 31% of the global frozen meat and poultry market and remains one of the most mature and technologically advanced regions. The United States leads regional demand due to high per capita meat consumption, strong QSR penetration, and well-established cold-chain logistics infrastructure. The primary growth driver in this region is the increasing consumer preference for convenience foods and protein-rich diets. Canada exhibits steady demand supported by processed food consumption and retail expansion, while Mexico is witnessing rapid growth driven by urbanization, rising incomes, and increasing adoption of western-style foodservice culture. Technological innovation and strong regulatory frameworks further reinforce regional market stability.

Europe

Europe holds nearly 24% of the global market, with strong demand across Germany, the United Kingdom, France, and Italy. The key driver of regional growth is the rising consumer preference for premium, organic, and sustainably sourced frozen meat products. European consumers are increasingly focused on clean-label food, antibiotic-free poultry, and environmentally responsible production practices. Additionally, Europe serves as a major export hub, particularly through processing centers in Poland and the Netherlands, supported by advanced logistics and compliance standards. The growth of frozen convenience foods and increasing demand for ethically produced protein continue to shape regional dynamics.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for approximately 29% of global demand. The primary driver is rapid urbanization combined with rising disposable incomes and expanding middle-class populations. China leads regional consumption due to increasing imports of frozen beef and poultry and expansion of cold-chain infrastructure. India is emerging as a high-growth market driven by retail modernization, e-commerce expansion, and increasing demand for processed poultry products. Japan and South Korea maintain strong demand for premium frozen ready meals, while Southeast Asia benefits from tourism growth, changing dietary habits, and rapid expansion of international foodservice chains.

Latin America

Latin America is a critical production and export region, with Brazil and Argentina serving as global leaders in poultry and beef exports. The key growth driver is the region’s competitive livestock production costs and strong export-oriented meat processing infrastructure. Domestic demand is also rising due to urbanization and growing consumption of processed and packaged foods. Chile is increasingly importing premium frozen meat products through expanding retail networks, reflecting changing consumer preferences toward higher-quality protein sources.

Middle East & Africa

The Middle East and Africa region is experiencing strong growth driven by rising demand for halal-certified frozen meat products and increasing dependence on imports. GCC countries such as Saudi Arabia, the UAE, and Qatar are major importers due to limited domestic production capacity. The key growth drivers include tourism expansion, rapid hospitality sector development, and rising foodservice demand. In Africa, countries such as South Africa and Egypt are witnessing growth supported by urbanization, expanding retail infrastructure, and improving cold-chain logistics. Investments in food security programs and refrigerated supply chains are expected to further enhance long-term regional growth potential.

Key Players in the Frozen Meat And Poultry Market

- Tyson Foods

- JBS S.A.

- BRF S.A.

- WH Group

- Cargill Incorporated

- NH Foods Ltd.

- Marfrig Global Foods

- Hormel Foods Corporation

- OSI Group

- Perdue Farms

- Charoen Pokphand Foods

- Danish Crown

- Pilgrim’s Pride Corporation

- Minerva Foods

- Mowi ASA