Frozen Lemon Concentrate Market Size

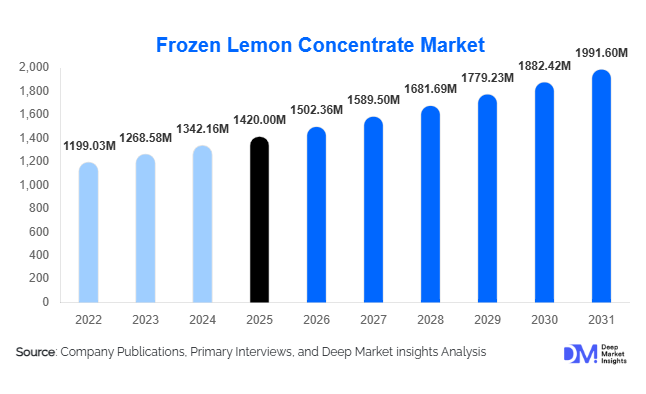

According to Deep Market Insights,the global frozen lemon concentrate market size was valued at USD 1,420 million in 2026 and is projected to grow from USD 1502.36 million in 2026 to reach USD 1991.60 million by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The market growth is primarily driven by rising global demand for natural and convenient food and beverage ingredients, increasing consumption of lemon-based beverages, and the growing preference for health-oriented functional products containing natural antioxidants and vitamin C.

Key Market Insights

- Double strength frozen lemon concentrate (DSFC) dominates the product type segment, owing to its concentrated form that is cost-effective for industrial food and beverage applications.

- Beverages remain the largest application segment, led by the increasing global consumption of lemonades, soft drinks, cocktails, and functional beverages.

- North America holds a leading share of the market, driven by strong beverage and food processing demand in the U.S. and Canada.

- Asia-Pacific is the fastest-growing region, fueled by rising middle-class incomes, urbanization, and expanding foodservice industries in China, India, and Japan.

- Online retail and e-commerce channels are emerging rapidly, providing direct-to-consumer access and expanding market reach for both organic and conventional frozen lemon concentrates.

- Technological innovations, such as advanced freezing techniques and cold-chain enhancements, are improving product quality, shelf life, and supply chain efficiency globally.

What are the latest trends in the frozen lemon concentrate market?

Health and Functional Beverage Integration

Frozen lemon concentrate is increasingly incorporated into functional beverages, immunity-boosting drinks, and organic lemonade formulations. Companies are leveraging the natural vitamin C content, antioxidants, and clean-label appeal of lemon concentrate to target health-conscious consumers. Products are being fortified or blended with other natural extracts to appeal to premium and wellness-oriented segments. The trend toward natural ingredients in beverages has led manufacturers to prioritize high-quality, certified organic frozen lemon concentrates, creating differentiation and commanding higher prices in the market.

Organic and Single-Strength Concentrate Growth

Demand for organic frozen lemon concentrate and single-strength variants is rising due to increasing awareness of sustainable agriculture and health benefits. These variants allow producers to cater to premium, eco-conscious consumers, particularly in North America and Europe. Organic certification and traceability of lemon origin have become critical for market competitiveness, with manufacturers investing in quality control, sustainable farming partnerships, and transparent labeling to gain consumer trust.

What are the key drivers in the frozen lemon concentrate market?

Rising Beverage Industry Demand

The beverage industry remains the primary growth driver, with frozen lemon concentrate used extensively in soft drinks, lemonades, cocktails, and functional beverages. In 2025, the beverage application accounted for over 50% of total market demand. Increasing urbanization, café culture, and premium ready-to-drink beverages are propelling growth, particularly in North America and Europe.

Health-Conscious Consumer Trends

Consumers are increasingly opting for natural, vitamin-rich, and preservative-free ingredients, favoring lemon concentrate over synthetic flavoring agents. The growing popularity of organic and immune-boosting beverages, as well as natural food formulations in bakery, dairy, and confectionery, is further enhancing market demand.

Long Shelf Life and Cost Efficiency

Frozen lemon concentrate offers extended shelf life, reducing spoilage and enabling bulk storage and transportation. Its concentrated form allows manufacturers to lower logistics and raw material costs, particularly for large-scale beverage and food processing operations. These advantages make it a preferred ingredient for industrial and commercial applications worldwide.

What are the restraints for the global market?

Seasonal Supply and Raw Material Fluctuations

Frozen lemon concentrate production depends on seasonal lemon harvests. Adverse weather events, crop diseases, or inconsistent harvests can lead to raw material shortages, impacting supply stability and driving price volatility in the market.

High Cold-Chain Infrastructure Costs

Investment in freezing, storage, and cold-chain logistics is capital-intensive. Small and medium-sized manufacturers face barriers entering the market due to high initial costs, limiting production capacity and geographic expansion. Maintaining optimal storage and transportation temperatures is critical to preserve quality, further adding to operational costs.

What are the key opportunities in the frozen lemon concentrate market?

Emerging Markets Expansion

Asia-Pacific and Latin America offer substantial growth opportunities. Rising disposable incomes, urbanization, and the expansion of cafes, juice bars, and beverage manufacturing industries in China, India, and Brazil are driving demand. Manufacturers can benefit from local production facilities or strategic partnerships to tap into these rapidly growing markets.

Functional and Organic Product Development

Health-focused and organic frozen lemon concentrates represent a premium segment with higher margins. Companies can innovate by blending lemon concentrate with vitamins, herbal extracts, or other natural ingredients to create value-added products for health-conscious consumers and the growing functional beverage segment.

Technological Integration and Cold-Chain Optimization

Adopting advanced freezing, processing, and storage technologies improves product consistency, reduces waste, and extends shelf life. Automation and cold-chain expansions, supported by initiatives like India’s “Make in India” and China’s “Made in China 2025,” offer opportunities for operational efficiency, supply reliability, and market expansion.

Product Type Insights

Double strength frozen lemon concentrate (DSFC) dominates the global market, accounting for approximately 48% of the market share in 2025. Its concentrated form allows industrial users to minimize transportation and storage costs while maintaining consistent flavor and quality, making it the preferred choice for large-scale beverage and food processing applications. Single strength and organic lemon concentrates are witnessing steady growth, fueled by increasing consumer awareness of health and wellness, a preference for natural ingredients, and the rising demand for premium products, particularly across Europe and North America. The organic segment is further supported by stringent regulatory frameworks and sustainability-driven consumption trends, which encourage the adoption of certified organic concentrates.

Application Insights

The beverage segment remains the leading application globally, representing over 50% of market consumption in 2025. This is driven by the popularity of lemonades, soft drinks, and functional beverages, which leverage the natural flavor and health benefits of lemon concentrates. The food processing sector, encompassing bakery, confectionery, and dairy products, is experiencing a robust CAGR of 5.5%–6%, driven by the rising use of natural flavoring agents and consumer preference for clean-label products. Industrial applications in nutraceuticals and cosmetics, although smaller in volume, show significant growth potential as the demand for natural ingredients in personal care and health supplements continues to rise, supported by trends in preventive healthcare and wellness.

Distribution Channel Insights

Supermarkets and hypermarkets lead the distribution landscape, accounting for approximately 40% of retail sales due to their extensive reach, brand visibility, and ability to provide a variety of product formats. Online retail is the fastest-growing channel, offering direct-to-consumer access, personalized shopping experiences, and the ability to target niche health-conscious segments. Foodservice and HoReCa (Hotels, Restaurants, and Cafés) channels continue to be essential for bulk purchases and commercial applications, particularly in beverage preparation and processed food production. The growth in e-commerce and B2B distribution platforms is expected to further accelerate market penetration globally.

End-Use Insights

Beverages dominate end-use consumption, accounting for over 50% of the total market. The food processing sector is emerging rapidly as a key driver, supported by the rising adoption of natural and clean-label ingredients in bakery, confectionery, and dairy applications. Industrial applications in cosmetics and nutraceuticals present new avenues for growth, fueled by the increasing demand for functional and health-oriented products. Export-driven demand is particularly significant in regions such as the Middle East, Eastern Europe, and Africa, where local lemon production is limited, creating opportunities for imported frozen lemon concentrates to meet the growing consumption requirements of beverages and processed foods.

| By Product Type | By Application | By Form | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America is the largest market, with the U.S. and Canada collectively holding 32% of the global share in 2025. Growth is primarily driven by high per capita beverage consumption, the presence of advanced food processing industries, and increasing consumer preference for premium and organic products. Sustainability initiatives, regulatory standards, and health-conscious consumption patterns encourage the adoption of certified organic lemon concentrates. The strong industrial base and well-established distribution networks, including supermarkets and online retail, further support the region’s dominance.

Europe

Europe accounted for 28% of the global market in 2025, with Germany, France, and the U.K. leading adoption. Market growth is fueled by health-conscious consumers, rising demand for functional beverages, and a robust foodservice sector that drives commercial usage. Germany, in particular, is the fastest-growing European country due to the increasing adoption of organic and functional concentrates, supported by government initiatives promoting natural and sustainable food products. Premium product awareness, coupled with strong retail infrastructure and e-commerce adoption, further enhances regional growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, led by China, India, Japan, and Australia. Expanding middle-class populations, rapid urbanization, and evolving beverage and café culture contribute significantly to the market’s growth. Rising demand for processed foods and functional beverages, combined with the proliferation of online retail platforms and group-oriented beverage production, is accelerating adoption. Government initiatives supporting food safety, quality standards, and organic production also serve as key growth drivers, particularly in developed markets like Japan and Australia.

Latin America

Brazil, Mexico, and Argentina dominate the Latin American market, driven by increasing consumption in beverage and food processing applications. Brazil is emerging rapidly as a key growth market due to rising domestic demand, expanding industrial production, and growing export potential to North America and Europe. Urbanization, rising disposable incomes, and a growing preference for natural and functional beverages support the adoption of both single and double strength lemon concentrates. Additionally, investments in cold-chain logistics enhance market accessibility across the region.

Middle East & Africa

Africa benefits from key lemon-producing regions, enabling local frozen concentrate production, while the Middle East, led by the UAE and Saudi Arabia, serves as a major import market. Market growth in these regions is driven by high-income populations, increasing consumption of beverages, and rising demand from food processing industries. Intra-African trade, investment in cold storage infrastructure, and the growing hospitality and HoReCa sectors further contribute to regional expansion. The preference for premium and organic products, particularly in high-income urban centers, is creating new opportunities for market participants.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Frozen Lemon Concentrate Market

- Citrosuco S.A.

- Sumifru Co., Ltd.

- Döhler Group

- Florida’s Natural Growers

- Lemonaid Beverages GmbH

- Louis Dreyfus Company

- TreeTop Inc.

- Greenyard NV

- Ocean Spray Cranberries, Inc.

- True Citrus LLC

- Bravura Foods Ltd

- Agrana Fruit

- Limonit S.A.

- RFM Corporation

- Runa LLC