Frozen Fruits and Vegetables Market Size

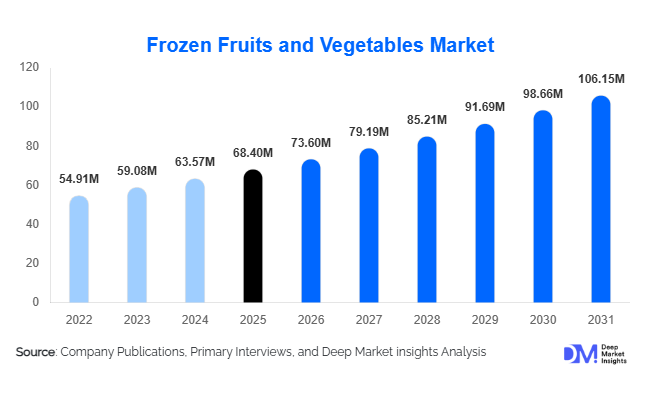

According to Deep Market Insights, the global frozen fruits and vegetables market size was valued at USD 68.4 billion in 2025 and is projected to grow from USD 73.60 billion in 2026 to reach USD 106.15 billion by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for convenient and long-shelf-life food products, rising urbanization, and expanding cold chain infrastructure globally. Consumers are increasingly shifting toward frozen produce due to its ability to retain nutritional value while offering year-round availability. Additionally, the growth of quick-service restaurants (QSRs), ready-to-cook meal solutions, and smoothie-based beverages is significantly boosting demand. Advancements in freezing technologies such as Individual Quick Freezing (IQF) are further enhancing product quality, making frozen fruits and vegetables a preferred alternative to fresh produce across both developed and emerging markets.

Key Market Insights

- Frozen vegetables dominate the market, accounting for over 60% share due to their extensive use in daily cooking and foodservice applications.

- IQF technology leads freezing methods, ensuring superior quality, texture, and nutrient retention.

- Retail channels remain dominant, driven by supermarket expansion and rapid growth of online grocery platforms.

- North America and Europe collectively hold over 55% market share, supported by mature cold chain infrastructure.

- Asia-Pacific is the fastest-growing region, driven by urbanization and rising disposable incomes.

- Flexible packaging is gaining traction, offering cost efficiency and improved storage convenience.

What are the latest trends in the frozen fruits and vegetables market?

Rising Demand for Clean-Label and Organic Frozen Products

Consumers are increasingly prioritizing clean-label and organic food options, which is significantly influencing the frozen fruits and vegetables market. Manufacturers are responding by offering preservative-free, non-GMO, and organically sourced frozen produce. This trend is particularly strong in developed markets where health awareness is high. Retailers are also expanding private-label organic frozen offerings, making them more accessible to mainstream consumers. The shift toward transparency in sourcing and processing is encouraging companies to adopt sustainable farming practices and eco-friendly packaging solutions.

Expansion of Ready-to-Cook and Value-Added Products

The growing demand for convenience foods is driving innovation in ready-to-cook frozen meal kits and mixed vegetable blends. Consumers are increasingly seeking time-saving solutions that require minimal preparation without compromising on nutrition. As a result, manufacturers are introducing pre-seasoned vegetables, smoothie-ready fruit mixes, and meal-specific blends. This trend is particularly strong among urban households and working professionals. Foodservice operators are also relying heavily on pre-processed frozen ingredients to ensure consistency and reduce preparation time.

What are the key drivers in the frozen fruits and vegetables market?

Growing Demand for Convenience Foods

Busy lifestyles and increasing urbanization are driving consumers toward convenient food options. Frozen fruits and vegetables offer ease of storage, minimal preparation time, and consistent quality, making them highly attractive for modern households. The expansion of online grocery platforms and organized retail is further enhancing product accessibility, contributing significantly to market growth.

Reduction in Food Wastage

Frozen produce plays a crucial role in minimizing food wastage due to its extended shelf life. Governments and organizations promoting sustainable food consumption are encouraging the adoption of frozen foods as a viable solution to reduce post-harvest losses. This factor is particularly important in regions with inadequate fresh produce storage infrastructure.

What are the restraints for the global market?

Dependence on Cold Chain Infrastructure

The frozen fruits and vegetables market heavily relies on efficient cold storage and transportation systems. In regions with underdeveloped infrastructure, maintaining product quality becomes challenging, leading to higher operational costs and limited market penetration.

Consumer Preference for Fresh Produce

Despite technological advancements, a segment of consumers still perceives fresh produce as superior in taste and nutrition. This perception can hinder the adoption of frozen products, particularly in traditional and rural markets where fresh produce is readily available.

What are the key opportunities in the frozen fruits and vegetables industry?

Expansion in Emerging Markets

Emerging economies in Asia, Africa, and Latin America present significant growth opportunities due to increasing investments in cold chain infrastructure and food processing industries. Rising disposable incomes and changing dietary habits are encouraging consumers to adopt frozen food products, creating a strong demand base for market players.

Integration of Advanced Freezing Technologies

Technological advancements such as cryogenic freezing and improved IQF methods are enabling manufacturers to enhance product quality and extend shelf life. These innovations allow companies to differentiate their offerings and enter premium market segments, catering to health-conscious and quality-focused consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.4 Million |

| Market Size in 2026 | USD 73.60 Million |

| Market Size in 2031 | USD 106.15 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The frozen fruits and vegetables market continues to be strongly anchored by the dominance of frozen vegetables, which account for approximately 62% of the total market share in 2025. This leadership position is not incidental but rather reflects deeply ingrained consumption habits across both developed and emerging economies. Frozen vegetables such as peas, corn, broccoli, carrots, spinach, and mixed vegetable blends are essential components of everyday cooking, forming the backbone of numerous traditional and modern cuisines. Their extended shelf life, minimal preparation requirements, and ability to retain nutritional value make them particularly appealing to time-constrained consumers. The leading segment driver for frozen vegetables lies in their cost efficiency, year-round availability, and adaptability across multiple culinary applications, ranging from home-cooked meals to large-scale foodservice operations.On the other hand, frozen fruits represent a smaller yet rapidly expanding segment within the market. Their growth trajectory is being fueled by evolving dietary preferences, particularly the increasing consumption of smoothies, desserts, and functional beverages. Fruits such as berries, mangoes, pineapples, and exotic blends are gaining popularity due to their versatility and health benefits. The leading segment driver for frozen fruits is the rising demand for health-oriented, ready-to-use ingredients in beverages and plant-based food applications. As consumers become more health-conscious, frozen fruits are being perceived as a convenient way to access seasonal fruits throughout the year without compromising on nutritional value.The expansion of vegan and plant-based diets is also playing a critical role in driving demand for both frozen fruits and vegetables. Consumers are increasingly incorporating plant-based ingredients into their daily meals, boosting the consumption of frozen produce as a reliable and accessible source of vitamins, minerals, and dietary fiber. This trend is particularly prominent in urban markets, where lifestyle changes and exposure to global food trends are reshaping consumption patterns. Overall, the product type segment is witnessing sustained growth, supported by innovation, convenience, and shifting consumer preferences toward healthier and more sustainable food choices.

Application Insights

The application landscape of the frozen fruits and vegetables market is diverse, with the household segment accounting for nearly 48% of the total market share. This dominance is primarily driven by the increasing reliance on convenient and time-saving food solutions among consumers. The leading segment driver for household applications is the growing demand for easy-to-prepare meals that align with busy lifestyles while maintaining nutritional value. Frozen produce enables consumers to prepare meals quickly without the need for extensive cleaning, cutting, or preparation, making it an ideal choice for modern households.Furthermore, the growing trend of online food delivery and takeaway services is amplifying demand within the foodservice segment. Restaurants and cloud kitchens rely heavily on frozen ingredients to streamline operations and meet high-volume demand without compromising quality. The ability to store and use ingredients as needed also reduces wastage and improves cost efficiency, making frozen produce an integral component of modern foodservice operations.The food processing industry also constitutes a significant application area, utilizing frozen fruits and vegetables in the production of ready meals, soups, sauces, and packaged snacks. The leading segment driver here is the increasing demand for processed and convenience foods that require high-quality, consistent raw materials. Frozen produce ensures that manufacturers can maintain product quality and meet stringent food safety standards while scaling production efficiently.Additionally, the beverage industry is emerging as a promising application segment, particularly for frozen fruits used in smoothies, juices, and functional beverages. The rising popularity of health drinks and natural ingredients is driving the adoption of frozen fruits in this sector. Beverage manufacturers are leveraging frozen fruits to create innovative products that cater to health-conscious consumers seeking nutritious and flavorful options.

Distribution Channel Insights

The distribution landscape of the frozen fruits and vegetables market is dominated by retail channels, which account for approximately 55% of the total market share. The leading segment driver for retail distribution is the expansion of organized retail infrastructure combined with the growing penetration of e-commerce platforms. Supermarkets, hypermarkets, and online grocery stores offer a wide variety of frozen products, enabling consumers to access diverse options under one roof or through convenient digital platforms.Retail channels benefit from strong merchandising strategies, promotional campaigns, and attractive pricing, which encourage consumer purchases. The increasing availability of private-label brands and premium product lines is further enhancing the competitiveness of retail channels. Online grocery platforms, in particular, are experiencing rapid growth, driven by changing consumer shopping behaviors and the convenience of home delivery. The integration of cold chain logistics in e-commerce has significantly improved the reliability of frozen product delivery, boosting consumer confidence in online purchases.Foodservice distribution channels are also witnessing steady growth, supported by increasing demand from restaurants, hotels, and catering services. The leading segment driver in this channel is the rising need for bulk procurement and efficient supply chain management in the foodservice industry. Distributors play a crucial role in ensuring timely delivery of frozen products to foodservice operators, enabling them to maintain consistent operations and meet customer expectations.Industrial and B2B processing channels are equally important, as they supply raw materials to food manufacturers. The leading segment driver for this channel is the growing demand for high-quality, standardized ingredients in large-scale food production. Frozen fruits and vegetables provide manufacturers with the consistency and reliability required for mass production, supporting the growth of the processed food industry. These channels are characterized by long-term contracts, bulk transactions, and stringent quality standards, ensuring a stable supply chain for industrial applications.

End-Use Insights

The end-use segment of the frozen fruits and vegetables market is led by the household sector, which remains the largest consumer base. The leading segment driver for household end-use is the increasing urbanization and shift toward convenient, ready-to-cook food options. As urban populations grow and lifestyles become more fast-paced, consumers are prioritizing convenience without compromising on nutrition. Frozen produce offers an ideal solution, enabling households to prepare meals quickly while maintaining a balanced diet.The foodservice sector is the fastest-growing end-use segment, driven by the rising demand for ready-to-eat and quick-service meals. The leading segment driver here is the expansion of the global foodservice industry and the increasing preference for dining out and food delivery services. Frozen fruits and vegetables play a critical role in supporting foodservice operations by providing consistent quality, reducing preparation time, and enabling efficient inventory management.Export-driven demand is another significant component of the end-use landscape, particularly in countries with strong agricultural production capabilities. The leading segment driver for export demand is the ability of frozen products to facilitate long-distance trade while preserving quality and reducing post-harvest losses. Frozen fruits and vegetables enable producers to access international markets, contributing to global trade and economic growth.Emerging applications in the beverage industry and plant-based food sector are further expanding the end-use landscape. The growing popularity of plant-based diets and functional beverages is driving demand for frozen fruits and vegetables as key ingredients. These trends are creating new opportunities for market players to innovate and diversify their product offerings, catering to evolving consumer preferences.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Fruits and Vegetables Market Segmentations

By Product Type

- Frozen Fruits

- Frozen Vegetables

By Freezing Technology

- Individual Quick Freezing

- Blast Freezing

- Cryogenic Freezing

By Form

- Whole

- Cut/Sliced

- Puree

- Ready-to-Cook Mixes

By Distribution Channel

- Retail

- Foodservice

- Industrial/B2B Processing

By End-Use Industry

- Household Consumption

- Food Processing Industry

- Foodservice Industry

- Beverage Industry

Regional Insights

North America

North America holds approximately 32% of the global market share, with the United States leading the region. The market is characterized by high consumption of frozen foods, advanced cold chain infrastructure, and well-established retail networks. The regional growth is primarily driven by the strong consumer preference for convenience foods, high disposable incomes, and widespread adoption of modern retail formats. Additionally, the presence of leading food processing companies and continuous product innovation are contributing to market expansion.The increasing demand for healthy and organic frozen products is also shaping the market in North America. Consumers are becoming more health-conscious, leading to a shift toward clean-label and minimally processed foods. The growth of online grocery platforms and home delivery services is further enhancing accessibility, making frozen fruits and vegetables a staple in many households. Furthermore, technological advancements in freezing and packaging are improving product quality, reinforcing consumer trust and driving sustained growth in the region.

Europe

Europe accounts for around 28% of the global market, with countries such as Germany, France, and the United Kingdom leading demand. The region benefits from a well-established food processing industry and a strong emphasis on sustainability and food quality standards. The regional growth is driven by the increasing demand for sustainable food solutions, stringent food safety regulations, and high consumer awareness regarding nutrition and quality.European consumers are particularly inclined toward environmentally friendly products, prompting manufacturers to adopt sustainable sourcing and packaging practices. The rising popularity of plant-based diets is also contributing to the growth of frozen fruits and vegetables in the region. Additionally, the expansion of private-label brands and premium product offerings is enhancing market competitiveness. The integration of advanced cold chain logistics and efficient distribution networks ensures the availability of high-quality frozen products across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the global frozen fruits and vegetables market, expanding at a CAGR of over 9%. Major contributors include China and India, where rapid urbanization, rising disposable incomes, and changing dietary habits are driving demand. The regional growth is fueled by the increasing adoption of convenience foods, expanding middle-class population, and supportive government initiatives for food processing industries.In countries like India and China, the growing influence of Western food habits and the proliferation of modern retail formats are accelerating market penetration. Government initiatives aimed at reducing food wastage and improving cold chain infrastructure are further supporting growth. The rise of e-commerce platforms and online grocery services is also playing a crucial role in expanding market reach. Additionally, the increasing awareness of health and nutrition is encouraging consumers to incorporate frozen fruits and vegetables into their diets, contributing to the region’s rapid growth.

Latin America

Latin America holds a modest share of approximately 6–8%, with Brazil and Mexico leading the market. The region’s growth is primarily driven by the abundance of agricultural resources, increasing export opportunities, and gradual development of cold chain infrastructure. Frozen fruits and vegetables are gaining popularity as a means of preserving surplus production and reducing post-harvest losses.The expansion of the food processing industry and the growing demand for convenience foods are also contributing to market growth. As urbanization increases and consumer lifestyles evolve, the demand for ready-to-cook and ready-to-eat products is rising. Additionally, government initiatives aimed at promoting agricultural exports and improving supply chain efficiency are supporting the development of the frozen fruits and vegetables market in the region.

Middle East & Africa

The Middle East & Africa region is gradually expanding, supported by improving cold chain infrastructure and rising demand for imported frozen products. Key markets include the United Arab Emirates and South Africa. The regional growth is driven by the increasing reliance on food imports, growing urban population, and rising demand for convenient and long-lasting food products.In the Middle East, limited agricultural production capabilities necessitate the import of frozen fruits and vegetables, creating significant growth opportunities for international suppliers. The expansion of modern retail formats and the increasing penetration of supermarkets and hypermarkets are enhancing product availability. In Africa, improving logistics and infrastructure are facilitating market growth, while rising consumer awareness and changing dietary habits are driving demand. Overall, the region presents promising opportunities, supported by ongoing investments in cold chain development and food distribution networks.

Key Players in the Frozen Fruits and Vegetables Market

- Nestlé S.A.

- Conagra Brands, Inc.

- General Mills, Inc.

- Nomad Foods Ltd.

- Lamb Weston Holdings, Inc.

- McCain Foods Limited

- Greenyard NV

- Dole plc

- Ardo Group

- Bonduelle Group

- Kraft Heinz Company

- Simplot Company

- B&G Foods, Inc.

- Iceland Foods Ltd.

- Ajinomoto Co., Inc.