Frozen French Fries Market Size

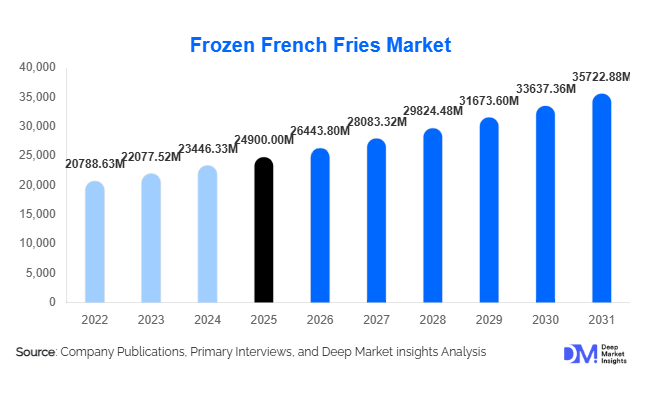

According to Deep Market Insights, the global frozen french fries market size was valued at USD 24,900 million in 2025 and is projected to grow from USD 26,443.80 million in 2026 to reach USD 35,722.88 million by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The frozen french fries market growth is primarily driven by the rapid expansion of quick service restaurants (QSRs), rising global demand for convenience foods, increasing urbanization, and continuous advancements in cold-chain logistics and IQF freezing technologies that enhance product quality and shelf life.

Key Market Insights

- QSR expansion remains the dominant consumption driver, with frozen fries serving as a standardized core menu item across global fast-food chains.

- Asia-Pacific is emerging as the fastest-growing consumption hub, supported by rising disposable incomes and Western dietary influence.

- IQF frozen fries dominate processing formats, accounting for the largest share due to superior texture preservation and export efficiency.

- Retail penetration of frozen potato products is rising rapidly, driven by e-commerce grocery platforms and modern supermarkets.

- Europe and North America continue to lead global consumption, supported by mature fast-food ecosystems and high per-capita frozen food intake.

- Product innovation is accelerating, with demand increasing for air-fryer compatible, low-oil, organic, and coated fries.

What are the latest trends in the frozen french fries market?

Premiumization and Health-Oriented Product Innovation

The frozen french fries market is witnessing a strong shift toward premium and health-focused offerings. Manufacturers are introducing low-oil, non-GMO, organic, and air-fryer-compatible fries to align with evolving consumer health consciousness. Coated fries designed for enhanced crispiness and reduced oil absorption are gaining traction in both retail and foodservice channels. Clean-label formulations and reduced acrylamide production techniques are also becoming standard, particularly in Europe and North America, where regulatory scrutiny is higher. This trend is enabling brands to move beyond commodity pricing and capture higher margins through product differentiation.

Cold Chain Expansion and Export-Led Growth

Improved cold-chain infrastructure is significantly enhancing global trade in frozen fries. Emerging economies such as India and China are investing heavily in integrated food processing zones and refrigerated logistics networks, enabling large-scale exports to Europe, the Middle East, and North America. Advanced freezing technologies, automated sorting systems, and AI-driven quality control are reducing wastage and improving operational efficiency. As a result, mid-tier manufacturers are increasingly entering global supply chains, strengthening international competition and supply diversification.

What are the key drivers in the frozen french fries market?

Rapid Expansion of Quick Service Restaurants (QSRs)

The global proliferation of QSR chains is the most significant growth driver for the frozen french fries market. Fast-food brands rely on frozen fries for consistency, cost efficiency, and standardized preparation across outlets. With QSR growth rates exceeding 5–7% annually in emerging markets, demand for frozen fries continues to surge. Large-scale contracts between suppliers and global fast-food chains further stabilize long-term demand and encourage capacity expansion among manufacturers.

Urbanization and Changing Consumer Lifestyles

Increasing urbanization, rising dual-income households, and fast-paced lifestyles are driving demand for convenient food products. Frozen french fries offer easy preparation, long shelf life, and consistent taste, making them a preferred choice in both households and foodservice. The growing influence of Western diets in Asia-Pacific and Latin America is further accelerating consumption patterns, especially among younger demographics.

Advancements in Freezing and Food Processing Technologies

Technological improvements such as IQF freezing, vacuum sealing, and automated peeling and cutting systems have significantly improved product quality and operational efficiency. These advancements reduce spoilage, extend shelf life, and enhance texture retention after frying, making frozen fries more appealing to both retailers and foodservice operators.

What are the restraints for the global market?

Volatility in Raw Potato Prices

The frozen french fries industry is highly dependent on potato cultivation, making it vulnerable to seasonal fluctuations, climate conditions, and agricultural yield variability. Price instability directly impacts production costs and profit margins, particularly for mid-sized manufacturers without integrated farming operations.

Health Concerns and Regulatory Pressure

Increasing consumer awareness regarding processed food consumption, acrylamide formation, sodium levels, and trans fats is creating regulatory pressure across developed markets. Governments and health agencies are imposing stricter labeling and nutritional standards, forcing manufacturers to invest in reformulation and compliance-driven product development.

What are the key opportunities in the frozen french fries industry?

Expansion in Emerging QSR Markets

Emerging economies in Asia-Pacific, the Middle East, and Latin America present strong expansion opportunities due to rapid QSR penetration and growing Western food adoption. Countries such as India, Indonesia, Vietnam, and Saudi Arabia are witnessing aggressive fast-food chain expansion, creating sustained demand for frozen fries. Establishing localized production facilities in these regions can significantly reduce logistics costs and enhance supply chain efficiency.

Growth of Retail and E-commerce Distribution

The rapid rise of online grocery platforms and quick-commerce delivery services is reshaping frozen food consumption. Frozen french fries are increasingly being sold through digital retail channels, enabling brands to directly reach households. This shift is expanding consumer accessibility and boosting impulse purchases in urban markets.

Sustainable and Value-Added Product Innovation

There is growing opportunity in sustainable production practices, including renewable-energy-based processing plants, recyclable packaging, and water-efficient potato farming. Additionally, value-added products such as seasoned fries, gourmet variants, and plant-based coating technologies are enabling manufacturers to capture premium pricing segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 24900.00 Million |

| Market Size in 2026 | USD 26443.80 Million |

| Market Size in 2031 | USD 35722.88 Million |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen fries market demonstrates a highly structured product segmentation, with straight cut fries continuing to dominate the landscape due to their universal acceptance across foodservice and retail channels. In 2025, straight cut fries account for approximately 38% share of the total market, primarily driven by their operational efficiency, standardized cooking performance, and compatibility with large-scale quick service restaurant (QSR) operations. Their uniform shape ensures consistent frying time, reduced oil absorption variability, and predictable plating presentation, making them the preferred choice for multinational fast-food chains that prioritize operational uniformity and cost efficiency.The leading growth driver for straight cut fries is the continued global expansion of QSR networks, particularly in emerging economies where standardized Western-style menus are being rapidly adopted. Additionally, advancements in frozen processing technology, including improved blanching and cryogenic freezing, have enhanced texture retention and extended shelf life, further strengthening demand in both developed and developing markets.Wedges and steak fries maintain a stable but niche position within the market, largely concentrated in casual dining restaurants and premium steakhouse-style establishments. Their appeal lies in their thicker cut and higher potato content per serving, which aligns with indulgent eating occasions. The key driver for this segment is the growing demand for hearty, comfort-based food options in dine-in environments where portion value perception is important.Specialty fries, including seasoned, coated, and flavored variants, represent the fastest-growing category in the global market. This growth is strongly influenced by the premiumization trend in frozen food consumption, where consumers seek differentiated taste profiles such as spicy, herb-infused, cheese-coated, or truffle-flavored fries. The leading driver for this segment is innovation in flavor development combined with rising demand for experiential eating. Food manufacturers are increasingly investing in R&D to introduce region-specific flavor profiles, which has significantly expanded adoption in both retail and foodservice channels.

Application Insights

Quick service restaurants remain the dominant application segment, accounting for nearly 45% of total global demand. This dominance is rooted in the global proliferation of fast-food chains and standardized menu structures that rely heavily on frozen fries as a core side item. QSRs prioritize frozen fries due to their operational efficiency, reduced preparation time, and ability to maintain consistent taste across multiple outlets worldwide.Retail consumption of frozen fries is expanding at a steady pace, driven by increasing household adoption of frozen convenience foods. Consumers are increasingly opting for frozen fries due to their ease of preparation, long shelf life, and cost efficiency compared to dining out. The key driver in the retail segment is the growth of modern grocery retail infrastructure, including supermarkets, hypermarkets, and online grocery platforms, which has significantly improved product accessibility.Institutional demand from schools, hospitals, corporate cafeterias, and defense catering remains relatively stable, with growth driven by bulk procurement requirements and standardized meal planning systems. The primary driver in this segment is cost-effective large-scale food provisioning, where frozen fries offer consistency and minimal preparation complexity.Food processing applications are also witnessing notable expansion, particularly as ready-meal manufacturers increasingly integrate frozen fries into packaged food offerings. The leading driver here is the rising demand for convenience meals, including frozen burgers, wraps, and meal kits, where fries serve as complementary components enhancing product value.Export-driven demand is another important contributor, particularly from established production hubs in Europe and North America supplying high-demand regions in Asia and the Middle East. The driver for this segment is global trade liberalization combined with improved cold-chain logistics enabling long-distance distribution without quality degradation.

Distribution Channel Insights

The global frozen fries market is primarily dominated by B2B foodservice supply channels, which serve as the backbone of distribution networks worldwide. These channels operate through long-term contractual agreements with QSR chains, restaurant groups, and institutional buyers, ensuring stable demand and predictable supply cycles. The leading driver of this segment is the need for supply chain reliability and cost predictability in high-volume foodservice operations.Retail packaged sales are expanding steadily, particularly in developed markets where frozen food penetration is high. Supermarkets and hypermarkets remain the primary retail outlets, supported by strong freezer infrastructure and established frozen food aisles. The growth driver in this segment is increasing consumer preference for at-home dining convenience combined with rising awareness of frozen food quality improvements.Online grocery platforms and quick-commerce channels are emerging as high-growth distribution avenues, especially in urban regions. These channels benefit from digital adoption, rapid delivery models, and expanding cold-chain logistics. The key driver here is the shift toward digital grocery shopping behavior, particularly among younger, tech-savvy consumers seeking convenience and time savings.Direct supply agreements between manufacturers and large-scale foodservice operators are becoming increasingly prevalent. These agreements eliminate intermediary costs and ensure consistent product quality and pricing stability. The primary driver for this channel is operational efficiency and the need for customized product specifications tailored to specific restaurant chains.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen French Fries Market Segmentations

By Product Type

- Straight Cut Fries

- Crinkle Cut Fries

- Wedges Fries

- Shoestring Fries

- Steak Fries

- Specialty & Seasoned Fries

By Processing Type

- IQF (Individually Quick Frozen) Fries

- Blanched & Pre-Fried Frozen Fries

- Fully Fried Frozen Fries

By Nature

- Conventional Frozen French Fries

- Organic Frozen French Fries

By End-Use Industry

- Quick Service Restaurants (QSRs)

- Full-Service Restaurants (FSRs)

- Retail / Supermarkets & Hypermarkets

- Institutional Catering

- Food Processing Industry

By Distribution Channel

- B2B Foodservice Supply

- Retail Packaged Sales

- Online Grocery & Quick Commerce Platforms

Regional Insights

North America

North America holds approximately 28% market share, with the United States and Canada serving as the core consumption hubs. The region benefits from a deeply entrenched fast-food culture, high per capita frozen food consumption, and a highly developed cold-chain infrastructure that ensures product integrity across long distribution routes.The leading growth driver in North America is the sustained expansion and modernization of QSR chains, coupled with increasing demand for premium frozen food products in retail channels. Additionally, shifting consumer lifestyles characterized by time constraints and preference for convenience meals further reinforce market growth. Technological advancements in freezing and packaging also support extended shelf life and improved product quality, enhancing consumer trust in frozen fries.

Europe

Europe represents the largest regional market, accounting for approximately 32% share, with Belgium, Netherlands, Germany, France, and the United Kingdom playing key roles in both consumption and production. The region is a global hub for potato processing and frozen food exports, supported by advanced agricultural practices and strong industrial processing capabilities.The primary growth driver in Europe is the combination of strong frozen food culture and increasing demand for premium and sustainable food products. Consumers in the region demonstrate high acceptance of frozen foods, while regulatory emphasis on sustainability is pushing manufacturers to adopt energy-efficient processing and eco-friendly packaging solutions. Furthermore, Europe’s strong export orientation continues to support global supply chains.

Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by rapid urbanization, rising disposable incomes, and expanding QSR penetration across China, India, Japan, and Southeast Asia. The region is also emerging as both a major consumption and production hub due to favorable manufacturing costs and improving cold-chain infrastructure.The leading growth driver in Asia-Pacific is the rapid transformation of dietary patterns influenced by Western food culture adoption. Increasing youth population, expansion of organized retail, and aggressive fast-food chain penetration are significantly boosting demand. Additionally, investments in refrigerated logistics networks are improving accessibility in tier-2 and tier-3 cities, further accelerating market expansion.

Latin America

Latin America, led by Brazil and Mexico, is experiencing steady growth supported by expanding urban populations and increasing adoption of fast-food culture. The region is witnessing rising integration of frozen fries into both foodservice and retail consumption patterns.The primary driver for Latin America is the growth of middle-class income groups combined with the rapid expansion of international QSR chains. Urbanization is also playing a critical role, as consumers in metropolitan areas increasingly adopt convenience-oriented food products. Improvements in cold-chain infrastructure are further enhancing product availability and distribution efficiency.

Middle East & Africa

The Middle East & Africa region is witnessing consistent growth driven by tourism development, hospitality sector expansion, and increasing Western dietary influence. Countries such as Saudi Arabia, United Arab Emirates, South Africa, and Kenya are key contributors to regional demand.The leading growth driver in this region is the expansion of tourism and hospitality infrastructure, particularly in Gulf countries where large-scale foodservice operations cater to international visitors. Additionally, rising urbanization and increasing disposable incomes are encouraging greater adoption of frozen convenience foods. Investments in cold-chain logistics are also improving supply chain efficiency, enabling broader market penetration across diverse geographies.

Key Players in the Frozen French Fries Market

- McCain Foods

- Lamb Weston Holdings

- J.R. Simplot Company

- Royal Cosun (Aviko)

- Farm Frites International

- Agristo NV

- Clarebout Potatoes

- Agrarfrost GmbH

- Nomad Foods

- Conagra Brands

- Kraft Heinz Company

- Orkla ASA

- Himalaya Food International

- Orchard Valley Foods

- General Mills