Frozen Fish and Seafood Market Size

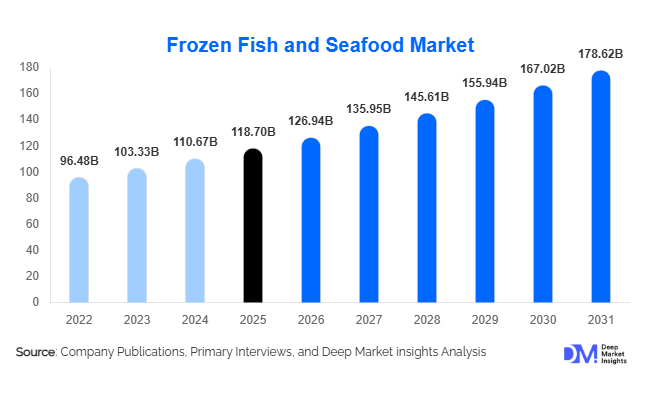

According to Deep Market Insights, the global frozen fish and seafood market size was valued at USD 118.7 billion in 2025 and is projected to grow from USD 126.94 billion in 2026 to reach USD 178.62 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). Market expansion is primarily driven by increasing global seafood consumption, rising demand for convenient protein-rich foods, advancements in cold chain logistics, and growing penetration of frozen food retail formats across emerging economies. Urbanization, changing dietary preferences toward lean protein sources, and improvements in freezing technologies that preserve nutritional value are supporting sustained adoption of frozen seafood products worldwide.

Key Market Insights

- Frozen seafood is gaining preference over fresh alternatives due to longer shelf life, reduced wastage, and stable pricing across retail and foodservice channels.

- Asia-Pacific dominates production and consumption, supported by strong aquaculture output in China, Vietnam, India, and Indonesia.

- Retail modernization and e-commerce grocery platforms are accelerating frozen seafood accessibility globally.

- Value-added seafood products such as breaded fillets, ready-to-cook shrimp, and seasoned seafood are driving premiumization.

- Cold chain investments across developing economies are reducing logistics losses and expanding export potential.

- Sustainability certifications and traceability technologies are increasingly influencing purchasing decisions among consumers and retailers.

What are the latest trends in the frozen fish and seafood market?

Rise of Value-Added and Ready-to-Cook Seafood

Consumers increasingly prefer convenience-oriented frozen seafood formats requiring minimal preparation. Products such as marinated fillets, breaded shrimp, seafood mixes, and microwave-ready meals are witnessing strong demand, particularly in North America and Europe. Manufacturers are expanding product innovation around flavor customization, portion-controlled packaging, and health-focused formulations such as low-sodium or high-protein offerings. This shift is transforming frozen seafood from a commodity category into a branded, differentiated segment with higher margins.

Digital Traceability and Sustainable Sourcing

Sustainability concerns and regulatory scrutiny are pushing seafood companies toward transparent sourcing practices. Blockchain-enabled traceability, eco-labeling, and certification programs are becoming competitive differentiators. Retailers increasingly require proof of sustainable fishing or aquaculture practices, encouraging suppliers to adopt responsible harvesting techniques. Consumers are also showing willingness to pay premium prices for responsibly sourced seafood, reinforcing long-term adoption of certified frozen seafood products.

What are the key drivers in the frozen fish and seafood market?

Growing Demand for Affordable Protein Sources

Fish and seafood are widely recognized as nutritionally dense protein sources rich in omega-3 fatty acids. Rising health awareness and dietary shifts away from red meat are increasing seafood consumption globally. Frozen formats enable wider distribution while maintaining quality, making seafood accessible in landlocked and non-coastal regions.

Expansion of Cold Chain Infrastructure

Rapid investments in refrigerated storage, temperature-controlled logistics, and modern retail refrigeration systems have significantly improved frozen food penetration. Governments and private players are investing heavily in cold storage networks, particularly across Asia-Pacific, Latin America, and Africa. Enhanced cold chains reduce spoilage and expand export capabilities, enabling year-round seafood availability.

Growth of Foodservice and Quick-Service Restaurants

Restaurants, hotels, and quick-service chains increasingly rely on frozen seafood due to consistent quality and predictable supply. Frozen products simplify inventory management while minimizing food waste. Expansion of global seafood cuisines and sushi consumption trends further supports institutional demand.

What are the restraints for the global market?

Volatility in Raw Material Supply

Fish availability is influenced by climate change, overfishing regulations, seasonal variability, and environmental disruptions. Supply fluctuations create pricing instability and procurement challenges for processors and exporters.

Energy-Intensive Storage and Logistics Costs

Frozen seafood relies heavily on continuous refrigeration across transportation and storage stages. Rising electricity costs and sustainability pressures increase operational expenses, particularly in developing markets with unstable power infrastructure.

What are the key opportunities in the frozen fish and seafood industry?

Expansion into Emerging Urban Markets

Rapid urbanization in Southeast Asia, Africa, and Latin America presents significant opportunities for frozen seafood adoption. Modern supermarkets and online grocery platforms are expanding rapidly, introducing frozen protein options to middle-income households. Companies entering these markets early can establish strong brand loyalty and distribution advantages.

Technological Advancements in Freezing Techniques

Innovations such as Individual Quick Freezing (IQF), cryogenic freezing, and smart packaging technologies improve texture retention and extend shelf life. Adoption of advanced freezing methods allows manufacturers to market frozen seafood as nutritionally comparable to fresh products, reducing consumer perception barriers.

Growth in Export-Oriented Aquaculture Production

Aquaculture expansion in countries such as India, Vietnam, Ecuador, and Norway is increasing global supply stability. Export-focused policies and trade agreements are encouraging seafood processing investments, enabling producers to capture higher-value international markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 118.7 Billion |

| Market Size in 2026 | USD 126.94 Billion |

| Market Size in 2031 | USD 178.62 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The frozen seafood market is characterized by a diversified product portfolio that caters to evolving consumer dietary preferences, global trade dynamics, and advancements in preservation technologies. Among all categories, frozen fish continues to dominate the global market landscape, accounting for approximately 46% of total market revenue in 2025. This leadership position is primarily driven by the widespread global consumption of species such as salmon, tuna, cod, pollock, and tilapia, which are widely accepted across cultures due to their nutritional value, affordability, and culinary versatility. Frozen fish products benefit significantly from their adaptability across retail, foodservice, and industrial processing applications, making them a staple category in both developed and emerging markets.Value-added seafood products represent the fastest-growing subsegment within the frozen seafood market. Products such as breaded fish fillets, marinated shrimp, seasoned seafood portions, and ready-to-cook meal components are gaining widespread acceptance. The leading growth driver for this segment is the rising consumer preference for convenience-oriented foods that reduce preparation time without compromising taste or nutrition. Manufacturers are increasingly investing in flavor innovation, portion-controlled packaging, and premium branding strategies to capture higher margins and differentiate offerings in competitive retail environments. As consumer lifestyles become increasingly fast-paced, value-added frozen seafood is expected to play a central role in shaping future market expansion.

Processing Type Insights

Processing technologies play a critical role in determining product quality, shelf stability, and market competitiveness within the frozen seafood industry. Individually Quick Frozen (IQF) processing leads globally, accounting for nearly 52% of total market share in 2025. IQF technology rapidly freezes individual pieces of seafood, preventing ice crystal formation that can damage cellular structure. This process preserves natural texture, flavor, and nutritional integrity while allowing consumers and foodservice operators to thaw only the required portion, minimizing waste.The leading driver behind IQF dominance is its superior flexibility across retail and commercial applications. Consumers benefit from portion control and convenience, while restaurants gain operational efficiency through consistent product quality. IQF products also align well with modern packaging formats such as resealable bags and portion packs, which are increasingly preferred by urban households. As cold-chain infrastructure improves globally, IQF technology continues to expand into emerging markets where quality preservation during transportation is critical.Cooked and pre-processed frozen seafood is experiencing rapid expansion as consumers increasingly prioritize ready-to-eat and ready-to-heat meal solutions. Pre-cooked shrimp, grilled fish portions, and seasoned seafood dishes appeal strongly to consumers seeking restaurant-quality meals at home. The growth of this processing segment is driven primarily by changing lifestyle patterns, rising workforce participation, and the increasing popularity of home dining experiences influenced by digital recipe platforms and food delivery culture. Manufacturers are integrating automation and advanced processing techniques to improve food safety, consistency, and scalability, further accelerating adoption.

Distribution Channel Insights

Distribution channels significantly influence purchasing behavior and market penetration within the frozen seafood industry. Retail distribution dominates global sales, accounting for approximately 58% of total market revenue. Supermarkets and hypermarkets remain the primary retail outlets due to their extensive freezer infrastructure, wide product assortments, and established consumer trust. Retailers increasingly allocate larger freezer space to seafood products as consumer demand for healthy frozen protein alternatives continues to rise.Foodservice distribution represents a steadily expanding channel supported by global growth in dining-out culture and the diversification of seafood-based menus. Quick-service restaurants, casual dining chains, and hotel operators increasingly rely on frozen seafood due to consistent quality, predictable pricing, and simplified inventory management. Frozen seafood allows chefs to maintain menu stability regardless of seasonal fishing fluctuations, making it an essential supply component across hospitality sectors. The recovery and expansion of global tourism and hospitality industries further reinforce demand through bulk procurement contracts and standardized supply requirements.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for nearly 54% of global frozen seafood demand. The leading driver for this segment is the growing preference for home cooking combined with increasing health consciousness among consumers. Frozen seafood provides an accessible and nutritious protein option with extended storage capability, enabling households to maintain meal flexibility without frequent grocery visits. Rising awareness of balanced diets, combined with culinary experimentation influenced by social media and cooking platforms, continues to boost household seafood consumption.Institutional buyers such as airlines, cruise operators, hospitals, and catering companies contribute to long-term market stability through large-scale procurement agreements. Frozen seafood aligns well with institutional foodservice requirements due to standardized quality, longer shelf life, and efficient inventory planning. As global travel and event industries expand, institutional demand is expected to provide consistent baseline consumption levels that support overall market resilience.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Fish and Seafood Market Segmentations

By Product Type

- Frozen Fish

- Frozen Crustaceans

- Frozen Mollusks

- Frozen Processed Seafood

By Processing Type

- Raw Frozen Seafood

- Cooked Frozen Seafood

- Breaded & Value-Added Seafood

- Individually Quick Frozen (IQF) Products

By Distribution Channel

- Retail Stores

- Foodservice Distribution

- Online Retail & E-commerce

- Institutional Sales

By End Use

- Household Consumption

- Restaurants & Quick Service Restaurants (QSRs)

- Hotels & Catering Services

- Food Processing Industry

Regional Insights

Asia-Pacific

Asia-Pacific held approximately 41% of the global frozen seafood market share in 2025, making it the largest regional market worldwide. The region’s leadership is supported by its dual role as both a major production hub and a rapidly expanding consumption market. China dominates regional dynamics through its extensive aquaculture industry, advanced seafood processing capabilities, and strong export infrastructure. Government support for aquaculture modernization and technological integration continues to enhance productivity and global competitiveness.Japan and South Korea contribute through high-value consumption patterns, where consumers prioritize premium seafood quality and convenience. The key regional growth driver is the rapid expansion of cold storage infrastructure and modern retail networks, which are enabling frozen seafood penetration into emerging middle-class markets across Southeast Asia.

North America

North America accounts for nearly 21% of global market share, with the United States serving as the primary demand center. High seafood consumption levels, combined with strong retail distribution systems and consumer preference for healthy protein alternatives, drive regional growth. Frozen salmon, shrimp, and ready-to-cook seafood products are particularly popular among health-conscious consumers seeking convenient meal options.The leading regional growth driver is the increasing adoption of value-added seafood products supported by busy lifestyles and rising demand for premium convenience foods. Expansion of online grocery platforms and meal-kit services has further accelerated frozen seafood purchases. Canada complements regional growth through sustainable fisheries management and export-oriented production, strengthening supply reliability while aligning with consumer demand for responsibly sourced seafood.

Europe

Europe represents a mature yet steadily expanding frozen seafood market led by Norway, Spain, the United Kingdom, Germany, and France. Norway remains one of the world’s largest exporters of frozen salmon, supplying high-quality products to global markets. Southern European countries maintain strong seafood consumption traditions, supporting consistent domestic demand.A primary growth driver in Europe is the region’s strong emphasis on sustainability and traceability. Regulatory frameworks and eco-labeling initiatives influence purchasing behavior, encouraging retailers and manufacturers to adopt certified sourcing practices. Consumers increasingly prefer frozen seafood as it reduces food waste compared to fresh alternatives, aligning with environmental awareness trends. Additionally, premiumization strategies and gourmet frozen seafood offerings are expanding retail value growth despite relatively stable consumption volumes.

Middle East & Africa

The Middle East and Africa region is experiencing rising frozen seafood demand driven by population growth, urban expansion, and increasing reliance on imports due to limited domestic fisheries capacity in several countries. The United Arab Emirates and Saudi Arabia lead regional consumption through rapid retail modernization and strong hospitality sector expansion.The primary regional growth driver is the expansion of tourism and foodservice industries, which require consistent seafood supply throughout the year. Frozen products provide logistical advantages in hot climates where maintaining fresh seafood quality is challenging. South Africa acts as a regional processing and distribution hub, supporting intra-regional trade and export activity. Growing middle-class populations and improving cold storage infrastructure are further accelerating market development across African economies.

Latin America

Latin America demonstrates strong export-oriented growth supported by abundant marine resources and competitive aquaculture industries. Ecuador leads global shrimp exports, benefiting from technological advancements in farming and processing efficiency. Chile’s salmon industry plays a vital role in supplying premium frozen seafood to North America, Europe, and Asia.The leading regional growth driver is increasing international demand for sustainably sourced seafood combined with favorable trade relationships. Governments across the region are investing in aquaculture expansion and certification programs to enhance export competitiveness. Domestic consumption is also gradually increasing as modern retail channels expand and frozen food acceptance rises among urban consumers. As logistics infrastructure continues to improve, Latin America is expected to strengthen its position as a key supplier within global frozen seafood trade networks.

Key Players in the Frozen Fish and Seafood Market

- Mowi ASA

- Thai Union Group PCL

- Maruha Nichiro Corporation

- Nippon Suisan Kaisha Ltd.

- Nomad Foods Limited

- High Liner Foods Inc.

- Lerøy Seafood Group

- Cooke Inc.

- Grupo Nueva Pescanova

- Pacific Seafood

- Dongwon Industries Co., Ltd.

- Trident Seafoods Corporation

- Royal Greenland A/S

- Austevoll Seafood ASA

- Clearwater Seafoods Incorporated