Frozen Drinks Market Size

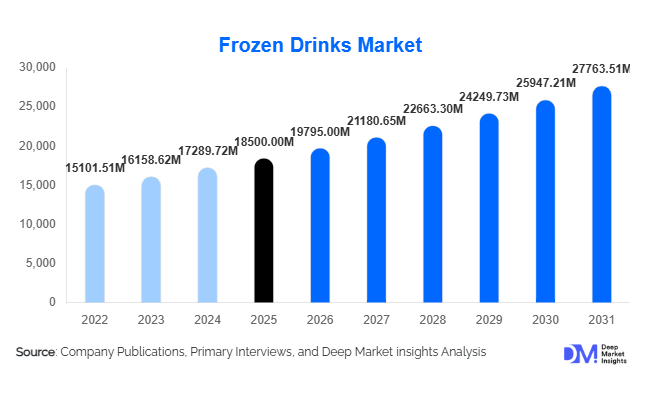

According to Deep Market Insights, the global frozen drinks market size was valued at USD 18,500 million in 2026 and is projected to grow from USD 19,795 million in 2027 to reach USD 27,763.51 million by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). The frozen drinks market growth is primarily driven by the rising demand for refreshing and indulgent beverages, rapid expansion of quick-service restaurants (QSRs) and café chains, and increasing consumer preference for experiential, customizable beverage formats such as slushies, frozen coffees, and frozen cocktails.

Key Market Insights

- Frozen beverages are increasingly becoming an experience-led product category, driven by demand for visually appealing, flavored, and customizable drinks across retail and foodservice outlets.

- QSR and café chains dominate consumption, with large global brands expanding frozen beverage dispensing systems across urban outlets.

- North America remains the largest market, supported by high penetration of frozen drink machines and strong consumer adoption.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable incomes, and expanding Western-style foodservice culture.

- Fruit-based and slush-based drinks are leading segments, supported by affordability and strong seasonal demand.

- Technological advancements in automated dispensing systems are transforming product consistency, operational efficiency, and flavor innovation.

What are the latest trends in the frozen drinks market?

Health-Oriented and Plant-Based Frozen Beverages

Consumers are increasingly shifting toward healthier indulgence options, driving demand for low-sugar, natural, and plant-based frozen drinks. Almond, oat, coconut, and fruit-based formulations are gaining traction, especially among urban Gen Z and millennial consumers. Functional ingredients such as vitamins, electrolytes, and probiotics are being added to frozen smoothies and slush beverages, creating a hybrid between refreshment and wellness. This trend is also encouraging manufacturers to reduce artificial syrups and adopt clean-label formulations.

Smart Dispensing and Automation in Beverage Retail

The adoption of IoT-enabled frozen drink machines is transforming the retail experience. Automated dispensing systems ensure consistency, reduce labor dependency, and allow real-time monitoring of inventory and machine performance. AI-powered flavor customization is also emerging in high-traffic QSR outlets, enabling personalized beverage creation. These systems are particularly popular in cinemas, amusement parks, and convenience stores, where high-volume, fast-service beverage delivery is essential.

What are the key drivers in the frozen drinks market?

Expansion of QSR and Café Culture

The rapid expansion of global QSR chains and café outlets is a major growth driver. Frozen drinks have become a core menu offering in major fast-food and coffee chains, contributing significantly to impulse sales. Urbanization and increasing consumption of on-the-go beverages are further strengthening demand across both developed and emerging markets. Franchise expansion in Asia-Pacific and Latin America is particularly accelerating product penetration.

Rising Demand for Experiential Beverages

Consumers are increasingly seeking beverages that offer sensory and experiential value beyond traditional drinks. Frozen drinks provide texture, visual appeal, and customization, making them highly attractive in social and entertainment settings. Seasonal demand spikes during summer months and tourism-heavy regions further boost market consumption. This experiential trend is especially strong among younger consumers.

Growth of Retail and Convenience Channels

Convenience stores, supermarkets, and Q-commerce platforms are expanding frozen drink availability through ready-to-mix syrups and packaged concentrates. This has made frozen beverages more accessible for at-home consumption, supporting steady market expansion beyond foodservice channels.

What are the restraints for the global market?

High Equipment and Operational Costs

Frozen beverage machines require significant upfront investment and maintenance costs, limiting adoption among small and independent retailers. Energy consumption and servicing requirements further increase operational expenses, particularly in developing regions.

Health Concerns and Sugar Content Regulations

Rising awareness of sugar intake and artificial additives is restricting consumption in health-conscious markets. Regulatory pressure in North America and Europe is pushing manufacturers to reformulate products, which increases R&D and production complexity.

What are the key opportunities in the frozen drinks industry?

Expansion in Emerging Markets

Rapid urbanization in India, Southeast Asia, and Latin America presents significant opportunities for frozen drink manufacturers. Growing café culture and QSR penetration are creating strong demand for affordable indulgence beverages, particularly slush-based drinks.

Product Innovation in Functional Beverages

The integration of functional ingredients such as energy boosters, vitamins, and immunity-supporting compounds offers strong differentiation potential. This is opening new consumer segments beyond traditional indulgence-focused buyers.

Tourism and Entertainment-Driven Consumption

Amusement parks, cinemas, stadiums, and tourist hubs represent high-margin consumption points for frozen beverages. These environments support impulse buying behavior, making them key revenue generators for operators.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18500.00 Million |

| Market Size in 2026 | USD 19795.00 Million |

| Market Size in 2031 | USD 27763.51 Million |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen drinks market is characterized by a diverse range of product types, each catering to distinct consumer preferences, consumption environments, and evolving lifestyle trends. Among these, slush-based frozen drinks continue to dominate the market with an estimated 28% share in 2025. Their leadership is primarily driven by their affordability, high visual appeal, and strong presence across convenience stores, amusement parks, cinema halls, and quick-service restaurant (QSR) chains. The vibrant colors, customizable flavor options, and refreshing texture of slush beverages make them particularly attractive to younger consumers and impulse buyers. Additionally, their relatively low production cost and compatibility with automated dispensing machines have enabled large-scale adoption across both developed and emerging markets. The growing popularity of experiential food and beverage consumption, where aesthetics and novelty play a significant role, further reinforces the dominance of slush-based drinks.Alcoholic frozen beverages are gaining notable traction, especially in bars, clubs, resorts, and entertainment venues. These beverages combine the refreshing characteristics of frozen drinks with alcoholic content, making them particularly popular in nightlife and tourism-driven markets. Innovations such as frozen margaritas, daiquiris, and wine-based slush cocktails are contributing to segment expansion. The growth of experiential nightlife culture, along with increasing tourism in tropical and coastal regions, is further accelerating demand. Additionally, seasonal festivals and outdoor events significantly boost consumption of alcoholic frozen drinks.Plant-based frozen beverages represent the fastest-growing sub-segment within the market, driven by rising veganism, lactose intolerance awareness, and broader health and sustainability trends. Consumers are increasingly seeking dairy-free alternatives made from almond, oat, coconut, and soy bases. This shift is strongly supported by environmental concerns and the perception of plant-based diets as healthier and more ethical. Beverage manufacturers are investing heavily in formulation innovation to improve texture, flavor, and nutritional value, thereby enhancing mainstream acceptance. As sustainability continues to influence purchasing behavior, plant-based frozen drinks are expected to register sustained high growth across all major regions.

Application Insights

The application landscape of the frozen drinks market is broad and continues to evolve with changing consumption patterns, technological advancements, and expanding retail and foodservice ecosystems. The foodservice sector remains the dominant application area, accounting for the majority of global frozen drink consumption. Within this segment, QSRs, cafés, cinemas, and casual dining restaurants play a central role in driving demand. The growth of global fast-food chains and standardized beverage offerings has significantly contributed to the widespread availability of frozen drinks. High footfall environments such as multiplexes and entertainment parks further reinforce bulk consumption patterns, particularly among younger demographics and families.Retail consumption is steadily expanding as consumers increasingly replicate café-style beverages at home. The availability of ready-to-mix syrups, frozen drink concentrates, and home-use slush machines is transforming the at-home consumption experience. This shift is largely driven by convenience-oriented lifestyles, rising disposable incomes, and growing interest in DIY beverage customization. Supermarkets, hypermarkets, and online grocery platforms are playing a crucial role in increasing product accessibility. The COVID-19 pandemic also accelerated at-home beverage experimentation, a trend that continues to influence long-term consumer behavior.Institutional demand from airports, stadiums, hospitals, and amusement parks is another important growth driver. These high-traffic environments require large-scale beverage solutions that are efficient, quick to serve, and universally appealing. Frozen drinks fit these requirements perfectly, offering high margin potential and operational simplicity. Tourism-driven consumption further enhances this segment, particularly in destinations with high visitor turnover and hot climates. Seasonal tourism peaks significantly influence sales cycles, making this application highly dynamic and regionally sensitive.

Distribution Channel Insights

The distribution structure of the frozen drinks market is undergoing significant transformation, influenced by digitalization, changing consumer behavior, and expansion of organized retail. On-trade channels continue to dominate the market with approximately 46% share, primarily driven by QSRs, cafés, bars, and entertainment venues. These channels benefit from high-volume consumption, impulse purchases, and strong brand-driven beverage offerings. The on-trade segment is also supported by the growing culture of social dining and experiential consumption, where frozen beverages play a key role in enhancing customer experience.Off-trade retail channels are witnessing steady expansion, supported by increasing penetration of supermarkets, convenience stores, and hypermarkets. The availability of packaged frozen drink mixes, syrups, and concentrates has enabled consumers to access products outside traditional foodservice environments. This shift is further supported by rising urbanization and increasing household penetration of refrigeration and beverage preparation appliances. Retail branding strategies, combined with attractive packaging and flavor innovation, are enhancing product visibility and consumer engagement in this segment.Direct-to-consumer (DTC) sales of beverage equipment, including slush machines and frozen drink dispensers, are also gaining traction. Small businesses, cafés, and even households are increasingly investing in compact beverage preparation systems. This trend is supported by technological advancements, affordability improvements, and growing entrepreneurial activity in the food and beverage sector. As consumers continue to seek personalized beverage experiences, DTC channels are expected to expand further.

Consumer Insights

Consumer behavior in the frozen drinks market is strongly influenced by demographic factors, lifestyle preferences, and digital engagement. The largest consumer base is represented by individuals aged 18–35, who are highly responsive to visual appeal, customization options, and social media-driven food trends. This demographic values experiential consumption and is highly influenced by platforms such as Instagram and TikTok, where frozen beverages often gain viral popularity due to their aesthetic presentation and innovative flavors.Families and children also represent a significant consumer segment, particularly in QSRs, amusement parks, and cinema environments. Frozen drinks are perceived as fun, safe, and indulgent treats, making them popular choices for family outings. Seasonal promotions, combo meals, and kid-friendly flavors further enhance consumption within this segment.Older consumers tend to prefer lower-sugar, functional, and café-style frozen beverages. This demographic is increasingly health-conscious and seeks beverages that offer both refreshment and nutritional value. The introduction of sugar-free, plant-based, and fortified frozen drinks is helping manufacturers cater to this evolving preference.Social media influence plays a critical role in shaping consumption trends across all age groups. Viral beverage challenges, influencer marketing, and visually appealing product launches significantly impact consumer awareness and trial rates. As digital engagement continues to grow, consumer preferences are expected to become even more trend-driven and experience-oriented.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Drinks Market Segmentations

By Product Type

- Slush-Based Frozen Drinks

- Frozen Carbonated Beverages

- Frozen Coffee Beverages

- Frozen Tea-Based Beverages

- Frozen Dairy-Based Beverages

- Alcoholic Frozen Beverages

- Plant-Based Frozen Beverages

By Ingredient Base

- Fruit-Based Formulations

- Dairy-Based Formulations

- Plant-Based Formulations

- Artificial Flavor & Syrup-Based

By Distribution Channel

- On-Trade

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Food Delivery & Q-Commerce Platforms

By Packaging Type

- Cups & On-the-Go Servings

- Bottles

- Pouches

- Concentrates & Syrups

By End-Use

- Foodservice Industry

- Retail Consumption

- Institutional Consumption

Regional Insights

North America

North America holds approximately 38% market share in 2025, making it the largest regional market for frozen drinks. The region’s dominance is driven by high QSR penetration, advanced foodservice infrastructure, and strong consumer spending on convenience beverages. The United States leads regional demand due to its well-established fast-food ecosystem and widespread availability of frozen beverage machines across retail and entertainment outlets. The culture of on-the-go consumption and strong preference for cold beverages, particularly during summer months, further supports market expansion.Canada contributes steadily to regional growth, supported by the expansion of café culture and increasing adoption of premium frozen beverages. Health-conscious consumer trends are also influencing product innovation, particularly in low-sugar and plant-based categories. Additionally, technological advancements in beverage dispensing systems and strong brand presence of global players continue to reinforce North America’s leadership position.

Europe

Europe accounts for around 24% market share, with key markets including the United Kingdom, Germany, France, and Italy. The region’s growth is strongly influenced by café culture, tourism, and increasing demand for premium and artisanal beverages. Seasonal tourism, particularly in Mediterranean countries, significantly boosts frozen drink consumption during warmer months.A major growth driver in Europe is the rising health consciousness among consumers, which is accelerating demand for plant-based and low-sugar frozen beverages. Regulatory emphasis on healthier food and beverage formulations is also encouraging manufacturers to innovate. Additionally, the popularity of specialty cafés and artisanal beverage outlets is enhancing product diversification and premiumization across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the global frozen drinks market, driven by rapid urbanization, rising disposable incomes, and the expansion of international QSR chains. Countries such as China, India, Japan, and those in Southeast Asia are witnessing strong growth in frozen beverage consumption. The increasing influence of Western food culture, combined with changing lifestyle patterns, is significantly boosting demand.A key driver in the region is the rapid expansion of urban retail and foodservice infrastructure. The growing youth population, coupled with strong social media influence, is accelerating adoption of visually appealing and customizable beverages. Additionally, hot climatic conditions in many countries naturally support high consumption of cold beverages throughout the year. The increasing penetration of digital food delivery platforms is further strengthening market accessibility and driving long-term growth.

Latin America

Latin America, led by Brazil and Mexico, is experiencing steady growth in frozen drink consumption. The region benefits from strong demand for cold beverages due to tropical and subtropical climates. Expanding fast-food chains and increasing urbanization are further supporting market development.Economic improvements and rising middle-class incomes are enabling higher discretionary spending on foodservice experiences. Seasonal festivals, outdoor events, and beach tourism significantly contribute to consumption spikes. Additionally, the growing presence of international beverage brands is enhancing product availability and awareness.

Middle East & Africa

The Middle East & Africa region is witnessing strong demand for frozen drinks, primarily driven by hot climatic conditions, tourism growth, and expanding hospitality infrastructure. Countries such as the United Arab Emirates and Saudi Arabia are key contributors, supported by high tourist inflows and premium hospitality developments.The growth of shopping malls, entertainment complexes, and luxury dining establishments is significantly boosting consumption. Tourism-driven economies and large-scale events also play a crucial role in seasonal demand fluctuations. Furthermore, increasing investments in foodservice infrastructure and the rising popularity of international QSR chains are expected to sustain long-term growth in the region.

Key Players in the Global Frozen Drinks Market

- PepsiCo Inc.

- The Coca-Cola Company

- Nestlé S.A.

- J&J Snack Foods Corp.

- Keurig Dr Pepper Inc.

- Unilever PLC

- Starbucks Corporation

- Dunkin’ (Inspire Brands)

- Danone S.A.

- Suntory Beverage & Food Ltd.

- Asahi Group Holdings

- JDE Peet’s

- Kerry Group

- General Mills Inc.

- Monster Beverage Corporation