Frozen Chicken Paws Market Size

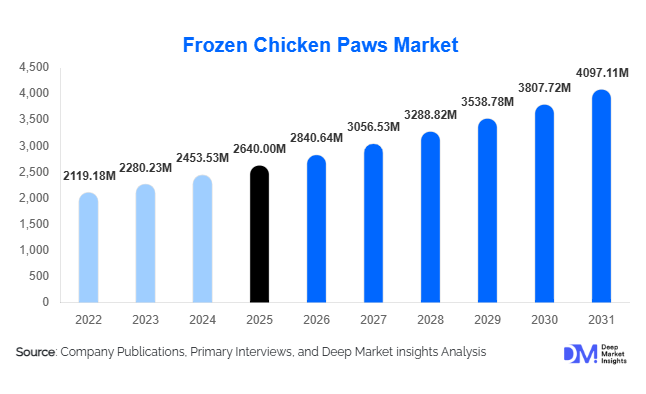

According to Deep Market Insights, the global frozen chicken paws market size was valued at USD 2,640 million in 2025 and is projected to grow from USD 2,840.64 million in 2026 to reach USD 4,097.11 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The frozen chicken paws market growth is primarily driven by strong export demand from Asia, increasing utilization of poultry by-products for profitability, and rising consumption in foodservice and processed food applications. What was once considered a low-value poultry component has evolved into a high-demand export commodity, especially in countries such as China, Vietnam, and the Philippines.

Key Market Insights

- Export-driven demand dominates the market, with over 70% of global production traded internationally, particularly toward Asian markets.

- Asia-Pacific leads global consumption, accounting for more than 60% of total demand, driven by cultural dietary preferences.

- Individually Quick Frozen (IQF) technology is gaining prominence, ensuring superior quality, longer shelf life, and better pricing realization.

- Foodservice industry remains the largest end-use segment, supported by rapid expansion of restaurants and street food culture in emerging economies.

- Latin America and North America dominate supply, with Brazil and the United States acting as major exporters.

- Value-added processing is emerging as a key growth lever, with marinated and ready-to-cook products gaining traction.

What are the latest trends in the frozen chicken paws market?

Rising Demand for Value-Added and Processed Products

The market is witnessing a shift from raw frozen chicken paws to value-added products such as marinated, pre-cooked, and flavored variants. These products cater to convenience-driven consumers and foodservice operators seeking ready-to-use ingredients. Food manufacturers are increasingly innovating with sauces and seasoning profiles tailored to regional tastes, particularly in Asia-Pacific. This trend is also helping companies achieve higher margins compared to bulk raw exports, while enhancing brand differentiation in international markets.

Advancements in Freezing and Cold Chain Technologies

Technological improvements in freezing processes, especially IQF, are transforming product quality and trade efficiency. IQF ensures individual separation, better texture retention, and reduced wastage, making it highly preferred in global trade. Additionally, investments in cold chain logistics, including refrigerated transport and storage infrastructure, are enabling exporters to expand into new markets with minimal quality degradation. Automation in poultry processing is also improving yield efficiency and reducing operational costs.

What are the key drivers in the frozen chicken paws market?

Strong Export Demand from Asia

China and Southeast Asian countries remain the primary drivers of global demand. Chicken paws are considered a delicacy in these regions, leading to consistent import volumes. Trade agreements and easing import restrictions are further supporting growth, making exports the backbone of the market.

Improved Profitability for Poultry Processors

Frozen chicken paws have transformed from a low-value byproduct into a significant revenue stream for poultry companies. Exporting paws allows processors to maximize carcass utilization and improve overall profitability, encouraging higher production volumes and investments in processing infrastructure.

Growth of Foodservice and Processed Food Sectors

The rapid expansion of quick-service restaurants (QSRs), street food vendors, and ready-to-eat meal manufacturers is boosting demand. Chicken paws are increasingly used in snacks, soups, and ready-to-cook meals, particularly in urban markets with rising disposable incomes.

What are the restraints for the global market?

Stringent Import Regulations and Quality Standards

Exporters must comply with strict sanitary and phytosanitary standards, particularly in key markets such as China and the European Union. These regulations increase compliance costs and can limit market access for smaller players lacking advanced processing capabilities.

Supply Chain Volatility and Price Fluctuations

The market is susceptible to fluctuations in poultry production, feed costs, and disease outbreaks such as avian influenza. These factors can disrupt supply chains, impact pricing stability, and create uncertainty for exporters and importers alike.

What are the key opportunities in the frozen chicken paws industry?

Expansion into Emerging Markets

Beyond China, emerging markets such as Indonesia, Nigeria, and Vietnam are showing strong growth potential due to urbanization and increasing protein consumption. Exporters can capitalize on these markets by establishing distribution networks and leveraging trade agreements to reduce tariffs.

Development of Premium and Ready-to-Cook Segments

There is significant opportunity in introducing premium, branded, and ready-to-cook chicken paw products. These offerings cater to modern retail and e-commerce channels, where consumers seek convenience and quality assurance. This shift also allows companies to capture higher margins compared to bulk exports.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2640.00 Million |

| Market Size in 2026 | USD 2840.64 Million |

| Market Size in 2031 | USD 4097.11 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen chicken paws market demonstrates a clear preference for trimmed chicken paws, which dominate the segment and account for approximately 48% of the global market share in 2025. This leadership position is primarily driven by the growing emphasis on hygiene, visual appeal, and compliance with stringent import regulations, particularly in key export destinations across Asia. Trimmed chicken paws undergo additional cleaning and processing steps that remove nails and outer skin layers, resulting in a more uniform and aesthetically acceptable product. This makes them highly suitable for premium foodservice applications and international trade, where quality consistency is non-negotiable. The leading segment driver for trimmed chicken paws is the increasing demand from export markets, especially China and Southeast Asia, where import standards and consumer expectations favor high-quality, ready-to-cook products.Whole chicken paws continue to hold a significant share as a cost-effective alternative, particularly in price-sensitive markets. These products are often preferred by small-scale processors and local foodservice operators who perform their own cleaning and preparation. However, as global supply chains modernize and food safety awareness increases, the relative share of whole chicken paws is gradually declining. In contrast, processed and marinated chicken paws are witnessing notable growth, driven by changing consumer preferences toward convenience and ready-to-eat or ready-to-cook food options. Urbanization, increasing disposable incomes, and the expansion of quick-service restaurants are further accelerating the adoption of value-added products. This shift indicates a broader transformation within the market, where traditional raw products are increasingly complemented by innovative, flavor-enhanced offerings tailored to evolving consumption patterns.

Processing Level Insights

In terms of processing level, raw frozen chicken paws dominate the market with an estimated 55% share. The primary driver behind this dominance is the flexibility they offer to importers and downstream processors. Raw frozen products serve as a base input that can be customized according to regional tastes, cooking styles, and packaging requirements. This is particularly important in markets like China and Vietnam, where local processing industries add value through seasoning, packaging, and branding. The leading segment driver here is the strong demand from international buyers who prefer to carry out processing domestically to optimize costs and tailor products to local consumer preferences.Semi-processed chicken paws, which include partially cleaned and pre-treated products, are gaining traction as they strike a balance between cost efficiency and convenience. These products reduce labor requirements for end users while maintaining a degree of flexibility in final preparation. Fully processed chicken paws, including cooked, marinated, or flavored variants, are experiencing steady growth, particularly in developed markets and urban centers. The expansion of modern retail formats, increasing penetration of cold chain infrastructure, and rising demand for convenience foods are key factors supporting this growth. Consumers are increasingly seeking ready-to-consume or minimally prepared food products, and manufacturers are responding by introducing innovative offerings that cater to these preferences.

Packaging Insights

Bulk packaging remains the dominant segment in the frozen chicken paws market, accounting for nearly 60% of the total market share. This dominance is largely attributed to the export-oriented nature of the industry, where large volumes are shipped to international markets for further processing and distribution. Bulk packaging offers significant cost advantages in terms of transportation and storage, making it the preferred choice for B2B transactions. The leading segment driver for bulk packaging is the high volume of international trade, particularly between major exporting countries like Brazil and the United States and importing countries in Asia.However, the market is witnessing a gradual shift toward retail-oriented packaging solutions, including vacuum-sealed and branded consumer packs. These formats are gaining popularity as companies increasingly target direct-to-consumer channels and premium market segments. Vacuum packaging, in particular, enhances product shelf life and maintains quality, making it suitable for high-end retail environments. The growth of e-commerce platforms, coupled with rising consumer awareness regarding food safety and quality, is further driving demand for packaged products. As a result, manufacturers are investing in advanced packaging technologies and branding strategies to differentiate their offerings and capture higher margins in competitive markets.

Distribution Channel Insights

The distribution landscape of the frozen chicken paws market is heavily dominated by direct export and B2B trade, which collectively account for approximately 65% of the market. This reflects the fundamentally export-driven structure of the industry, where large-scale producers supply international buyers through established trade networks. The leading segment driver for this channel is the strong and consistent demand from Asian markets, which rely heavily on imports to meet domestic consumption needs. Exporters benefit from long-term contracts, economies of scale, and well-developed logistics infrastructure, enabling efficient and cost-effective distribution.Foodservice distributors and wholesale markets also play a crucial role in bridging the gap between importers and end users. These intermediaries ensure timely delivery and maintain product quality across the supply chain. Meanwhile, retail channels are gaining momentum, driven by the rapid expansion of modern trade formats such as supermarkets, hypermarkets, and online grocery platforms. The increasing penetration of digital commerce is transforming the way consumers access frozen food products, creating new opportunities for market players. As consumer purchasing behavior evolves, companies are adopting omnichannel distribution strategies to enhance market reach and improve customer engagement.

End-Use Insights

The foodservice industry represents the largest end-use segment, accounting for approximately 52% of the market share. This dominance is driven by the widespread use of chicken paws in restaurants, street food outlets, and catering services, particularly in Asia-Pacific. Chicken paws are a staple ingredient in various traditional dishes, and their affordability and versatility make them highly attractive to foodservice operators. The leading segment driver is the strong cultural preference for chicken paws in key consumption markets, combined with the rapid growth of the hospitality sector.The food processing industry is another significant and rapidly expanding segment. Manufacturers are increasingly incorporating chicken paws into processed food products such as snacks, ready meals, and specialty dishes. This trend is supported by advancements in food technology and the growing demand for innovative and convenient food solutions. Retail consumption is also on the rise, particularly in urban areas where consumers have greater access to frozen food products and modern retail infrastructure. Changing lifestyles, increasing disposable incomes, and a growing preference for convenient cooking options are key factors driving this segment.

Freezing Technology Insights

Individually Quick Frozen (IQF) technology dominates the market with an estimated 58% share. This technology is widely preferred due to its ability to preserve the texture, flavor, and nutritional value of chicken paws while preventing clumping. IQF products are easier to handle, store, and portion, making them highly suitable for both foodservice and retail applications. The leading segment driver is the increasing demand for high-quality frozen products that meet international standards and offer extended shelf life.Block freezing, while still relevant in cost-sensitive markets, is gradually losing share to more advanced freezing methods. Block-frozen products are typically less convenient to handle and may compromise product quality due to uneven freezing. However, they remain a viable option for bulk buyers who prioritize cost over convenience. As technological advancements continue to improve the efficiency and affordability of IQF systems, the adoption of this technology is expected to increase further, reinforcing its dominant position in the market.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Chicken Paws Market Segmentations

By Product Type

- Whole Chicken Paws

- Trimmed Chicken Paws

- Blanched Chicken Paws

- Marinated / Pre-seasoned Chicken Paws

By Processing Level

- Raw Frozen

- Semi-Processed Frozen

- Fully Processed / Ready-to-Cook

By Distribution Channel

- Direct Export / B2B Trade

- Foodservice Distributors

- Wholesale Markets

- Retail

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global frozen chicken paws market, accounting for approximately 62% of the market share in 2025. The region’s leadership is primarily driven by strong cultural preferences for chicken paws, particularly in countries such as China, Vietnam, and the Philippines. China represents the largest consumer market, where chicken paws are considered a delicacy and are widely used in traditional cuisine. The regional growth is further supported by rapid urbanization, rising disposable incomes, and the expansion of the foodservice sector. Additionally, the presence of well-established processing hubs in countries like Vietnam and Thailand enhances the region’s capacity to import, process, and redistribute chicken paws. Government support for food processing industries, improving cold chain infrastructure, and increasing demand for convenience foods are key drivers contributing to sustained growth in this region.

Latin America

Latin America holds approximately 18% of the global market share, with Brazil emerging as a dominant player in the export landscape. The region benefits from abundant poultry resources, favorable climatic conditions, and highly efficient production systems. Brazil, in particular, has developed a मजबूत export infrastructure and maintains strong trade relationships with major importing countries in Asia. Regional growth is driven by increasing investments in poultry farming, advancements in processing technologies, and competitive pricing strategies. Additionally, supportive government policies and trade agreements are facilitating market expansion. The ability of Latin American exporters to meet international quality standards while maintaining cost efficiency positions the region as a critical supplier in the global market.

North America

North America accounts for around 10% of the global market, with the United States playing a key role as an exporter. The region’s growth is driven by its large-scale poultry production capacity and well-established supply chains. Export-oriented operations are supported by advanced processing facilities, stringent quality control measures, and strong logistics networks. Regional growth drivers include increasing demand from Asian markets, favorable trade agreements, and continuous improvements in cold chain infrastructure. Although domestic consumption of chicken paws is relatively limited, the region’s focus on export markets ensures its continued relevance in the global industry.

Europe

Europe represents a moderate share of the frozen chicken paws market, with countries such as the Netherlands and Poland focusing primarily on exports. The region’s growth is influenced by stringent food safety regulations and high standards for animal welfare, which can increase production costs. However, these factors also enhance the quality and reliability of European exports. Regional growth drivers include strong demand from international markets, technological advancements in processing, and increasing investments in sustainable production practices. While domestic consumption remains limited, Europe’s strategic position as a high-quality exporter supports its participation in the global market.

Middle East & Africa

The Middle East and Africa region is emerging as the fastest-growing market, with a projected CAGR exceeding 9%. Growth in this region is driven by rapid urbanization, population growth, and increasing demand for affordable protein sources. Countries such as Saudi Arabia and Nigeria are witnessing a surge in imports due to limited domestic production capacity and rising consumption needs. Expanding retail networks, improving cold storage infrastructure, and increasing awareness of frozen food products are further supporting market growth. Additionally, the diversification of import sources and the strengthening of trade relationships with major exporters are creating new opportunities for market expansion in this region.

Key Players in the Frozen Chicken Paws Market

- BRF S.A.

- JBS S.A.

- Tyson Foods, Inc.

- Pilgrim’s Pride Corporation

- Sanderson Farms, Inc.

- Perdue Farms

- Cargill, Incorporated

- Charoen Pokphand Foods

- Wen’s Food Group

- New Hope Liuhe Co., Ltd.

- Suguna Foods

- Venky’s (India) Limited

- Minerva Foods

- Marfrig Global Foods

- Industrias Bachoco