Frozen Breaded Chicken for Home Market Size

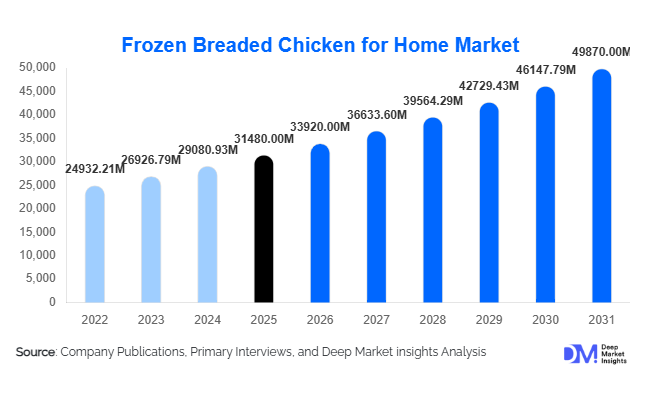

According to Deep Market Insights, the global frozen breaded chicken for home market size was valued at USD 31,480 million in 2025 and is projected to grow from USD 33,920 million in 2026 to reach USD 49,870 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). Market growth is supported by rising demand for convenient protein-based meals, increasing penetration of frozen food retail infrastructure, and changing consumer lifestyles favoring ready-to-cook and ready-to-heat products. Growing urbanization, dual-income households, and expansion of modern retail and e-commerce grocery platforms are accelerating adoption globally.

Key Market Insights

- Convenience-driven consumption patterns are reshaping home meal preparation, driving strong demand for frozen breaded chicken products.

- Air-fryer compatible and healthier formulations with reduced oil and clean-label coatings are gaining rapid traction.

- North America dominates global demand, supported by high frozen food penetration and strong retail cold-chain networks.

- Asia-Pacific is the fastest-growing region, fueled by expanding middle-class populations and modern retail growth.

- Private-label brands are expanding aggressively, increasing price competition and accessibility across supermarkets.

- Technological advancements in freezing and coating systems are improving texture retention and shelf life.

What are the latest trends in the frozen breaded chicken for home market?

Shift Toward Premium and Health-Oriented Frozen Foods

Consumers increasingly prefer high-protein, minimally processed frozen meals that combine convenience with nutrition. Manufacturers are launching products featuring whole-muscle chicken cuts, antibiotic-free sourcing, gluten-free breading, and reduced sodium coatings. Air-fryer optimization has emerged as a major innovation trend, enabling healthier cooking methods while maintaining crisp texture. Premiumization is evident through gourmet flavors, global seasoning profiles, and restaurant-style offerings tailored for home consumption.

Expansion of Direct-to-Consumer and Online Grocery Channels

E-commerce grocery platforms and quick-commerce delivery models are transforming frozen food accessibility. Online retail allows broader product assortment visibility and supports impulse purchasing through bundled meal solutions. Subscription-based frozen meal kits and digital promotions are improving repeat purchase behavior. Improved last-mile cold-chain logistics and insulated packaging technologies are enabling safe frozen deliveries even in emerging markets.

What are the key drivers in the frozen breaded chicken for home market?

Rising Demand for Convenient Home Meal Solutions

Busy urban lifestyles and time constraints are driving consumers toward ready-to-cook protein products. Frozen breaded chicken offers minimal preparation time while maintaining taste consistency. Increasing work-from-home and hybrid lifestyles have further boosted at-home consumption occasions, strengthening retail demand globally.

Expansion of Organized Retail and Cold Chain Infrastructure

Supermarkets, hypermarkets, and modern convenience stores are expanding freezer capacity worldwide. Investments in refrigeration logistics and warehouse automation have reduced spoilage risks and enabled wider distribution. Emerging economies are witnessing rapid frozen category penetration as retail modernization improves product availability.

Growth in Poultry Consumption as Affordable Protein

Chicken remains one of the most affordable and widely accepted animal proteins globally. Compared to red meat, poultry aligns with health-conscious dietary trends, encouraging sustained demand growth. Breaded formats further enhance taste appeal among families and younger consumers.

What are the restraints for the global market?

Volatility in Poultry and Grain Prices

Feed costs linked to corn and soybean price fluctuations directly impact poultry production expenses. Price instability pressures manufacturer margins and leads to periodic retail price increases, affecting consumer affordability in price-sensitive markets.

Health Perception Challenges

Despite convenience advantages, some consumers associate breaded frozen products with high sodium and processed food concerns. Regulatory scrutiny regarding nutritional labeling and additives requires continuous reformulation investments by manufacturers.

What are the key opportunities in the frozen breaded chicken industry?

Emerging Market Retail Expansion

Rapid urbanization across Southeast Asia, Latin America, and the Middle East is expanding frozen food consumption. Governments investing in food logistics infrastructure are enabling deeper market penetration. New entrants can capture growth through localized flavor offerings tailored to regional cuisines.

Technology Integration in Processing and Freezing

Advanced Individual Quick Freezing (IQF) systems and automated coating technologies improve texture preservation and production efficiency. Smart manufacturing and AI-enabled quality control systems reduce waste and enhance product consistency, creating competitive differentiation.

Clean-Label and Functional Product Innovation

Opportunities exist in developing organic, plant-fed poultry variants and high-protein functional meals targeting health-conscious consumers. Fortified coatings, alternative grains, and allergen-free formulations are expected to expand consumer reach.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 31480 Million |

| Market Size in 2026 | USD 33920 Million |

| Market Size in 2031 | USD 49870 Million |

| CAGR | 8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen breaded chicken products market demonstrates strong diversification across product categories; however, chicken nuggets continue to represent the dominant product segment, accounting for approximately 28% of the global market in 2025. The leadership of chicken nuggets is primarily supported by their universal consumer appeal, standardized portion sizes, affordability, and adaptability across multiple consumption occasions ranging from children’s meals to quick snacks and casual dining solutions. Their compatibility with air fryers, ovens, and microwave preparation further enhances convenience, aligning closely with modern household cooking behaviors that prioritize speed and minimal preparation effort. Additionally, strong penetration within quick-service restaurant (QSR) menus reinforces brand familiarity, which translates into sustained retail demand as consumers seek restaurant-style experiences at home.Stuffed and specialty chicken products, including cheese-filled or sauce-infused variants, represent an emerging premium niche targeting consumers seeking complete meal solutions with minimal preparation requirements. These products benefit from innovation in freezing technologies that preserve texture and flavor integrity while delivering restaurant-quality outcomes. As consumers increasingly prioritize experiential eating at home, specialty products are expected to capture higher value growth despite comparatively smaller volume shares.

Coating Type Insights

Coating technology remains a critical differentiator within the frozen breaded chicken market, directly influencing texture, flavor retention, and consumer perception of quality. Traditional breadcrumb coatings dominate the category, accounting for nearly 46% market share, largely due to their cost efficiency, manufacturing scalability, and longstanding consumer familiarity. Breadcrumb coatings provide consistent crispness and reliable cooking performance across preparation methods, making them highly attractive for mass-market distribution.The leading segment driver within coating types is the balance between sensory appeal and production efficiency offered by conventional breadcrumb systems. These coatings allow manufacturers to maintain competitive pricing while delivering expected taste and texture characteristics. Their adaptability across multiple product formats, including nuggets, patties, and tenders, further reinforces widespread adoption.Gluten-free and alternative grain coatings represent the fastest-growing niche segment, reflecting structural changes in dietary preferences and allergen awareness. Coatings made from rice flour, cornmeal, chickpea flour, and other alternative grains address growing demand among consumers managing gluten sensitivities or pursuing lifestyle-based dietary choices. Although still representing a smaller share of total volume, this segment commands higher price premiums and demonstrates strong growth potential due to increasing demand for inclusive food products. Innovation in plant-based binders and clean-label ingredients continues to improve texture performance, enabling broader market adoption.

Distribution Channel Insights

Distribution dynamics play a pivotal role in shaping market expansion, with supermarkets and hypermarkets accounting for approximately 52% of global sales. Their dominance stems from extensive freezer infrastructure, wide product assortment, and aggressive promotional pricing strategies that encourage bulk purchases. Large-format retail environments allow consumers to compare brands easily while benefiting from bundled offers and loyalty programs, which significantly influence purchasing decisions.The leading segment driver for this channel is the ability to combine product visibility with cold-chain reliability, ensuring product freshness and consistent availability. Retailers increasingly allocate dedicated frozen food sections that highlight convenience-oriented products, reinforcing impulse purchasing behavior. Private-label expansion within supermarkets further strengthens competitiveness by offering lower-cost alternatives while maintaining acceptable quality standards.Discount retailers and value-oriented chains are gaining share through competitive pricing strategies, particularly during periods of economic uncertainty. Frozen breaded chicken products align well with value-seeking behavior due to long shelf life and meal versatility. Expansion of private-label portfolios within discount channels continues to intensify price competition while broadening consumer access across emerging markets.

End-Use Insights

Household consumption represents nearly 72% of total global demand, making it the dominant end-use segment. The leading segment driver is the growing reliance on convenient meal solutions that reduce cooking time without sacrificing taste or protein intake. Frozen breaded chicken products offer predictable preparation outcomes, making them attractive for busy households balancing work schedules and family responsibilities.Dual-income households and urban consumers represent the fastest-growing demographic groups within this segment. Increasing workforce participation and longer commuting times encourage reliance on ready-to-cook foods that simplify meal preparation. Additionally, the growing popularity of air fryers has significantly enhanced at-home consumption by improving texture quality while reducing oil usage, reinforcing perceptions of healthier indulgence.Growth in frozen ready-meal ecosystems further amplifies household consumption volumes. Breaded chicken products frequently serve as core protein components within multi-item meal kits, strengthening cross-category integration with frozen vegetables, sauces, and bakery items. As consumers increasingly view frozen foods as reliable meal solutions rather than emergency purchases, long-term demand stability continues to improve.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Breaded Chicken for Home Market Segmentations

By Product Type

- Chicken Nuggets

- Chicken Tenders & Strips

- Breaded Chicken Patties

- Popcorn Chicken & Bites

- Stuffed & Specialty Breaded Chicken

By Coating Type

- Traditional Breadcrumb Coating

- Panko Coating

- Batter-Based Coating

- Gluten-Free & Alternative Grain Coating

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Grocery & E-commerce Platforms

- Discount Retailers & Warehouse Clubs

- Direct-to-Consumer (D2C) Channels

By End Use

- Household Consumption

- Family Meal Preparation

- Snacking & Quick Meals

- Home Party & Occasion Consumption

Regional Insights

North America

North America held approximately 34% of the global market in 2025, making it the largest regional market. The United States dominates regional consumption, supported by deeply entrenched frozen food culture, advanced cold-chain logistics, and strong retail penetration. High per-capita poultry consumption combined with widespread acceptance of convenience foods sustains consistent demand across both retail and foodservice channels.Regional growth is primarily driven by continuous product innovation, including healthier formulations, reduced-sodium variants, and premium coating technologies. Strong private-label adoption across major retailers enables competitive pricing, encouraging volume expansion even during inflationary periods. The popularity of air fryer cooking appliances has significantly revitalized frozen chicken categories, as consumers achieve restaurant-quality crispiness at home. Additionally, well-established quick-service restaurant ecosystems reinforce consumer familiarity with breaded chicken products, indirectly supporting retail sales growth.

Europe

Europe accounts for nearly 26% of global market share, with strong consumption across the United Kingdom, Germany, and France. The region demonstrates increasing consumer preference for premium, organic, and ethically sourced poultry products. European buyers place significant emphasis on animal welfare standards, traceability, and ingredient transparency, shaping product innovation strategies among manufacturers.Regional growth drivers include stringent labeling regulations that encourage cleaner formulations and reduced additive usage, fostering consumer trust. Expansion of private-label premium ranges within European supermarkets is accelerating adoption of higher-value frozen products. Additionally, busy urban lifestyles and smaller household sizes are increasing demand for portion-controlled frozen meal components. The rapid expansion of discount grocery chains across Europe further enhances accessibility, supporting steady market growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by China, India, Japan, and South Korea. Rising disposable incomes, accelerating urbanization, and modernization of retail infrastructure are transforming dietary habits across the region. Increasing exposure to Western-style fast food and international cuisine is encouraging adoption of breaded chicken products as convenient protein options.China leads regional consumption volume due to its large population base and expanding cold storage capacity. India is projected to record the fastest CAGR exceeding 10%, supported by rapid supermarket expansion, growth in online grocery platforms, and increasing demand among younger urban consumers. Japan and South Korea contribute through strong convenience-store cultures that emphasize ready-to-eat and easy-to-prepare meals. Improvements in cold-chain logistics and domestic poultry processing investments further support long-term regional expansion.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth supported by high poultry consumption levels and increasing reliance on frozen imports. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa represent key demand centers due to rising urban populations and expanding modern retail infrastructure.Regional growth drivers include limited local poultry processing capacity in several markets, which increases dependence on imported frozen products. Rapid expansion of supermarket chains and shopping malls enhances product availability, while rising tourism and foodservice activity stimulate demand across hospitality sectors. Younger populations and growing acceptance of Western dining formats further accelerate adoption, particularly among urban consumers seeking convenient meal solutions.

Latin America

Latin America demonstrates strong growth potential, led by Brazil and Mexico. Brazil’s extensive poultry production infrastructure positions the country as both a major consumer and a significant exporter within the global frozen chicken supply chain. Export-oriented processing facilities contribute substantially to international trade volumes while supporting domestic product innovation.Regional growth is driven by rising middle-class populations, improving cold-chain logistics, and increasing adoption of frozen convenience foods among urban households. Economic volatility encourages consumers to seek affordable protein sources with long shelf life, benefiting frozen breaded chicken products. Expansion of modern retail formats and private-label penetration continues to strengthen accessibility, enabling sustained market expansion across the region.

Key Players in the Frozen Breaded Chicken for Home Market

- Tyson Foods Inc.

- Pilgrim’s Pride Corporation

- BRF S.A.

- Perdue Farms Inc.

- Sanderson Farms (now integrated under major poultry operations)

- Cargill Incorporated

- JBS S.A.

- Hormel Foods Corporation

- Foster Farms

- OSI Group

- Wayne-Sanderson Farms

- CP Foods (Charoen Pokphand Foods)

- NH Foods Ltd.

- Moy Park (Pilgrim’s Pride Europe operations)

- Marfrig Global Foods