Frozen Bakery Market Size

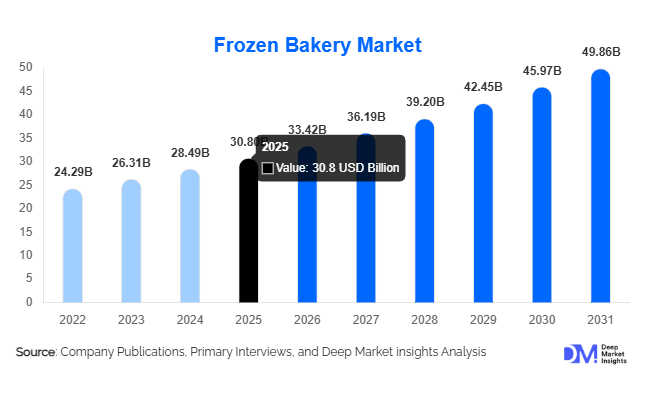

According to Deep Market Insights, the global frozen bakery market size was valued at USD 30.8 billion in 2025 and is projected to grow from USD 33.42 billion in 2026 to reach USD 49.86 billion by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). Market expansion is primarily supported by rising demand for convenience foods, rapid growth of quick-service restaurants (QSRs), increasing urban lifestyles, and technological advancements in freezing and cold-chain logistics. The adoption of frozen bakery products across retail, foodservice, and institutional channels has accelerated globally as consumers increasingly seek ready-to-bake and ready-to-eat solutions without compromising freshness and quality.

Key Market Insights

- Convenience-led consumption patterns are driving strong adoption of frozen bread, pastries, and bakery snacks across urban households globally.

- Foodservice and QSR expansion remains the largest demand contributor, particularly in North America, Europe, and Asia-Pacific.

- Technological innovations in blast freezing and IQF technologies are improving shelf life while preserving texture and flavor quality.

- Private-label frozen bakery products are gaining traction across supermarkets and hypermarkets due to competitive pricing.

- Asia-Pacific is the fastest-growing regional market, supported by westernized diets and expanding cold storage infrastructure.

- Automation in bakery manufacturing is improving scalability and reducing operational costs for large producers.

What are the latest trends in the frozen bakery market?

Rise of Ready-to-Bake Premium Products

Consumers increasingly prefer bakery-quality products prepared at home, driving demand for ready-to-bake frozen dough, artisan breads, and premium pastries. Retailers are expanding offerings such as sourdough loaves, croissants, and specialty desserts that replicate in-store bakery freshness. Premiumization is becoming a major trend, with manufacturers introducing clean-label formulations, organic ingredients, and preservative-free frozen products. This shift aligns with consumer expectations for convenience combined with authenticity and artisanal quality.

Expansion of Cold Chain and E-commerce Distribution

Improved refrigerated logistics and last-mile cold-chain delivery are enabling frozen bakery penetration into emerging markets. Online grocery platforms now offer frozen bakery assortments with reliable temperature-controlled delivery. Subscription-based meal kits and frozen breakfast solutions are expanding product accessibility. Digital retail channels are reshaping purchasing behavior, especially among younger urban consumers seeking convenience-driven food solutions.

What are the key drivers in the frozen bakery market?

Growth of Quick-Service Restaurants and Cafés

The rapid global expansion of café chains, bakeries, and QSR outlets has significantly increased demand for standardized frozen bakery inputs. Frozen dough and par-baked products allow foodservice operators to ensure consistent quality while minimizing labor and preparation time. Chains benefit from centralized production, reduced wastage, and improved operational efficiency, making frozen bakery products essential to modern foodservice supply chains.

Changing Consumer Lifestyles and Urbanization

Rising urban populations and dual-income households have increased reliance on convenient food options. Frozen bakery products offer longer shelf life and minimal preparation time, making them ideal for fast-paced lifestyles. Breakfast-on-the-go culture and growing snack consumption trends further contribute to rising global demand.

Advancements in Freezing Technologies

Innovations such as individual quick freezing (IQF), cryogenic freezing, and improved packaging technologies are enhancing product quality and extending shelf stability. These technologies maintain moisture retention, texture integrity, and flavor consistency, helping frozen bakery products compete directly with freshly baked alternatives.

What are the restraints for the global market?

Cold Chain Infrastructure Costs

Frozen bakery distribution depends heavily on refrigerated storage and transportation systems. Developing economies face challenges due to high infrastructure investment requirements, electricity costs, and logistics inefficiencies, which may restrict market penetration in rural or semi-urban regions.

Health and Clean-Label Concerns

Consumers increasingly scrutinize processed food ingredients, including preservatives and additives historically associated with frozen foods. Manufacturers must invest in reformulation and clean-label innovation to maintain consumer trust and comply with evolving regulatory standards.

What are the key opportunities in the frozen bakery industry?

Emerging Market Expansion

Rapid urbanization across Asia-Pacific, Latin America, and parts of Africa presents strong opportunities for frozen bakery manufacturers. Rising middle-class income and supermarket expansion are enabling wider adoption of frozen foods. Governments supporting modern retail infrastructure and food processing investments are accelerating market entry opportunities for global producers.

Plant-Based and Health-Focused Bakery Innovation

The growing popularity of vegan, gluten-free, and high-protein diets presents new product development avenues. Manufacturers introducing functional bakery products enriched with fiber, plant protein, and reduced sugar formulations can attract health-conscious consumers while maintaining convenience advantages.

Automation and Smart Manufacturing

Industry participants are investing in automated production lines and AI-driven demand forecasting to optimize inventory management and reduce waste. Smart factories enable large-scale production with consistent quality, helping companies expand global exports while improving margins.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 30.8 Billion |

| Market Size in 2026 | USD 33.42 Billion |

| Market Size in 2031 | USD 49.86 Billion |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen bakery market demonstrates strong product diversification, with frozen bread maintaining its position as the dominant category, accounting for approximately 34% of the global frozen bakery market in 2025. The leadership of frozen bread is primarily driven by its widespread consumption across both foodservice and household segments, where consistency, extended shelf life, and operational efficiency remain critical purchasing considerations. Foodservice operators, including quick-service restaurants (QSRs), sandwich chains, and institutional kitchens, increasingly rely on frozen bread products to maintain uniform quality while minimizing labor dependency and ingredient wastage. The ability of frozen bread to be partially baked, stored, and finished on demand aligns with modern operational models focused on speed and efficiency. Additionally, advancements in freezing technologies such as individual quick freezing (IQF) and improved fermentation preservation techniques have enhanced texture retention and flavor quality, narrowing the perceived gap between fresh and frozen bakery offerings.Ready-to-bake dough products are emerging as one of the fastest-growing categories within the frozen bakery landscape. These products cater directly to consumers seeking freshly baked experiences at home without the technical expertise or time commitment associated with traditional baking. The primary growth driver lies in experiential consumption, where baking becomes both a convenience solution and a leisure activity. Technological improvements in freezing and packaging now allow dough to maintain fermentation quality, ensuring bakery-style results. As remote work and home-centered lifestyles continue to influence consumer behavior, ready-to-bake formats are expected to witness sustained adoption across global markets.

Application Insights

Foodservice applications dominate frozen bakery consumption, contributing nearly 48% of total demand in 2025. The leadership of this segment is driven by the operational advantages frozen bakery products provide to restaurants, cafés, hotels, and quick-service chains. Consistency in taste and appearance across multiple outlets remains a critical requirement for large foodservice operators, and frozen bakery solutions enable centralized production with standardized quality outcomes. Rising labor costs and workforce shortages across hospitality markets further reinforce adoption, as frozen products significantly reduce preparation time and skill dependency. Additionally, menu diversification trends encourage operators to frequently introduce new bakery items without investing in specialized baking infrastructure.Institutional demand from airlines, educational institutions, healthcare facilities, and corporate catering providers is gaining importance as standardized meal planning becomes essential for cost management and operational efficiency. Frozen bakery products allow institutions to maintain predictable portion control, hygiene standards, and supply stability. Airlines, in particular, benefit from frozen bakery solutions that maintain product integrity during long storage and reheating cycles. Healthcare and education sectors increasingly adopt frozen bakery items due to nutritional customization capabilities and simplified logistics management.

Distribution Channel Insights

Supermarkets and hypermarkets account for the largest distribution share at approximately 41% of global sales, supported by extensive product assortments and strong private-label penetration. Large retail chains leverage frozen bakery products to expand value-added offerings while maintaining competitive pricing structures. The leading driver for this channel is consumer trust in organized retail environments, where consistent availability, promotional pricing, and dedicated frozen sections encourage bulk purchasing behavior. Retailers also benefit from frozen bakery products’ longer shelf stability, which reduces inventory losses compared to fresh bakery alternatives.Online retail is emerging as the fastest-growing distribution segment, fueled by advancements in cold-chain logistics and increasing consumer adoption of digital grocery platforms. Improvements in last-mile delivery infrastructure and temperature-controlled packaging have enabled frozen bakery products to reach consumers without compromising quality. The leading growth driver for online channels is convenience combined with wider product access, allowing consumers to explore premium and international bakery offerings previously unavailable in local stores. Subscription-based grocery services and app-driven purchasing behavior further accelerate market expansion.

End-Use Insights

Commercial foodservice operators represent the largest end-use segment, supported by the continuous expansion of café chains, bakery franchises, and quick-service restaurant networks worldwide. Frozen bakery products enable scalable operations by simplifying kitchen workflows and ensuring uniform product quality regardless of location. The primary driver of this segment is operational efficiency, as businesses seek solutions that reduce labor intensity while maintaining customer satisfaction. The growth of takeaway and delivery-focused dining models further strengthens demand for products that can be prepared quickly without compromising taste or presentation.Industrial end users, including airline catering companies, hospitality groups, and large-scale catering services, are adopting frozen bakery products to maintain consistency across multiple service points. These organizations benefit from predictable supply cycles, standardized recipes, and reduced food waste. The integration of frozen bakery solutions into centralized production systems supports cost optimization and ensures compliance with strict food safety standards across international operations.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Bakery Market Segmentations

By Product Type

- Frozen Bread

- Frozen Cakes & Pastries

- Frozen Viennoiserie

- Frozen Pizza & Pizza Crusts

- Frozen Savory Bakery Snacks

- Frozen Dough & Part-Baked Products

- Gluten-Free & Specialty Frozen Bakery Products

By Distribution Channel

- Foodservice & HoReCa Distribution

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer (D2C)

- Wholesale & Institutional Supply

By End Use

- Quick-Service Restaurants (QSRs)

- Full-Service Restaurants & Cafés

- Hotels & Catering Services

- Retail Household Consumption

- Institutional Buyers (Airlines, Schools, Hospitals)

By Technology Type

- Fully Baked Frozen Products

- Partially Baked (Par-Baked)

- Ready-to-Proof Products

- Raw Frozen Dough

Regional Insights

North America

North America accounted for nearly 32% of the global frozen bakery market in 2025, led predominantly by the United States, where frozen food consumption is deeply embedded in consumer purchasing behavior. The region’s mature cold-chain infrastructure, widespread freezer ownership, and strong presence of large-scale foodservice chains create a highly favorable environment for frozen bakery adoption. A key regional growth driver is the increasing demand for convenience-oriented meal solutions among working professionals and smaller households seeking time-efficient food preparation. Canada contributes steady growth through expanding retail networks and rising demand for premium and artisanal frozen bakery products. Additionally, innovation in health-focused offerings such as gluten-free and high-protein bakery items supports market expansion across North America.

Europe

Europe holds approximately 29% market share, supported by its long-standing bakery traditions and advanced food manufacturing ecosystem. Countries such as Germany, France, Italy, and the United Kingdom demonstrate strong adoption of par-baked bread and artisan frozen pastries across both retail and foodservice sectors. The leading regional driver is the integration of frozen technology into traditional bakery craftsmanship, allowing producers to preserve authenticity while achieving scalable distribution. European consumers increasingly value premium quality and authenticity, encouraging manufacturers to develop high-quality frozen alternatives that replicate fresh bakery experiences. Cross-border trade within the region and strong export capabilities further strengthen Europe’s position as a global production hub.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, projected to expand at a CAGR exceeding 10% through 2031. Rapid urbanization, rising disposable incomes, and westernization of dietary habits significantly influence market growth across China, Japan, India, and South Korea. The primary regional growth driver is the expansion of international QSR and café chains, which introduce standardized bakery menus requiring frozen product supply. Improvements in refrigeration infrastructure and increasing penetration of modern retail formats further accelerate adoption. India is emerging as a key consumption hub due to expanding urban retail penetration, growing middle-class populations, and rising demand for convenient breakfast and snack options. Younger consumers increasingly embrace bakery products as everyday meals rather than occasional indulgences, supporting sustained long-term growth.

Latin America

Latin America is experiencing steady expansion led by Brazil and Mexico, where modern retail development and urbanization trends are reshaping food consumption patterns. The leading regional growth driver is the increasing participation of women in the workforce, which elevates demand for convenient meal solutions that reduce preparation time. Rising investment in cold storage infrastructure and supermarket expansion improves product accessibility across urban centers. Additionally, growing exposure to international food trends and expanding foodservice industries encourage adoption of frozen bakery offerings, particularly bread and dessert categories.

Middle East & Africa

The Middle East & Africa region is witnessing accelerating adoption of frozen bakery products, with the UAE, Saudi Arabia, and South Africa emerging as key growth markets. Tourism-driven hospitality sectors and expanding café cultures significantly influence regional demand, as hotels and restaurants require consistent, high-quality bakery solutions capable of supporting large visitor volumes. The primary growth driver in this region is the rapid expansion of premium hospitality and foodservice infrastructure supported by economic diversification initiatives. Rising expatriate populations and increasing exposure to global food trends further stimulate demand for pastries, desserts, and specialty bakery items. Investments in cold-chain logistics and organized retail development continue to improve distribution efficiency, enabling broader market penetration across urban and semi-urban areas.

Key Players in the Frozen Bakery Market

- Grupo Bimbo S.A.B. de C.V.

- General Mills Inc.

- ARYZTA AG

- Lantmännen Unibake

- Associated British Foods plc

- Conagra Brands Inc.

- Flowers Foods Inc.

- Europastry S.A.

- Vandemoortele NV

- Bridgford Foods Corporation

- Premier Foods plc

- Finsbury Food Group plc

- Gonnella Baking Company

- Rich Products Corporation

- CSM Ingredients Group