Fresh Broccoli Market Size

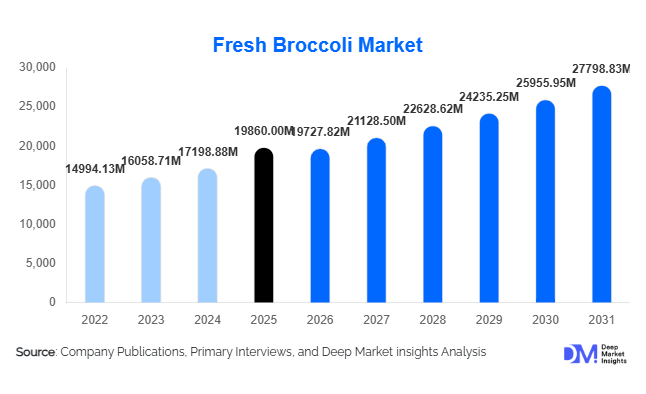

According to Deep Market Insights, the global fresh broccoli market size was valued at USD 18,420 million in 2025 and is projected to grow from USD 19,860 million in 2026 to reach USD 27,798.83 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). Market growth is primarily driven by rising global consumption of nutrient-dense vegetables, increasing adoption of plant-forward diets, and expanding retail distribution networks that enhance year-round availability of fresh produce. Growing consumer awareness regarding immunity, digestive health, and functional nutrition continues to strengthen demand for broccoli across both developed and emerging economies.

Key Market Insights

- Health-focused consumption patterns are accelerating broccoli demand due to its association with antioxidants, fiber, and vitamin-rich diets.

- Modern retail expansion and cold-chain logistics are enabling consistent supply across urban markets worldwide.

- Asia-Pacific dominates production and consumption, led by China and India’s large agricultural base.

- Convenience-driven fresh-cut and ready-to-cook formats are emerging as high-growth product categories.

- Foodservice recovery and healthy menu innovation are boosting institutional demand globally.

- Sustainable farming and precision agriculture adoption are improving yields and reducing supply volatility.

What are the latest trends in the fresh broccoli market?

Rise of Functional and Immunity-Focused Diets

Consumers increasingly associate fresh vegetables with preventive healthcare, driving sustained demand for broccoli due to its high vitamin C, fiber, and antioxidant content. Retailers are marketing broccoli as a “superfood vegetable,” aligning with broader wellness trends and plant-based eating habits. Demand is particularly strong among urban consumers seeking low-calorie and nutrient-dense meal ingredients. The integration of broccoli into meal kits, smoothies, and ready-to-cook vegetable mixes further strengthens retail penetration. Health campaigns promoting vegetable consumption and government-backed nutrition programs are reinforcing long-term demand stability.

Expansion of Fresh-Cut and Value-Added Produce

Fresh-cut broccoli florets, microwave-ready packs, and pre-washed packaging formats are transforming purchasing behavior. Time-constrained consumers increasingly prefer convenience-based vegetables that reduce preparation effort. Retail chains and food processors are investing in automated cutting, sorting, and packaging systems to improve shelf life and reduce waste. Modified atmosphere packaging technologies are extending freshness, enabling cross-border trade and expanding supermarket distribution. This trend is particularly strong in North America and Europe, where convenience-oriented consumption patterns dominate.

What are the key drivers in the fresh broccoli market?

Growing Global Shift Toward Healthy Diets

The increasing prevalence of lifestyle diseases such as obesity and diabetes has encouraged consumers to adopt vegetable-rich diets. Broccoli’s strong nutritional profile positions it as a staple ingredient in health-conscious meal planning. Governments and healthcare organizations promoting balanced nutrition are indirectly supporting market expansion. Rising vegan and flexitarian populations further accelerate vegetable consumption trends globally.

Expansion of Organized Retail and Cold Chain Infrastructure

Investment in refrigerated logistics, storage facilities, and supply chain modernization has significantly improved the availability of fresh broccoli throughout the year. Emerging markets are witnessing rapid supermarket penetration, allowing farmers to access larger consumer bases. Efficient cold chains reduce spoilage losses, increase export viability, and stabilize prices across seasons.

Foodservice and Quick-Service Restaurant Adoption

Restaurants and institutional catering services increasingly incorporate broccoli into menus due to its versatility and nutritional positioning. Growth of healthy fast-casual dining formats and meal subscription services is driving consistent bulk demand. Broccoli’s compatibility with multiple cuisines enhances adoption across global foodservice markets.

What are the restraints for the global market?

Price Volatility and Weather Dependency

Broccoli cultivation is sensitive to temperature fluctuations and water availability. Climate variability, drought conditions, and pest outbreaks can significantly impact yields, causing supply instability and price fluctuations. Producers face challenges maintaining consistent production volumes amid changing climatic conditions.

Post-Harvest Losses and Shelf-Life Constraints

Fresh broccoli has limited shelf life compared with processed vegetables, leading to high wastage during transportation and retail handling. Developing regions with inadequate cold storage infrastructure experience higher losses, limiting profitability for growers and distributors.

What are the key opportunities in the fresh broccoli industry?

Expansion in Emerging Urban Markets

Rapid urbanization in Asia, Latin America, and Africa presents significant growth opportunities. Rising disposable incomes and increasing supermarket penetration are enabling consumers to purchase premium fresh vegetables regularly. Governments encouraging vegetable cultivation and nutritional security programs further support demand growth.

Technology Integration in Farming

Precision agriculture technologies, including sensor-based irrigation and AI-powered crop monitoring, are improving yield predictability and reducing input costs. Adoption of greenhouse cultivation and climate-controlled farming allows year-round production, reducing seasonal supply gaps and stabilizing pricing structures.

Export-Oriented Production Growth

Countries with strong agricultural capabilities are expanding exports to meet rising demand in Europe and North America. Improved phytosanitary standards, packaging innovation, and logistics optimization enable exporters to access premium markets. Export diversification reduces dependency on domestic demand cycles while increasing farmer income stability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 19860 Million |

| Market Size in 2026 | USD 19727.82 Million |

| Market Size in 2031 | USD 27798.83 Million |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Calabrese broccoli continues to dominate the global broccoli market, representing an estimated 61% of market share in 2025. This dominance is largely fueled by its widespread culinary acceptance, versatility across various cuisines, and higher agricultural yields compared to specialty broccoli varieties. Its adaptability to diverse climatic conditions and efficient harvesting processes have also contributed to sustained production growth. Concurrently, premium varieties such as Tenderstem and sprouting broccoli are witnessing increased consumer interest, particularly within higher-end retail and health-conscious segments. These varieties are often perceived as superior in taste, texture, and nutritional value, with Tenderstem broccoli being favored for its tender stalks and uniform florets that appeal to gourmet cooking. Organic broccoli is emerging as the fastest-growing segment within the product type category, propelled by the rising consumer preference for chemical-free produce. Growing awareness of the environmental impact of conventional agriculture, coupled with sustainability certifications, has bolstered organic cultivation, allowing producers to command higher price points in both developed and emerging markets.

Application Insights

The household consumption segment remains the largest contributor to global broccoli demand, accounting for nearly 54% of the market in 2025. This trend is underpinned by increasing health consciousness, where consumers are incorporating nutrient-dense vegetables into daily meals to support immunity and overall wellness. Broccoli's rich profile of vitamins, minerals, and dietary fiber aligns with growing consumer awareness about disease prevention and healthy eating. The foodservice sector is expanding steadily, capturing a roughly 29% market share, as restaurants, hotels, and cafes integrate vegetable-forward dishes to cater to evolving consumer preferences for wholesome, fresh, and visually appealing meals. In particular, health-focused quick-service restaurants (QSRs) and premium casual dining establishments are standardizing broccoli-based menu items, thereby driving bulk procurement from distributors. Meanwhile, the food processing application, including frozen vegetable mixes, ready-to-eat meals, and snack formulations, is experiencing robust growth. Manufacturers are increasingly leveraging broccoli as a globally accepted ingredient to enhance nutritional content while meeting the demand for convenient and time-saving meal solutions.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate broccoli distribution, holding nearly 46% market share in 2025. This leadership is largely due to the expansion of organized retail networks, which provide reliable cold storage infrastructure and streamlined supply chain management. The modern retail environment enables consistent product quality, standardized pricing, and promotional activities that encourage repeat purchases. Wholesale markets remain relevant, particularly for institutional buyers and traditional retailers, who rely on bulk procurement to meet high-volume demand. Online grocery platforms are emerging as a significant growth channel, fueled by increasing digital penetration, urban lifestyle changes, and rising consumer preference for home delivery. E-commerce allows consumers to access premium and organic broccoli varieties conveniently, bridging the gap between producers and urban households.

Farming Method Insights

Conventional farming continues to dominate global broccoli production, accounting for approximately 78% of output, due to cost efficiency, established supply chains, and scalability. Conventional methods remain the preferred choice for large-scale commercial growers who aim to meet mass-market demand efficiently. However, organic farming is witnessing the fastest growth rate, driven by regulatory frameworks promoting sustainable agriculture and increasing consumer willingness to pay premium prices for pesticide-free produce. Governments and agricultural organizations across Europe, North America, and Asia-Pacific are supporting organic cultivation through subsidies, technical training, and market access programs. This trend reflects the convergence of health consciousness, environmental awareness, and premium product positioning within the global broccoli market.

End-Use Industry Insights

Retail households continue to be the primary consumers of broccoli, benefiting from convenient availability and strong health messaging. Nevertheless, foodservice and food processing sectors are outpacing retail growth due to diversification of menu offerings and value-added processing. The rise of health-focused quick-service restaurants and meal kit providers has created a stable, predictable demand for broccoli, facilitating large-scale bulk procurement agreements. Processed food manufacturers are increasingly incorporating broccoli into frozen, ready-to-eat, and snack products, capitalizing on its nutrient density and long shelf life when processed appropriately. Export-driven demand has strengthened, particularly in Europe and North America, where off-season fresh vegetable supply is limited. Countries like Mexico, Egypt, and Spain have become vital suppliers, balancing regional demand and contributing to a more integrated global supply chain. The processed food industry's global valuation exceeding USD 2 trillion further supports the sustained utilization of broccoli, as manufacturers seek nutritious, versatile, and globally recognized ingredients to meet evolving consumer demands.

Explore more data points, trends and opportunities Download Free Sample Report

Fresh Broccoli Market Segmentations

By Product Type

- Conventional Fresh Broccoli

- Organic Fresh Broccoli

- Baby Broccoli / Tenderstem Broccoli

- Broccoli Crowns

- Whole Head Broccoli

- Pre-cut & Ready-to-Cook Broccoli

By Application

- Household Consumption

- Foodservice & HoReCa

- Food Processing Industry

- Institutional Catering

- Retail Fresh Produce Packs

By Distribution Channel

- Supermarkets & Hypermarkets

- Traditional Grocery Stores

- Online Grocery Platforms

- Wholesale & Agricultural Markets

- Direct Farm Sales & CSA Models

By Cultivation Method

- Open Field Farming

- Greenhouse Cultivation

- Hydroponic & Controlled Environment Farming

By End Use Industry

- Fresh Retail Consumption

- Quick Service Restaurants

- Frozen & Processed Food Manufacturers

- Meal Kit & Ready Meal Companies

Regional Insights

Asia-Pacific

Asia-Pacific is projected to maintain its dominance, accounting for approximately 48% of the global market in 2025. China remains the regional leader due to its vast agricultural base, widespread adoption of modern cultivation techniques, and strong domestic vegetable consumption patterns. Factors driving regional growth include urbanization, rising disposable incomes, and increasing awareness of healthy diets. India is witnessing a shift in dietary preferences, with urban consumers embracing vegetables like broccoli as part of balanced meals, supported by the expansion of organized retail chains and cold chain logistics. Japan and South Korea continue to focus on premium-quality imports, where taste, texture, and organic certifications drive purchase decisions. The increasing penetration of e-commerce platforms in these markets further supports accessibility, making broccoli available to a wider demographic while promoting premium and organic variants. Investments in post-harvest storage, efficient transport networks, and processing infrastructure are additional growth catalysts in the Asia-Pacific region.

North America

North America holds nearly 21% market share, with the United States leading consumption due to established health-centric diets and widespread incorporation of broccoli into everyday meals. High demand through retail chains, coupled with the growth of the foodservice sector, ensures consistent market expansion. Mexico plays a strategic role as an export-oriented producer, supplying fresh broccoli year-round to the U.S. market and capitalizing on trade agreements such as USMCA that facilitate cross-border vegetable trade. The growth drivers in North America include increasing consumer health awareness, the rising popularity of plant-based diets, and the adoption of organic and sustainably produced broccoli. Advanced farming technologies, such as precision agriculture and automated irrigation systems, are enhancing crop yields and quality, reinforcing North America's leadership in both production and consumption.

Europe

Europe represents roughly 19% of global broccoli demand, with major markets including the U.K., Germany, France, Italy, and Spain. Consumers in this region demonstrate strong preferences for organic and sustainably produced vegetables, which enables premium pricing opportunities for certified produce. Spain and other Mediterranean countries play a critical role in ensuring year-round supply through exports, particularly during off-season periods in northern Europe. Regional growth is further supported by government initiatives promoting healthy eating, subsidies for organic farming, and increasing retail penetration of fresh and ready-to-eat vegetables. Foodservice applications, especially in urban centers, are expanding as restaurants and catering services respond to the demand for nutritious and aesthetically appealing meals. Additionally, Europe’s well-developed logistics infrastructure and cold chain capabilities help maintain quality standards, which encourages greater broccoli consumption in both domestic and cross-border markets.

Middle East & Africa

The Middle East is experiencing rising broccoli demand, driven by rapid urbanization, increased health awareness, and expanding modern retail formats, particularly in the UAE and Saudi Arabia. Consumers in these markets increasingly prefer fresh, premium-quality vegetables, often sourced from local and imported supplies. Africa’s growth is primarily production-led, with countries such as Egypt and South Africa expanding cultivation to meet both domestic and export demand. Investments in irrigation infrastructure, agricultural technology, and processing facilities are strengthening the region’s ability to supply high-quality broccoli consistently. Export markets in the Middle East also act as a growth catalyst for African producers, creating opportunities for trade partnerships and capacity building. The increasing presence of organized retail chains and cold storage facilities is further enhancing market penetration and product accessibility.

Latin America

Latin America is emerging as a critical production hub, particularly in Mexico, Guatemala, and Peru, driven by favorable climatic conditions, agricultural expertise, and strong export orientation. Trade agreements with North America and Europe are accelerating regional growth by ensuring steady demand and favorable pricing for export-oriented producers. Investment in modern farming practices, post-harvest handling, and cold chain logistics is enhancing product quality and shelf life, making Latin America one of the fastest-growing supply regions globally. Domestic consumption is also rising in urban centers, supported by retail modernization and growing awareness of healthy diets. Leading segment drivers include the expansion of organic and high-yield broccoli varieties, which cater to both domestic health-conscious consumers and international markets seeking sustainable and premium produce.

Key Players in the Fresh Broccoli Market

- Dole Food Company, Inc.

- Fresh Del Monte Produce Inc.

- Bonduelle Group

- Green Giant (B&G Foods)

- Ocean Mist Farms

- Tanimura & Antle

- Mann Packing Co., Inc.

- Church Brothers Farms

- Vegpro International Inc.

- Taylor Farms

- Driscoll’s (Fresh Vegetable Division)

- Sakata Seed Corporation

- Agrovision Corp.

- Camposol Holding PLC

- Earthbound Farm