Fresh Berries Market Size

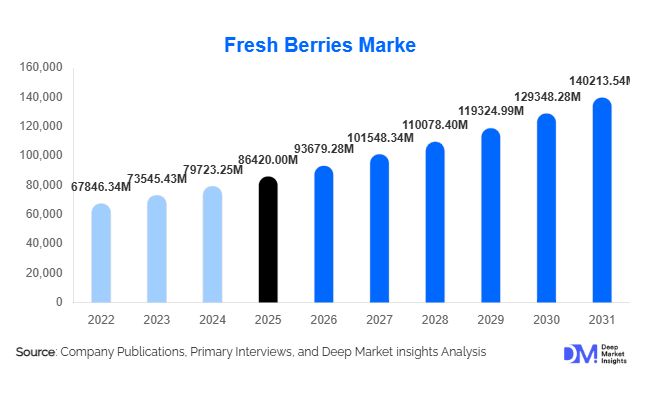

According to Deep Market Insights, the global fresh berries market size was valued at USD 86,420 million in 2025 and is projected to grow from USD 93,679.28 million in 2026 to reach USD 140,213.54 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The fresh berries market growth is primarily driven by increasing consumer preference for nutrient-dense foods, rising adoption of healthy snacking habits, expanding cold-chain logistics infrastructure, and strong retail penetration across both developed and emerging economies. Demand for blueberries, strawberries, raspberries, and blackberries continues to rise globally as consumers increasingly associate berries with immunity support, antioxidant intake, and functional nutrition. Additionally, year-round availability enabled by greenhouse cultivation, controlled-environment agriculture, and international trade networks has transformed berries from seasonal fruits into everyday dietary staples.

Key Market Insights

- Health-driven consumption trends are accelerating global berry demand due to high antioxidant and vitamin content.

- Blueberries and strawberries dominate global production and consumption, supported by large-scale commercial farming and export networks.

- Modern retail and e-commerce grocery platforms are improving accessibility and reducing post-harvest losses.

- Asia-Pacific is emerging as the fastest-growing consumption hub, driven by urbanization and premium fruit demand.

- Technological adoption in protected cultivation is enabling year-round production and improved yield stability.

- Export-oriented farming models in Latin America and Africa are reshaping global supply chains.

What are the latest trends in the fresh berries market?

Shift Toward Functional and Superfood Consumption

Fresh berries are increasingly positioned as functional foods due to their antioxidant properties, low calorie content, and association with heart health and cognitive wellness. Consumers are prioritizing fresh, minimally processed produce, pushing retailers to expand premium berry assortments. Marketing strategies emphasizing immunity, clean eating, and plant-based diets are strengthening berries’ perception as a daily wellness product rather than a luxury fruit. This trend is particularly strong among millennials and urban consumers seeking convenient yet healthy snack options.

Expansion of Controlled-Environment Agriculture

Greenhouse farming, hydroponics, and vertical agriculture are transforming berry cultivation. Producers are investing heavily in climate-controlled production systems that reduce weather dependency and extend harvesting seasons. Countries with limited arable land are increasingly adopting indoor berry cultivation technologies, improving productivity while minimizing water consumption and pesticide use. These advancements are stabilizing supply chains and enabling consistent quality standards required by global retailers.

What are the key drivers in the fresh berries market?

Growing Health Awareness and Nutritional Demand

Consumers worldwide are shifting toward diets rich in fruits with functional health benefits. Berries are widely recognized for high levels of antioxidants, fiber, and vitamins, making them central to preventive health nutrition. Rising incidences of lifestyle-related diseases have accelerated demand for natural foods perceived as healthier alternatives to processed snacks. Retail promotions and health-focused branding have further amplified adoption across households globally.

Expansion of Cold Chain and Global Trade Networks

Improvements in refrigerated transportation, packaging technology, and logistics infrastructure have significantly extended berry shelf life. This has enabled producers in Latin America and Africa to export fresh berries to North America, Europe, and Asia efficiently. Enhanced cold storage capacity has reduced spoilage rates and improved profitability for exporters, supporting consistent global supply throughout the year.

Retail Modernization and E-commerce Penetration

The growth of supermarket chains, premium grocery stores, and online food delivery platforms has made fresh berries widely accessible. Digital grocery platforms allow direct farm-to-consumer distribution, improving price transparency and freshness perception. Subscription fruit delivery models and rapid-commerce channels are further increasing consumption frequency.

What are the restraints for the global market?

High Production and Labor Costs

Berry cultivation remains labor-intensive due to delicate harvesting requirements. Rising labor wages and operational costs challenge profitability, particularly in developed markets. Producers are increasingly investing in automation technologies, but adoption remains gradual due to high upfront investment requirements.

Perishability and Supply Chain Vulnerability

Fresh berries are highly perishable, making the industry sensitive to transportation delays, climate disruptions, and storage inefficiencies. Price volatility caused by seasonal supply fluctuations and weather-related crop losses continues to act as a major restraint for market participants.

What are the key opportunities in the fresh berries industry?

Premium Organic and Sustainable Berry Production

Organic berries represent one of the fastest-growing opportunities, supported by consumer demand for pesticide-free produce. Governments are encouraging sustainable agriculture practices through subsidies and certification programs, enabling producers to command premium pricing and expand export opportunities.

Emerging Market Consumption Growth

Rapid urbanization and rising disposable incomes across Asia-Pacific, the Middle East, and Latin America are expanding demand for premium fruits. Increasing exposure to Western dietary patterns and modern retail formats is accelerating berry consumption in countries such as China, India, and the UAE.

Value-Added Packaging and Convenience Formats

Innovations in packaging such as resealable containers, snack-size portions, and biodegradable materials are improving consumer convenience while reducing food waste. Smart packaging technologies that extend freshness are creating additional growth avenues for producers and retailers.

Product Type Insights

The global berries market demonstrates strong diversification across product categories; however, strawberries continue to dominate the industry landscape, accounting for nearly 41% of the global market share in 2025. The leadership position of strawberries is primarily supported by their extensive global cultivation footprint, relatively lower production costs compared to other berry varieties, and high consumer familiarity across both developed and emerging markets. Strawberries benefit from year-round availability enabled by greenhouse cultivation, controlled-environment agriculture, and international trade networks that ensure continuous supply. Their adaptability across multiple climates and farming systems further enhances production scalability, allowing producers in North America, Europe, Latin America, and Asia-Pacific to maintain consistent volumes. Additionally, strawberries remain highly versatile across consumption formats, including fresh retail sales, desserts, dairy integration, beverages, and processed foods, reinforcing their dominance.The leading growth driver for blueberries is expanding international trade supported by counter-seasonal production cycles. Countries such as Peru, Chile, and Mexico have strategically invested in export-oriented cultivation to supply North American and European markets during off-season periods. Improvements in cold-chain logistics and packaging technologies have further enabled long-distance transportation while maintaining product quality. Blueberries also experience rising demand from food processing industries, especially for smoothies, cereals, snack bars, and functional beverages, reinforcing long-term growth momentum.Raspberries account for approximately 17% of the global market, positioned as a premium berry segment driven by specialty retail demand and culinary applications. Their delicate texture and distinctive flavor profile make raspberries particularly attractive for gourmet desserts, artisanal bakery products, and upscale foodservice menus. The primary driver for raspberries is premiumization within the fresh produce sector, where consumers increasingly seek differentiated fruit experiences. Rising disposable income levels and growing café culture worldwide have amplified raspberry consumption, especially in urban markets.Although raspberries present higher production and logistics costs due to fragility and shorter shelf life, technological improvements in packaging, modified atmosphere storage, and rapid distribution systems are gradually mitigating these limitations. Producers are investing in protected cultivation methods such as tunnels and greenhouses to improve yield consistency, allowing raspberries to expand beyond traditional seasonal boundaries.Blackberries, contributing nearly 9% of total market share, maintain steady growth supported by niche consumer demand and expanding usage in jams, preserves, and premium beverages. Their increasing popularity stems from growing consumer interest in darker fruits associated with higher antioxidant concentrations.

Application Insights

Application trends in the global berries market reveal a strong shift toward fresh and minimally processed consumption patterns. Direct fresh consumption dominates applications, representing over 62% of total demand in 2025. This dominance reflects broader consumer transitions away from highly processed snacks toward natural, nutrient-rich alternatives perceived as healthier lifestyle choices. Increasing awareness surrounding clean-label diets, weight management, and preventive healthcare continues to reinforce fresh berry consumption across age groups.The leading application driver for fresh consumption is convenience combined with perceived health benefits. Berries require minimal preparation, making them highly compatible with fast-paced urban lifestyles. Retailers increasingly promote ready-to-eat packaging formats, including portion-controlled packs and mixed berry assortments, which further stimulate impulse purchases. Social media influence and visual appeal also play a significant role, as berries are widely associated with aesthetically appealing meals and wellness-focused dietary trends.Foodservice applications account for approximately 21% of market demand, supported by innovation across bakery, dessert, and beverage categories. Restaurants, cafés, and quick-service chains increasingly integrate berries into menu offerings to enhance flavor profiles while reinforcing premium brand positioning. The expansion of global café culture and dessert-oriented dining experiences has significantly increased berry usage in pastries, cheesecakes, smoothies, and frozen desserts. Seasonal menu rotations further boost demand as berries are frequently marketed as fresh and indulgent ingredients.Industrial food processing contributes nearly 17% of total applications, supported by rising production of smoothies, yogurts, breakfast cereals, and functional beverages. The primary growth driver within this segment is the increasing incorporation of natural fruit ingredients as replacements for artificial flavors and colors. Food manufacturers leverage berries to enhance nutritional labeling claims, particularly antioxidant and vitamin content, aligning products with consumer expectations for transparency and health functionality. Frozen berries play a crucial role in this segment, enabling year-round manufacturing consistency.

Distribution Channel Insights

Distribution dynamics within the berries market highlight the importance of modern retail infrastructure and cold-chain efficiency. Supermarkets and hypermarkets dominate distribution channels with approximately 48% market share, benefiting from advanced refrigeration capabilities, standardized quality control systems, and high consumer footfall. Large-format retailers provide consistent product availability, attractive displays, and promotional pricing strategies that drive bulk purchasing behavior.The leading driver for supermarket dominance is integrated supply-chain management, allowing retailers to maintain freshness standards while minimizing spoilage. Partnerships between growers, exporters, and retail chains have strengthened procurement efficiency, enabling global sourcing strategies that ensure uninterrupted supply regardless of seasonal limitations.Convenience stores account for around 18% of sales, supported by increasing urbanization and on-the-go consumption habits. Smaller package sizes and proximity to residential and workplace areas encourage frequent purchases, particularly among younger consumers seeking quick healthy snack options.Online grocery platforms represent nearly 16% of distribution and are expanding rapidly due to digital transformation in retail. E-commerce adoption accelerated significantly following shifts in consumer purchasing behavior toward home delivery and contactless shopping. Advanced logistics, real-time inventory tracking, and subscription-based fresh produce services are improving consumer trust in online fresh fruit purchasing. The leading growth driver for online channels is convenience combined with improved last-mile cold-chain delivery systems that preserve product freshness.Wholesale and traditional markets contribute the remaining 18%, particularly across emerging economies where informal retail networks remain influential. These channels play a crucial role in regional distribution by connecting small-scale farmers with urban markets, ensuring affordability and accessibility in price-sensitive regions.

End-Use Insights

Household consumption remains the dominant end-use category, accounting for nearly 58% of total market demand. Increasing health awareness, rising disposable incomes, and growing preference for fresh fruits as daily dietary components continue to drive residential purchases. Families increasingly incorporate berries into breakfast routines, snacks, and home-prepared desserts, reinforcing consistent consumption patterns.The leading driver for household dominance is the integration of berries into everyday wellness habits. Nutrition campaigns promoting fruit intake, combined with growing awareness of antioxidants and immune-supporting nutrients, have encouraged frequent household purchases. The availability of smaller packaging formats and mixed berry offerings further supports adoption among nuclear families and single-person households.The foodservice sector represents the fastest-growing end-use segment, expanding alongside global café culture, premium dessert consumption, and experiential dining trends. Restaurants and beverage chains increasingly rely on berries to differentiate menus through freshness and visual appeal. Seasonal promotions featuring berry-based beverages and desserts contribute to recurring demand cycles.Beverage manufacturers are emerging as significant end users, incorporating berries into smoothies, flavored waters, kombuchas, and functional drinks. The rise of health-oriented beverages has positioned berries as natural flavor enhancers with strong nutritional branding advantages. Simultaneously, nutraceutical and wellness industries are expanding berry utilization in supplements, powders, and fortified foods due to their antioxidant-rich composition.Export-driven demand from bakery and dairy industries further strengthens long-term consumption growth. Yogurt producers, ice cream manufacturers, and confectionery companies increasingly depend on stable berry supply chains to support product innovation and premium product positioning.

| By Product Type | By Nature | By Distribution Channel | By Application | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America held approximately 32% of the global berries market share in 2025, led primarily by the United States and Canada. The region benefits from advanced agricultural practices, high consumer awareness regarding nutrition, and one of the most sophisticated cold-chain infrastructures globally. Consumers in North America demonstrate strong preference for fresh, organic, and locally sourced produce, which significantly supports berry consumption across retail channels.The primary regional growth driver is year-round availability supported by integrated import networks. The United States remains both the largest consumer and importer of berries, sourcing significant volumes from Mexico, Peru, and Chile during domestic off-seasons. Strong retail penetration, widespread supermarket networks, and high purchasing power enable consistent demand growth. Additionally, increasing adoption of healthy snacking habits and functional diets continues to elevate berry consumption frequency. Innovation in packaging, including resealable and snack-sized containers, further encourages repeat purchases.Technological advancements in farming, including precision agriculture and greenhouse production, also contribute to regional expansion by improving yields and extending growing seasons. Rising demand for organic berries and sustainably farmed produce continues to shape purchasing behavior, reinforcing North America’s leadership position.

Europe

Europe accounted for nearly 27% of global demand, with Germany, the United Kingdom, Spain, and France representing key consumption markets. European consumers exhibit strong preference for sustainably sourced and organic produce, driving retailers to prioritize environmentally responsible supply chains. Government regulations promoting pesticide reduction and sustainable agriculture further influence production and sourcing practices.The leading regional growth driver in Europe is sustainability-driven consumption combined with premium retail positioning. Consumers increasingly value traceability, ethical sourcing, and environmentally friendly packaging, encouraging berry producers to adopt eco-certified farming methods. Expansion of private-label premium fruit ranges within supermarkets has also increased accessibility to high-quality berries.Europe’s well-developed logistics infrastructure enables efficient cross-border trade, allowing southern producers such as Spain to supply northern markets year-round. Additionally, increasing vegan and plant-forward dietary trends are supporting berry consumption as natural dessert alternatives and breakfast ingredients.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market, projected to expand at over 10% CAGR during the forecast period. China, Japan, South Korea, and India are witnessing rapid growth driven by urbanization, rising disposable incomes, and evolving dietary preferences. Consumers are increasingly shifting toward premium fruits perceived as healthier and more aspirational.The primary driver for regional growth is expanding middle-class populations combined with Western dietary influence. Urban consumers increasingly incorporate berries into smoothies, bakery products, and café beverages. China is emerging as both a major producer and importer, investing heavily in greenhouse cultivation technologies to support domestic supply. E-commerce platforms also play a critical role in expanding accessibility, particularly in densely populated urban centers.In India and Southeast Asia, growing health awareness and increasing exposure to international cuisines are accelerating berry adoption. Premium retail chains and online grocery platforms are introducing berries to new consumer segments, transforming them from luxury imports into mainstream health foods.

Middle East & Africa

The Middle East and Africa region demonstrates steadily rising demand, supported primarily by import-driven consumption. Countries such as the United Arab Emirates and Saudi Arabia exhibit strong purchasing power and growing preference for premium fresh fruits. Expansion of modern retail infrastructure and luxury hospitality sectors significantly contributes to berry demand.The key regional growth driver is rising disposable income combined with expanding tourism and hospitality industries. Hotels, restaurants, and high-end cafés increasingly incorporate berries into international cuisine offerings, driving consistent imports. Additionally, health-conscious expatriate populations influence consumption patterns by introducing Western dietary habits.South Africa plays a strategic role as an export-oriented producer supplying European and Asian markets. Favorable climatic conditions and investment in export logistics have strengthened the region’s position within global berry supply chains.

Latin America

Latin America serves as a critical supply-side powerhouse within the global berries market, with Chile, Peru, and Mexico acting as major exporters. The region benefits from diverse climatic zones that enable counter-seasonal production, allowing continuous supply to Northern Hemisphere markets.The leading driver for Latin American growth is export-led agricultural expansion supported by international trade agreements and foreign investment in berry farming. Producers have adopted advanced cultivation technologies, irrigation systems, and post-harvest handling processes to meet stringent quality standards required by North American and European retailers.Blueberries and strawberries represent the fastest-expanding export categories, supported by rising global demand for premium fruits. Infrastructure improvements in ports, cold storage, and logistics networks further enhance export efficiency. As global berry consumption continues to rise, Latin America is expected to remain a cornerstone of global supply stability, reinforcing its long-term strategic importance within the industry.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Fresh Berries Market

- Driscoll’s Inc.

- Dole Food Company, Inc.

- Berry Global Group Farms

- Wish Farms

- Naturipe Farms LLC

- California Giant Berry Farms

- Hortifrut S.A.

- Camposol Holding PLC

- Agrovision Corp.

- Planasa Group

- Fall Creek Farm & Nursery

- Joy Wing Mau Group

- Costa Group Holdings

- Angus Soft Fruits Ltd.

- Sun Belle Inc.