Freeze-Dried Acerola Powder Market Size

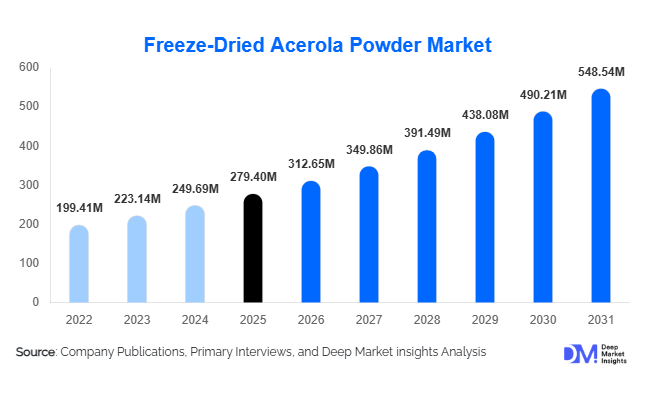

According to Deep Market Insights,the global freeze-dried acerola powder market size was valued at USD 279.4 million in 2025 and is projected to grow from USD 312.65 million in 2026 to reach USD 548.54 million by 2031, expanding at a CAGR of 11.9% during the forecast period (2026–2031). Market growth is primarily driven by increasing consumer preference for natural vitamin C sources, rising adoption of clean-label ingredients across functional foods and nutraceuticals, and growing demand for immune-support formulations worldwide. Freeze-drying technology preserves bioactive compounds and antioxidant potency, making acerola powder a premium ingredient in dietary supplements, fortified beverages, cosmetics, and pharmaceutical formulations.

Key Market Insights

- Natural vitamin C replacement trends are accelerating, with manufacturers shifting away from synthetic ascorbic acid toward plant-derived ingredients.

- Nutraceutical applications dominate global demand, supported by expanding immunity and preventive healthcare markets.

- North America leads global consumption, driven by strong dietary supplement penetration and clean-label awareness.

- Asia-Pacific is the fastest-growing region, fueled by rising middle-class health awareness and expanding supplement manufacturing capacity.

- Organic-certified acerola powder demand is increasing rapidly, enabling premium pricing and export opportunities.

- Technological improvements in freeze-drying are enhancing vitamin retention and improving production efficiency.

What are the latest trends in the freeze-dried acerola powder market?

Shift Toward Natural and Clean-Label Nutrition

Consumers are increasingly prioritizing natural ingredients with recognizable sourcing, leading food and supplement manufacturers to replace synthetic additives with botanical alternatives. Freeze-dried acerola powder is gaining popularity due to its naturally high vitamin C concentration and antioxidant profile. Clean-label product positioning has become a key differentiator across functional beverages, gummies, and fortified snacks. Brands increasingly highlight acerola as a “fruit-derived vitamin C” ingredient, improving consumer trust and enabling premium pricing strategies. Regulatory encouragement for natural additives, particularly in Europe and North America, is further reinforcing this transition.

Expansion of Functional Beverage Applications

Functional beverages represent one of the fastest-growing applications for freeze-dried acerola powder. Ready-to-mix immunity drinks, hydration powders, and wellness beverages increasingly incorporate acerola for both nutritional enhancement and natural preservation benefits. Beverage manufacturers value its stability, solubility, and compatibility with plant-based formulations. Social media-driven wellness trends and rising demand for convenient nutrition solutions are accelerating adoption, especially among younger consumers seeking daily immunity support products.

What are the key drivers in the freeze-dried acerola powder market?

Rising Preventive Healthcare Awareness

Global consumer behavior has shifted toward preventive health management, increasing daily supplement consumption. Vitamin C remains one of the most widely consumed micronutrients worldwide, and natural sources such as acerola are gaining preference due to perceived higher bioavailability. Growth in immunity supplements, collagen boosters, and antioxidant blends continues to drive ingredient demand across developed and emerging markets.

Growth of the Nutraceutical Industry

The rapid expansion of the global nutraceutical industry is significantly supporting market growth. Manufacturers are incorporating freeze-dried acerola powder into capsules, gummies, powders, and functional blends targeting immune health, skin wellness, and energy support. The ability to standardize vitamin C content above 25% makes freeze-dried acerola suitable for high-performance formulations demanded by premium supplement brands.

What are the restraints for the global market?

High Production Costs

Freeze-drying remains an energy-intensive process compared to conventional drying technologies, resulting in higher product pricing. This limits adoption among price-sensitive manufacturers and emerging markets where synthetic alternatives remain cheaper. Capital investments required for advanced freeze-drying infrastructure also create entry barriers for new participants.

Raw Material Supply Volatility

Acerola cultivation is geographically concentrated, primarily in Brazil and parts of Latin America. Climate variability, seasonal harvest fluctuations, and agricultural risks can influence raw material availability and pricing stability. Supply chain disruptions can therefore impact production planning and long-term pricing agreements.

What are the key opportunities in the freeze-dried acerola powder industry?

Beauty-from-Within and Cosmeceutical Growth

The expanding ingestible beauty segment presents significant opportunities for acerola powder adoption. Vitamin C’s role in collagen synthesis and antioxidant protection makes it highly attractive for skin health supplements and cosmetic formulations. Brands are increasingly launching beauty powders and functional drinks incorporating acerola as a natural active ingredient, creating high-margin opportunities.

Emerging Market Expansion

Rapid urbanization and rising disposable incomes across Asia-Pacific and the Middle East are expanding demand for premium health products. Local nutraceutical manufacturing growth in countries such as India and China is increasing ingredient imports. Export-oriented suppliers are capitalizing on these markets by establishing regional partnerships and certified supply chains.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 279.4 Million |

| Market Size in 2026 | USD 312.65 Million |

| Market Size in 2031 | USD 548.54 Million |

| CAGR | 11.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The organic freeze-dried acerola powder segment holds the leading position in the market, primarily driven by accelerating consumer demand for clean-label, traceable, and certified natural ingredients across nutraceutical, functional food, and premium wellness categories. Increasing awareness regarding pesticide-free sourcing, sustainable agriculture practices, and transparency in ingredient labeling has significantly strengthened adoption of organic variants among health-conscious consumers and premium product manufacturers. In addition, regulatory encouragement for organic certifications in developed markets and growing willingness among consumers to pay premium prices for high-quality natural vitamin C sources continue to reinforce segment dominance. Organic freeze-dried acerola powder is extensively utilized in high-value dietary supplements, plant-based nutrition products, and fortified beverages where ingredient purity and brand positioning are critical.

Conventional freeze-dried acerola powder continues to maintain substantial demand, particularly among large-scale food and beverage manufacturers prioritizing cost efficiency and consistent supply volumes. This segment benefits from economies of scale, enabling manufacturers to incorporate natural vitamin C fortification into mass-market products while maintaining competitive pricing structures. Meanwhile, high-potency formulations containing vitamin C concentrations above 25% are witnessing increasing adoption as supplement brands shift toward standardized, performance-oriented formulations designed to meet specific dosage requirements. The growing preference for scientifically validated nutrient content, combined with expanding preventive healthcare trends, is further accelerating innovation in concentrated and standardized acerola powder formats.

Application Insights

Dietary supplements represent the leading application segment, supported by the sustained global focus on immunity enhancement, preventive healthcare adoption, and expanding digital supplement retail ecosystems. Rising consumer preference for plant-derived vitamin C alternatives over synthetic ascorbic acid has strengthened acerola powder utilization in capsules, tablets, powders, and liquid supplements. The growth of personalized nutrition programs and subscription-based supplement models is also contributing to higher consumption volumes, positioning dietary supplements as the primary demand driver within the application landscape.

Functional foods and beverages are emerging as one of the fastest-growing applications, fueled by increasing reformulation activities among food manufacturers seeking natural fortification solutions. Acerola powder is widely incorporated into fortified juices, energy drinks, dairy alternatives, snack bars, and plant-based products to enhance nutritional value while supporting clean-label claims. Cosmetics and personal care applications are expanding steadily as antioxidant-rich ingredients gain prominence in both topical skincare and ingestible beauty products targeting skin health and anti-aging benefits. Pharmaceutical applications maintain stable demand, largely focused on preventive formulations, immune-support therapies, and adjunct nutritional products designed to support overall wellness and recovery.

Distribution Channel Insights

Direct business-to-business ingredient supply remains the dominant distribution channel, driven by long-term procurement partnerships between acerola powder producers and large nutraceutical, pharmaceutical, and food manufacturers. These contractual agreements ensure consistent quality standards, secure supply chains, and predictable pricing structures, which are essential for large-scale production planning. The increasing globalization of ingredient sourcing has further strengthened direct supplier relationships, particularly among multinational manufacturers seeking reliable natural vitamin C inputs.

Specialty ingredient distributors play a critical role in supporting small and mid-sized brands entering the functional nutrition and clean-label product space. These distributors provide technical formulation support, regulatory guidance, and flexible order quantities that enable innovation among emerging brands. Additionally, online ingredient procurement platforms are gaining traction as digital transformation reshapes supply chain operations. These platforms enhance sourcing transparency, improve price discovery, and facilitate cross-border trade by connecting global suppliers with manufacturers seeking verified natural ingredients.

End-Use Industry Insights

The nutraceutical industry accounts for the largest share of global demand, primarily driven by increasing supplement consumption, aging populations, and growing consumer investment in preventive health solutions. Acerola powder’s naturally high vitamin C concentration and antioxidant profile align closely with market demand for plant-based immune-support ingredients, reinforcing its widespread adoption across nutritional formulations. Continuous product innovation, including immunity blends, energy supplements, and wellness powders, further strengthens demand within this segment.

The food and beverage industry represents the fastest-growing end-use sector, supported by widespread clean-label reformulations and increasing consumer preference for functional nutrition products. Manufacturers are increasingly replacing synthetic additives with natural alternatives such as acerola powder to meet evolving regulatory standards and consumer expectations. In cosmetics and personal care, acerola extracts are gaining traction in antioxidant skincare, nutricosmetics, and beauty-from-within product categories due to their perceived skin-protective and collagen-supporting benefits. Pharmaceutical demand remains stable, supported by preventive healthcare trends and integration of natural ingredients into complementary therapies. Emerging adoption within premium pet nutrition and animal supplements is also contributing incremental growth as pet owners increasingly seek functional and natural nutrition solutions for companion animals.

Explore more data points, trends and opportunities Download Free Sample Report

Freeze-Dried Acerola Powder Market Segmentations

By Product Type

- Organic Freeze-Dried Acerola Powder

- Conventional Freeze-Dried Acerola Powder

- High Vitamin C Standardized Powder (>25% Vitamin C)

- Low/Medium Potency Acerola Powder (<25% Vitamin C)

By Application

- Dietary Supplements & Nutraceuticals

- Functional Foods

- Functional Beverages

- Cosmetics & Personal Care Products

- Pharmaceutical Preparations

- Animal Nutrition & Pet Supplements

By Distribution Channel

- Direct B2B Ingredient Supply

- Specialty Ingredient Distributors

- Online Ingredient Marketplaces

- Contract Manufacturing & Private Label Supply

By End-Use Industry

- Nutraceutical Manufacturers

- Food & Beverage Manufacturers

- Cosmetics & Personal Care Companies

- Pharmaceutical Companies

- Animal Nutrition Producers

Regional Insights

North America

North America accounts for approximately 32% of global market share, led predominantly by the United States, where high consumer awareness regarding immunity, wellness, and preventive healthcare continues to drive strong demand. The region benefits from advanced nutraceutical manufacturing infrastructure, robust research and development capabilities, and widespread adoption of clean-label and organic products. Rapid innovation in functional beverages, sports nutrition, and plant-based supplements further supports market expansion. Additionally, strong e-commerce penetration, influencer-driven wellness trends, and increasing demand for natural vitamin C alternatives are accelerating regional growth, while regulatory acceptance of botanical ingredients enhances commercialization opportunities.

Europe

Europe represents nearly 27% of global demand, supported by mature organic food markets and stringent regulatory frameworks that encourage the use of natural additives over synthetic alternatives. Countries such as Germany, France, Italy, and the United Kingdom lead adoption due to high consumer trust in certified organic products and sustainability-focused purchasing behavior. Regional growth is further driven by increasing clean-label reformulation initiatives among food manufacturers, rising demand for plant-based nutrition, and expanding nutricosmetic product innovation. Strong retail penetration of health foods and growing investment in functional ingredient research also contribute to sustained market expansion across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at an estimated CAGR of nearly 14%, driven by rising disposable incomes, rapid urbanization, and increasing health awareness among expanding middle-class populations. China and Japan remain key consumption hubs due to established supplement markets and strong demand for functional beverages, while India is emerging rapidly as a manufacturing and export center for nutraceutical products. Growth is further supported by increasing adoption of preventive healthcare practices, expanding e-commerce nutrition platforms, government initiatives promoting domestic supplement production, and growing acceptance of natural botanical ingredients across food, beverage, and wellness applications.

Latin America

Latin America plays a strategic dual role as both a production and consumption hub within the global acerola powder market. Brazil dominates regional supply due to favorable climatic conditions supporting large-scale acerola cultivation and established agricultural expertise. Expansion of processing facilities and improvements in freeze-drying technologies are enhancing export competitiveness and strengthening integration into global supply chains. Rising regional consumption of functional foods and dietary supplements, coupled with increasing investments in value-added ingredient processing, is further supporting market development across Latin America.

Middle East & Africa

The Middle East and Africa market is experiencing steady growth, particularly in the United Arab Emirates and Saudi Arabia, where rising disposable incomes and growing wellness awareness are fueling demand for premium health and nutrition products. Expansion of modern retail channels, increasing penetration of international supplement brands, and growing consumer interest in immunity-support products are key growth drivers. Additionally, the region’s expanding hospitality and luxury wellness sectors are promoting functional beverages and nutraceutical adoption, while gradual regulatory modernization is improving market accessibility for natural ingredient suppliers.

Key Players in the Freeze-Dried Acerola Powder Market

- Givaudan (Naturex)

- Symrise (Diana Food)

- Nexira

- Duas Rodas Industrial

- Martin Bauer Group

- Döhler Group

- Van Drunen Farms

- FutureCeuticals

- Paradise Fruits Solutions

- Xi’an Lyphar Biotech

- Organicway Inc.

- Green Source Organics

- BioActives Japan Corporation

- Herbo Nutra

- NutriBotanica