Football Merchandise Market Size

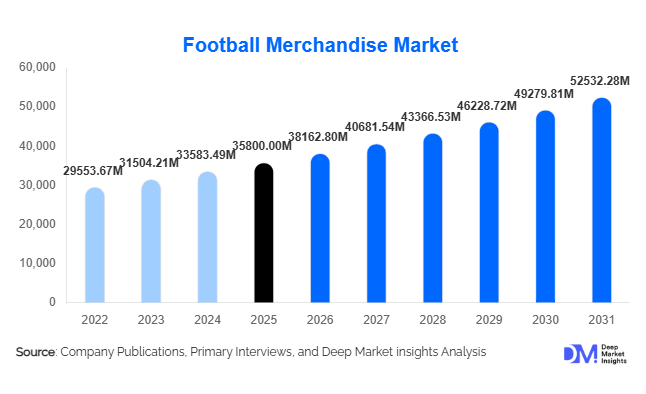

According to Deep Market Insights, the global football merchandise market size was valued at USD 35,800 million in 2025 and is projected to grow from USD 38,162.80 million in 2026 to reach USD 52,532.28 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The football merchandise market growth is primarily driven by rising global fan engagement, digital direct-to-consumer (DTC) expansion, the commercialization of elite football leagues, and increasing participation in grassroots football worldwide.

Global tournaments such as the FIFA World Cup and premier club competitions, including the English Premier League, La Liga, Bundesliga, Serie A, and the UEFA Champions League, continue to serve as key revenue catalysts. The increasing integration of football culture into mainstream fashion, collaborations with designers and influencers, and the growing popularity of women’s football are further expanding the market base. Additionally, e-commerce penetration and data-driven personalization strategies are improving global accessibility, raising average order values, and strengthening profit margins for leading brands.

Key Market Insights

- Apparel dominates the market, accounting for nearly 48% of total revenue in 2025, led by replica jerseys and lifestyle collections.

- Club-licensed merchandise leads, contributing approximately 54% of global revenue due to year-round fan loyalty.

- Online DTC channels account for over 42% of total sales, reflecting the rapid shift toward digital retail ecosystems.

- Europe holds the largest regional share (38%), supported by strong domestic leagues and international fan bases.

- Asia-Pacific is the fastest-growing region, expanding at over 8.5% CAGR through 2031.

- Premiumization and limited-edition drops are driving higher average selling prices and stronger brand exclusivity.

What are the latest trends in the football merchandise market?

Premiumization and Limited-Edition Drops

Football merchandise is increasingly positioned as a lifestyle and fashion statement rather than solely sportswear. Clubs and brands are launching retro collections, anniversary editions, and player milestone kits in limited quantities to create scarcity-driven demand. These premium launches often command 20–40% price premiums compared to standard replica jerseys. Collaborations with fashion designers and streetwear labels are also strengthening football’s presence in urban fashion, expanding the consumer base beyond traditional sports fans.

Digital-First Retail and Personalization

Online DTC platforms are transforming purchasing behavior. AI-powered recommendation engines, real-time inventory visibility, and customization features such as personalized name printing are improving conversion rates. Mobile apps now integrate loyalty rewards, early-access drops, and geo-targeted marketing campaigns. Social commerce and influencer-led promotions are particularly effective in Asia-Pacific and North America, enabling brands to directly engage younger demographics and international fans.

What are the key drivers in the football merchandise market?

Globalization of Elite Football Leagues

The international broadcasting reach of European leagues has significantly expanded global fan bases. Overseas supporters of clubs in England, Spain, Germany, and Italy contribute substantially to replica jersey and accessories sales. Cross-border e-commerce logistics and localized marketing strategies have enabled clubs to monetize global fandom effectively.

Expansion of Women’s Football

The commercialization of women’s leagues and international tournaments is accelerating merchandise demand. Dedicated women-fit apparel, athlete-endorsed collections, and inclusive marketing campaigns are driving double-digit growth in the women’s segment. This expansion is broadening the addressable market and strengthening long-term growth prospects.

What are the restraints for the global market?

Counterfeit and Unlicensed Products

Unauthorized replicas continue to impact legitimate revenue streams, particularly in price-sensitive emerging markets. Counterfeiting is estimated to erode up to 8–12% of potential annual revenue, affecting brand equity and pricing power.

Raw Material and Logistics Volatility

Fluctuations in polyester, cotton, and synthetic fiber prices directly influence production costs. Rising shipping expenses and supply chain disruptions can compress margins, especially for mid-tier manufacturers operating on tighter cost structures.

What are the key opportunities in the football merchandise industry?

Direct-to-Consumer Ecosystem Expansion

Clubs and manufacturers are investing heavily in proprietary digital storefronts to improve margins and customer retention. Enhanced data analytics, subscription-based merchandise drops, and exclusive online launches can increase customer lifetime value and strengthen brand loyalty globally.

Emerging Market Penetration

India, Indonesia, Saudi Arabia, and other high-growth economies present strong opportunities due to rising youth participation and digital retail adoption. Localized pricing, regional warehousing, and strategic partnerships with domestic leagues can unlock incremental revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 35800 Million |

| Market Size in 2026 | USD 38162.80 Million |

| Market Size in 2031 | USD 52532.28 Million |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Apparel remains the dominant product category, accounting for approximately 48% of total global revenue in 2025, making it the primary growth engine of the football merchandise market. Within apparel, replica jerseys alone contribute nearly 30% of overall market sales, underscoring their emotional and symbolic importance among fans. The leading driver behind apparel’s dominance is the strong psychological association between supporters and club identity, reinforced by seasonal kit launches (home, away, and third kits) that stimulate repeat purchases annually. Limited-edition releases, retro collections, and player-specific editions further enhance demand by introducing scarcity-driven purchasing behavior. Additionally, the integration of football apparel into everyday lifestyle fashion, through streetwear collaborations and designer partnerships, has expanded its consumer base beyond match-day supporters.

Footwear represents approximately 21% of market revenue, supported by innovation in performance football boots and the crossover appeal of lifestyle sneakers inspired by club aesthetics. Accessories contribute around 16%, including scarves, caps, socks, and bags, which benefit from impulse buying and lower price points. Equipment and collectibles collectively account for the remaining share, with trading cards, signed memorabilia, and digital collectibles witnessing growing interest among younger and investment-oriented consumers.

Licensing Type Insights

Club-licensed merchandise leads with a 54% share of total revenue in 2025, driven by year-round fan engagement and global league commercialization. Unlike tournament-driven demand cycles, club merchandise benefits from consistent domestic league schedules, international tours, and global broadcast exposure. The expansion of global fan bases for elite European clubs has significantly strengthened cross-border e-commerce sales, particularly in Asia-Pacific and North America.

National team merchandise accounts for approximately 26% of total revenue, with demand peaking during major international tournaments. Sales spikes during global competitions can elevate annual revenue by 15–25% in tournament years. Player-branded merchandise is expanding steadily, fueled by athlete endorsements, social media influence, and individual brand-building strategies. Younger demographics are particularly responsive to player-driven collections, especially when linked to limited drops and lifestyle integration.

Distribution Channel Insights

Online direct-to-consumer (DTC) platforms account for 42% of total global sales, making them the leading distribution channel in 2025. The primary growth driver for this segment is higher margin realization, as brands reduce reliance on intermediaries while leveraging first-party customer data. AI-driven personalization, real-time inventory management, and localized digital marketing campaigns have significantly improved conversion rates and customer retention.

Offline retail, including brand flagship stores, sports retail chains, and multi-brand outlets, holds approximately 38% market share. While physical retail remains relevant for experiential engagement and immediate purchases, brands are increasingly integrating omnichannel strategies to unify inventory and enhance consumer convenience. Stadium and event-based sales contribute the remaining share, particularly benefiting from match-day purchases and international tournament events.

End-Use Insights

Individual consumers dominate the market with approximately 78% of total revenue in 2025, reflecting the emotional and lifestyle-driven nature of football merchandise purchases. The key driver for this segment is fan identity expression, supported by recurring seasonal kit releases and limited-edition collaborations. Institutional procurement, accounting for roughly 15% of total revenue, is growing at nearly 7% CAGR, driven by the expansion of football academies, school-level programs, and community leagues. Governments and private sports organizations are investing in grassroots development, increasing bulk purchases of kits, training apparel, and equipment. Corporate gifting and promotional merchandise form a smaller yet expanding niche, particularly during tournament years when companies leverage football-themed campaigns for marketing engagement.

Explore more data points, trends and opportunities Download Free Sample Report

Football Merchandise Market Segmentations

By Product Type

- Apparel

- Footwear

- Accessories

- Equipment & Sporting Goods

- Collectibles & Memorabilia

By Licensing Type

- Club-Licensed Merchandise

- National Team-Licensed Merchandise

- Tournament/Event-Licensed Merchandise

- Player-Branded Merchandise

- Non-Licensed/Generic Merchandise

By Distribution Channel

- Online Direct-to-Consumer

- E-commerce Marketplaces

- Offline Retail

- Stadium & Event-Based Sales

By End Use

- Individual Consumers

- Institutional Procurement

- Corporate Gifting & Promotional Use

By Consumer Type

- Men

- Women

- Kids & Youth

Regional Insights

Europe

Europe leads the global football merchandise market with a 38% share in 2025, supported by the commercial dominance of leagues such as the English Premier League, La Liga, Bundesliga, and Serie A. The United Kingdom alone accounts for approximately 11% of global revenue, driven by strong domestic consumption and extensive global fan exports. Germany contributes around 7%, supported by deep-rooted club loyalty and high per capita sports spending. Spain, Italy, and France remain major contributors due to globally recognized clubs and strong tourism-driven merchandise purchases. Key regional growth drivers include international broadcasting rights expansion, premium pricing strategies, strong stadium retail networks, and sustained demand from overseas fans purchasing European club merchandise via e-commerce platforms.

North America

North America holds approximately 24% market share, with the United States representing nearly 19% of global licensed merchandise imports. Regional growth is driven by rising youth soccer participation, increasing popularity of European leagues, and expanding Major League Soccer fan engagement. The growth of digital retail ecosystems and high disposable income levels further strengthen demand. Additionally, multicultural demographics with strong ties to football-centric nations contribute to steady merchandise consumption.

Asia-Pacific

Asia-Pacific accounts for around 22% of global revenue and is the fastest-growing region, expanding at over 8.5% CAGR. China, India, Japan, and Indonesia are key growth markets. Rising middle-class income, rapid urbanization, and strong e-commerce penetration are primary drivers. Increasing youth participation in football academies and growing social media engagement with international clubs are accelerating merchandise sales. Localization strategies and improved cross-border logistics are further strengthening regional growth.

Middle East & Africa

The Middle East & Africa region represents approximately 9% of global revenue. Saudi Arabia and the UAE demonstrate strong per capita spending due to significant investments in domestic leagues, stadium infrastructure, and international player acquisitions. Government-backed sports diversification strategies and high disposable incomes are key drivers. In Africa, strong football culture in countries such as Nigeria and South Africa supports consistent domestic demand, while growing retail infrastructure enhances accessibility.

Latin America

Latin America contributes roughly 7% of global market revenue, led by Brazil and Argentina. Deep-rooted football culture and strong club loyalty underpin domestic merchandise consumption. Growth drivers include expanding middle-class purchasing power, improved retail penetration, and rising digital commerce adoption. International success of regional players also stimulates player-branded merchandise demand, particularly among younger demographics.