Foods High in Amino Acid Lysine Market Size

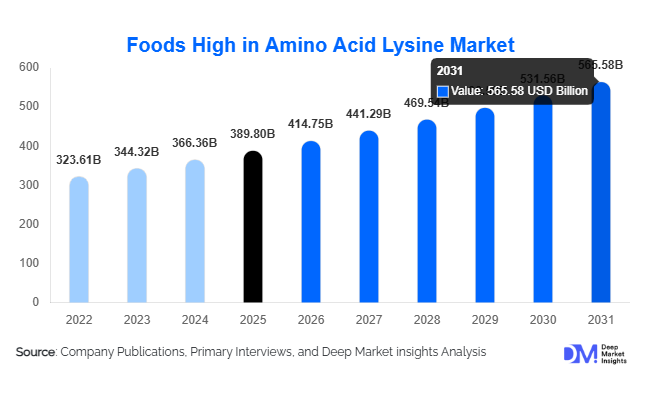

According to Deep Market Insights, the global foods high in amino acid lysine market size was valued at USD 389.8 billion in 2025 and is projected to grow from USD 414.75 billion in 2026 to reach USD 565.58 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). Market growth is primarily driven by rising global protein consumption, increasing awareness of essential amino acid deficiencies, expansion of plant-based diets, and the growing integration of lysine-rich ingredients in functional and clinical nutrition products.

Key Market Insights

- Animal-based lysine-rich foods dominate the market, accounting for over 60% of global consumption due to established meat, poultry, dairy, and seafood industries.

- Plant-based lysine sources are the fastest-growing segment, fueled by vegan and flexitarian dietary trends across Europe and Asia-Pacific.

- North America leads global consumption, supported by high per-capita protein intake and a strong sports nutrition industry.

- Asia-Pacific is the fastest-growing region, driven by rising disposable incomes and expanding middle-class dietary upgrades.

- Clinical and performance nutrition applications are accelerating demand, particularly among aging populations and fitness-conscious consumers.

- Fortified and lysine-enhanced food innovation is reshaping competitive dynamics in processed and packaged food categories.

What are the latest trends in the foods high in amino acid lysine market?

Rise of Plant-Based Lysine-Rich Foods

The surge in plant-based dietary adoption is significantly influencing the lysine-rich foods landscape. Traditionally dominated by meat and dairy, the market is witnessing rapid expansion in legumes, soy-based products, quinoa, and amaranth. Food manufacturers are increasingly promoting lysine completeness in plant protein blends, especially in vegan protein products. Fermentation technologies and crop biofortification techniques are being explored to enhance lysine concentration in cereals and plant-based ready-to-eat foods. Retail shelves are seeing expanded offerings of lentil pastas, chickpea snacks, and soy-based dairy alternatives positioned specifically for protein adequacy and amino acid balance.

Growth in Functional & Clinical Nutrition Integration

Lysine’s recognized role in immune support, collagen synthesis, and calcium absorption has led to its increased integration into fortified foods and medical nutrition products. Hospitals, eldercare institutions, and sports nutrition brands are incorporating lysine-rich ingredients into high-protein meals and supplements. Ready-to-drink protein beverages, high-protein yogurts, and fortified cereals are increasingly marketed with amino acid-specific benefits. This trend is supported by regulatory approvals allowing amino acid disclosure on packaging, improving consumer transparency and trust.

What are the key drivers in the foods high in amino acid lysine market?

Rising Global Protein Consumption

Growing fitness awareness and muscle-health priorities have significantly increased protein intake worldwide. Countries such as the U.S., China, Brazil, and India are witnessing steady increases in per-capita meat, dairy, and legume consumption. High-protein dietary patterns including keto, paleo, and weight-management diets further strengthen demand for lysine-rich foods.

Expansion of Sports & Performance Nutrition

The global sports nutrition industry, valued at over USD 90 billion, is creating sustained demand for high-lysine food products. Protein powders, fortified snacks, dairy-based drinks, and soy protein isolates are increasingly used by athletes and recreational fitness consumers. This segment is growing at above 8% CAGR, outpacing traditional household food demand.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in soybean prices, livestock feed costs, dairy input prices, and global commodity trade dynamics significantly affect production margins. Price sensitivity in emerging markets can restrict premium product adoption.

Regulatory & Labeling Constraints

Strict health claim regulations in North America and Europe limit explicit amino acid-related marketing claims. Compliance with nutritional labeling standards increases operational complexity for food manufacturers.

What are the key opportunities in the foods high in amino acid lysine industry?

Government Nutrition & Food Security Programs

Emerging economies are investing heavily in protein-enrichment programs aimed at combating malnutrition. Public procurement for school meals, maternal nutrition, and defense rations represents a stable, high-volume opportunity for lysine-rich food producers.

Innovation in Fortified & Bio-Enhanced Foods

Advancements in food fortification technologies enable cereal and grain manufacturers to enhance lysine content, addressing amino acid imbalances in carbohydrate-heavy diets. Bioengineered crops and fermentation-derived lysine enrichment create new premium product categories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 389.8 Billion |

| Market Size in 2026 | USD 414.75 Billion |

| Market Size in 2031 | USD 565.58 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Type Insights

Animal-based sources dominate the global lysine-rich foods market, accounting for approximately 61% of the total market share in 2025. The dominance of this segment is primarily driven by high global poultry and dairy consumption, which serve as major dietary protein sources. Poultry remains the largest contributor due to its affordability, short production cycles, scalability, and strong demand across both developed and emerging economies. Additionally, expanding quick-service restaurant chains and processed meat consumption continue to reinforce segment leadership.

Plant-based sources represent nearly 39% of the market share and are the fastest-growing source segment. Growth is driven by rising vegan and flexitarian populations, increasing awareness of sustainable protein production, and environmental concerns associated with animal agriculture. Soy, legumes, lentils, quinoa, and fortified plant-based foods are witnessing significant demand, particularly in North America, Europe, and parts of Asia-Pacific.

Product Form Insights

Fresh and raw foods account for approximately 45% of the total market share, reflecting traditional dietary patterns centered around fresh meat, fish, dairy, and legumes. The leading segment driver is sustained household demand for minimally processed protein sources, particularly in emerging economies where fresh markets dominate food retail.Processed and packaged protein foods are expanding rapidly due to accelerating urbanization, dual-income households, and convenience-driven consumption behavior. Ready-to-eat meals, frozen meat products, and fortified dairy items are gaining popularity in metropolitan areas.Powdered and concentrated protein ingredients are witnessing strong growth in sports nutrition, dietary supplements, and functional food manufacturing. Increasing gym participation, lifestyle diseases, and demand for performance-enhancing nutrition solutions are key factors supporting segment expansion.

Processing Level Insights

Conventional products dominate the market, representing approximately 72% of global market share in 2025. The leading driver for this segment is affordability and well-established global supply chains, making conventional protein products accessible to a broad consumer base across both developed and developing economies.However, organic and fortified protein-rich foods are expanding at faster growth rates. Growth is particularly strong in North America and Europe, where consumers increasingly prioritize clean-label, non-GMO, hormone-free, and nutritionally enhanced food options. Fortification with essential amino acids and micronutrients is gaining traction in preventive healthcare and child nutrition programs.

Distribution Channel Insights

Supermarkets and hypermarkets dominate distribution channels, accounting for approximately 48% of total market share. The leading driver for this segment is strong organized retail penetration and the availability of diversified protein product portfolios under one roof. Bulk purchasing options and private-label protein brands further support sales growth.Online retail is the fastest-growing distribution channel, supported by rapid digitalization, subscription-based protein food deliveries, and expansion of e-commerce grocery platforms. Direct-to-consumer (DTC) protein brands and fitness-oriented online marketplaces are significantly contributing to channel expansion.

End-Use Insights

Household consumption accounts for approximately 54% of total demand, making it the largest end-use segment. The primary driver is the integral role of lysine-rich foods in daily diets, particularly through meat, dairy, and plant-based staples consumed across global households.Sports and performance nutrition represents the fastest-growing end-use segment, driven by increasing health consciousness, fitness participation, bodybuilding trends, and demand for muscle recovery products.Clinical nutrition applications are expanding steadily due to aging populations, rising chronic disease prevalence, hospital nutrition programs, and growing focus on preventive healthcare strategies worldwide.

Explore more data points, trends and opportunities Download Free Sample Report

Foods High in Amino Acid Lysine Market Segmentations

- Animal-Based Sources

- Plant-Based Sources

By Product Form

- Fresh/Raw Foods

- Frozen Foods

- Processed & Packaged Foods

- Ready-to-Eat (RTE) & Ready-to-Cook (RTC)

- Powdered & Concentrated Protein Ingredients

By Processing Level

- Conventional

- Organic

- Fortified/Lysine-Enhanced Foods

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Online Retail/E-Commerce

- Foodservice (HoReCa)

- Institutional Sales (Hospitals, Schools, Defense)

By End-Use Application

- Household Consumption

- Clinical & Medical Nutrition

- Sports & Performance Nutrition

- Infant & Child Nutrition

- Functional & Fortified Foods Industry

Regional Insights

North America

North America holds approximately 32% of the global market share in 2025, making it the leading regional market. The United States dominates due to high per capita meat and dairy consumption, a mature food processing industry, and a well-established sports nutrition ecosystem. Strong consumer awareness regarding protein quality, widespread availability of fortified foods, and high disposable income levels further support regional demand. Canada contributes significantly through dairy exports, advanced food fortification practices, and government-backed nutrition guidelines that encourage balanced protein intake. Additionally, innovation in plant-based protein alternatives and clean-label product development is accelerating regional growth.

Asia-Pacific

Asia-Pacific accounts for nearly 29% of global market share and is the fastest-growing region, expanding at a 7.8% CAGR. Rapid population growth, rising disposable incomes, and increasing urbanization are key drivers of protein demand across the region. China leads regional consumption due to high soy intake, expanding middle-class dietary shifts toward higher protein consumption, and growing meat production industries. India demonstrates strong growth potential in plant-based lysine-rich foods, supported by vegetarian dietary patterns and increasing demand for fortified staples. Japan emphasizes clinical and functional nutrition integration, driven by an aging population and advanced healthcare awareness. Additionally, Southeast Asian markets are experiencing rising poultry and aquaculture production, further strengthening regional expansion.

Europe

Europe represents approximately 24% of global market share, led by Germany, France, and the United Kingdom. Regional growth is driven by strong plant-based food adoption, stringent food quality regulations, and increasing demand for organic and sustainable protein sources. European consumers prioritize traceability, animal welfare standards, and environmental sustainability, encouraging expansion in certified organic and alternative protein segments. Government initiatives promoting healthier diets and protein diversification further stimulate market growth across both Western and Northern Europe.

Latin America

Latin America accounts for about 9% of global demand, with Brazil and Argentina serving as major production and export hubs for meat and soy. The region benefits from abundant agricultural resources, large-scale livestock farming, and competitive export capabilities. Rising domestic consumption of poultry and beef, combined with expanding food processing infrastructure, is strengthening internal market growth. Increasing urbanization and growing middle-class populations are also contributing to higher protein intake across key economies.

Middle East & Africa

The Middle East & Africa region holds approximately 6% market share. Saudi Arabia and South Africa serve as major demand centers, supported by rising urbanization, expanding retail infrastructure, and government-led nutrition diversification initiatives. Increasing investments in food security programs, growth in poultry production, and rising awareness regarding protein-rich diets are supporting regional demand. Additionally, improving cold chain logistics and expanding supermarket penetration are enhancing product accessibility across emerging African economies.

Key Players in the Foods High in Amino Acid Lysine Market

- Tyson Foods Inc.

- JBS S.A.

- Cargill Incorporated

- Nestlé S.A.

- Danone S.A.

- Hormel Foods Corporation

- BRF S.A.

- Maple Leaf Foods Inc.

- Marfrig Global Foods

- Fonterra Co-operative Group

- Arla Foods

- Lactalis Group

- Beyond Meat Inc.

- Impossible Foods Inc.

- Wilmar International