Foods Containing Sulfites Market Size

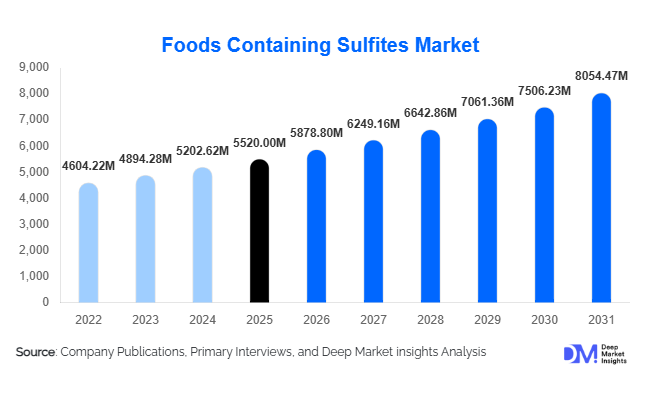

According to Deep Market Insights, the global foods containing sulfites market size was valued at USD 5,520 million in 2025 and is projected to grow from USD 5,878.80 million in 2026 to reach USD 8,054.47 million by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). Market growth is primarily driven by rising consumption of processed foods and beverages, expanding global wine production, and increasing seafood exports requiring preservation solutions to maintain quality and shelf stability.

Sulfites—including sodium metabisulfite, potassium metabisulfite, sodium sulfite, and sulfur dioxide—are widely used as preservatives and antioxidants across alcoholic beverages, dried fruits, processed vegetables, seafood, bakery products, and convenience foods. These compounds help prevent oxidation, discoloration, microbial spoilage, and enzymatic browning, making them essential for large-scale industrial food manufacturing and global food trade.

Key Market Insights

- Alcoholic beverages represent the largest application segment, accounting for approximately 34% of global demand, driven by mandatory stabilization requirements in wine production.

- Powdered sulfites dominate by form, holding nearly 52% market share due to ease of storage, transportation, and industrial dosing efficiency.

- Europe leads the global market, contributing around 32% of total demand, supported by strong wine production in France, Italy, and Spain.

- Asia-Pacific is the fastest-growing region, expanding at over 7% CAGR, fueled by seafood exports and rising processed food consumption.

- Top five manufacturers account for nearly 41% of global market share, indicating moderate industry concentration.

- Clean-label pressures and regulatory compliance requirements are reshaping formulation strategies across premium food segments.

What are the latest trends in the foods containing sulfites market?

Rising Demand from Seafood Export Hubs

The global seafood trade, valued at over USD 180 billion annually, continues to expand, particularly in shrimp and crustaceans. Sodium metabisulfite plays a critical role in preventing melanosis (black spot formation) during storage and transport. Major exporters such as India, Vietnam, Ecuador, and Thailand are increasing processing capacity to meet rising demand from the U.S., EU, and Japan. As cold chain infrastructure improves, sulfite-treated seafood products are traveling longer distances, increasing preservative demand. The growth of aquaculture further strengthens long-term consumption of sulfite-based preservation solutions.

Shift Toward Precision Dosing and Automated Processing

Food manufacturers are increasingly integrating automated sulfite dosing systems to ensure compliance with strict regulatory thresholds. Precision monitoring technologies reduce overuse while maintaining product stability, particularly in wineries and beverage processing plants. Advanced blending and controlled-release sulfite formulations are also emerging, enabling manufacturers to optimize antioxidant performance while addressing consumer safety standards. Digital quality control systems integrated into beverage bottling and seafood processing lines are becoming mainstream in developed markets.

What are the key drivers in the foods containing sulfites market?

Growth in Global Wine Production

Global wine production exceeds 250 million hectoliters annually, with sulfur dioxide and potassium metabisulfite serving as essential stabilizers. Countries such as France, Italy, Spain, the United States, China, Chile, and Australia continue to expand vineyard acreage and export volumes. Sulfites are mandatory in most commercial wine production processes to prevent microbial contamination and oxidation, ensuring stable, long-distance exports. Premiumization of wines in Asia-Pacific further accelerates demand for high-purity sulfite grades.

Expansion of Processed and Packaged Food Consumption

Urbanization, dual-income households, and rising disposable incomes are increasing demand for packaged foods globally. Dried fruits, canned vegetables, bakery mixes, sauces, and ready-to-eat meals rely on sulfites to maintain shelf life and visual quality. Processed food penetration exceeds 60% in developed economies and continues to rise in emerging markets such as India, Indonesia, Brazil, and Mexico, directly supporting sulfite consumption growth.

Seafood Processing and Export Growth

Asia-Pacific dominates global shrimp exports, with India alone accounting for a significant share of U.S. imports. Sodium metabisulfite remains the industry standard for preserving crustaceans during freezing and shipment. Increasing seafood trade volumes and improvements in aquaculture productivity continue to drive stable and predictable demand for sulfite preservatives.

What are the restraints for the global market?

Regulatory Compliance and Labeling Requirements

Food safety authorities in the U.S., EU, Japan, and Australia require mandatory labeling when sulfite content exceeds specified thresholds. Compliance adds operational complexity and monitoring costs. Non-compliance risks product recalls and reputational damage, particularly in export-oriented markets.

Growing Clean-Label Movement

Consumers increasingly prefer “free-from” and natural preservative alternatives. Premium food brands are reformulating products using natural antioxidants such as rosemary extracts and ascorbic acid, limiting sulfite use in certain categories. Although sulfites remain cost-effective and technically superior in many applications, clean-label pressures represent a moderate restraint.

What are the key opportunities in the foods containing sulfites industry?

Emerging Market Food Processing Expansion

Government initiatives such as “Make in India” and China’s food industry modernization programs are driving investment in domestic food processing capacity. Expansion of industrial-scale fruit dehydration, vegetable canning, and beverage production plants presents opportunities for sulfite manufacturers to establish localized production and long-term B2B supply contracts.

Premium Wine and Craft Beverage Growth

The craft wine and specialty beverage segment is expanding in Asia-Pacific and Latin America. High-end producers demand high-purity potassium metabisulfite with consistent quality standards. Suppliers offering customized solutions, small-batch supply flexibility, and automated dosing support can capture premium margins in this segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5520 Million |

| Market Size in 2026 | USD 5878.80 Million |

| Market Size in 2031 | USD 8054.47 Million |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Category Insights

The alcoholic beverages segment dominates the global market, accounting for approximately 34% of total revenue share in 2025. The leading driver for this segment is the extensive use of sulfites in wine production for microbial stabilization, oxidation control, and shelf-life enhancement. Europe’s large-scale viticulture industry and expanding premium wine consumption in North America continue to reinforce demand. Additionally, regulatory acceptance of controlled sulfite usage in alcoholic beverages further supports sustained consumption across developed markets.Dried and processed fruits represent a significant application segment, supported by rising global trade in raisins, apricots, prunes, and other dehydrated fruits. Sulfites are widely used to prevent enzymatic browning and maintain color stability during storage and export. Growth in cross-border dried fruit trade, particularly from Turkey, the United States, and Middle Eastern suppliers, continues to drive volume demand.

Meat and seafood products are the fastest-growing category, expanding at a CAGR of over 7%. The leading growth driver in this segment is the rapid expansion of aquaculture and shrimp exports from Asia-Pacific and Latin America. Sulfites are essential in preventing melanosis (black spot formation) in crustaceans, which directly impacts export quality standards. Increasing global seafood consumption and rising cold chain investments further accelerate this segment’s growth trajectory.Bakery and confectionery applications maintain steady expansion, supported by industrial bread production, dough conditioning, and large-scale commercial baking operations in developed economies. The growth of packaged baked goods and convenience foods across urban markets continues to sustain demand within this segment.

Sulfite Type Insights

Sodium metabisulfite leads the market with nearly 29% share due to its versatility, cost-effectiveness, and broad-spectrum preservative functionality. The primary driver for this segment is its multi-industry applicability across seafood preservation, dried fruit processing, and vegetable dehydration. Its strong antimicrobial and antioxidant properties make it the preferred industrial-grade sulfite.otassium metabisulfite is widely used in wine stabilization and brewing applications. The growing global wine industry, particularly in Europe and the United States, remains the key demand driver for this sulfite type.

Sulfur dioxide continues to serve as a core preservative in beverage processing, particularly in wineries and fruit juice production facilities. Its direct application for microbial control and oxidation prevention sustains stable demand.Sodium sulfite and sodium bisulfite cater to niche industrial food applications, including starch processing and specialty formulations. Although smaller in market share, these variants remain essential in specific controlled processing environments.

Form Insights

Powdered sulfites account for approximately 52% of total market share in 2025. The leading driver for this segment is ease of handling, longer shelf stability, lower transportation costs, and suitability for bulk industrial storage. Powder form is particularly favored in dried fruit processing, bakery manufacturing, and seafood treatment facilities.

Granular sulfites are commonly used in automated industrial blending systems where precise dosing and controlled dissolution are required. Their application is prevalent in large-scale food processing plants with integrated mixing operations.Liquid sulfites are primarily preferred in beverage bottling plants and continuous processing units due to automated injection capabilities. Increasing adoption of automated production lines in wineries and juice processing facilities supports steady growth of this segment.

Distribution Channel Insights

Direct industrial supply dominates the market with approximately 61% share, as large food and beverage manufacturers typically engage in long-term procurement contracts with chemical suppliers. The leading driver for this channel is bulk purchasing efficiency, stable pricing agreements, and regulatory compliance assurance through certified suppliers.Foodservice supply chains represent a smaller yet stable segment, supplying institutional catering operations and commercial kitchens. Growth in hospitality and quick-service restaurants contributes to incremental demand.Retail and private label processors account for growing consumption, particularly in emerging markets where small-scale food manufacturers and regional processors are expanding operations. Increasing domestic food processing capacity in Asia-Pacific and Latin America strengthens this channel.

End-Use Industry Insights

The food processing industry accounts for nearly 48% of overall demand and remains the largest end-use sector. The leading growth driver is the continued expansion of global packaged food consumption, particularly ready-to-eat meals, preserved vegetables, dehydrated ingredients, and processed fruit products. Urbanization, rising disposable incomes, and modern retail penetration significantly contribute to steady growth.The beverage industry is another major contributor, driven primarily by wine production and fruit juice manufacturing. Increasing premium wine exports and rising demand for shelf-stable beverages sustain sulfite usage.

Seafood processing is the fastest-growing end-use segment, expanding at approximately 7.2% CAGR. Export-oriented seafood industries in India, Vietnam, Ecuador, and Thailand significantly influence global demand. Stringent export quality standards and the need to preserve product appearance during long shipping durations act as key growth accelerators.Emerging ready-to-eat meal manufacturers and institutional catering services are also contributing to incremental sulfite consumption, particularly in rapidly urbanizing economies.

Explore more data points, trends and opportunities Download Free Sample Report

Foods Containing Sulfites Market Segmentations

By Product Category

- Alcoholic Beverages

- Non-Alcoholic Beverages

- Dried & Processed Fruits

- Processed Vegetables

- Bakery & Confectionery

- Convenience & Ready-to-Eat Foods

By Sulfite Type

- Sodium Sulfite

- Sodium Bisulfite

- Sodium Metabisulfite

- Potassium Metabisulfite

- Sulfur Dioxide

By Form

- Powder

- Granular

- Liquid

By Distribution Channel

- Direct Industrial Supply (B2B)

- Foodservice Supply Chains

- Retail & Private Label Processors

By End-Use Industry

- Food Processing Industry

- Beverage Industry

- Seafood Processing Industry

- Institutional Catering

Regional Insights

Europe

Europe holds approximately 32% of global market share in 2025, making it the largest regional market. The primary growth driver is the region’s strong wine production base in France, Italy, and Spain, where sulfites are essential for fermentation control and preservation. Germany and the U.K. contribute significantly through high processed food imports and dried fruit consumption.Additionally, Europe benefits from well-established food export industries and strict quality regulations that standardize preservative usage. Although regulatory frameworks are stringent, consistent demand from premium wine exports and value-added food processing ensures stable regional growth.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of the global market and is the fastest-growing region, expanding at over 7% CAGR. The leading driver is rapid industrialization of food processing industries in China and India, supported by rising domestic consumption of packaged foods.Vietnam and Thailand are major contributors due to strong seafood export industries, while India’s shrimp exports significantly boost sulfite demand. Japan remains a high-value importer of sulfite-treated seafood and processed foods. Expanding cold chain infrastructure and increasing foreign direct investment in food manufacturing further accelerate regional expansion.

North America

North America represents about 24% of global demand, with the United States accounting for nearly 20% alone. Growth is driven by California’s large-scale wine production, strong processed food consumption patterns, and high seafood import volumes.The region also benefits from advanced food safety systems and large integrated food manufacturers that rely on stable preservative inputs. Rising demand for convenience foods and ready-to-eat meals further sustains consumption.

Latin America

Latin America contributes approximately 9% of the global market share. Chile’s expanding wine exports serve as the primary regional growth driver. Additionally, Brazil’s growing processed food sector and Ecuador’s shrimp export industry significantly support sulfite consumption.Increasing agricultural exports and modernization of food processing facilities are expected to strengthen long-term regional demand.

Middle East & Africa

The Middle East & Africa region holds nearly 6% market share. South Africa leads regional demand due to its well-established wine production industry. Gulf Cooperation Council (GCC) countries drive growth through high import dependence on processed and packaged foods.Rising urbanization, expanding retail chains, and increasing food import volumes continue to create moderate but stable demand growth across the region.