Foods Containing Complete Protein Market Size

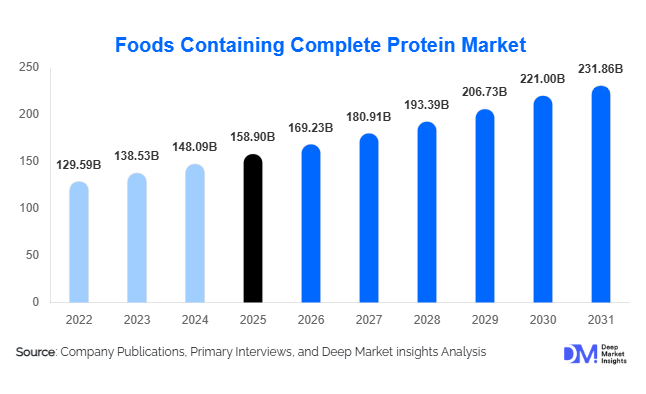

According to Deep Market Insights,the global foods containing complete protein market size was valued at USD 158.9 billion in 2025 and is projected to grow from USD 169.23 billion in 2026 to reach USD 231.86 billion by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer awareness of balanced amino acid intake, increasing demand for high-protein diets, expansion of plant-based complete protein innovations, and the growing role of protein in preventive healthcare and active lifestyles.

Key Market Insights

- Animal-based protein foods dominate globally, accounting for nearly 68% of total market share in 2025, led by dairy, eggs, poultry, and seafood consumption.

- Plant-based complete proteins are the fastest-growing segment, expanding at over 9% CAGR due to sustainability and flexitarian diet trends.

- North America holds approximately 35% market share in 2025, supported by strong sports nutrition and functional food adoption.

- Asia-Pacific is the fastest-growing regional market, driven by rising middle-class income and government nutrition initiatives.

- Fortified and functional packaged foods account for 34% of product demand, particularly protein bars and ready-to-drink beverages.

- E-commerce sales now represent nearly 18% of global revenue, reshaping distribution strategies and direct-to-consumer models.

What are the latest trends in the foods containing complete protein market?

Plant-Based Amino Acid Optimization

Manufacturers are increasingly developing blended plant protein formulations to achieve complete amino acid profiles comparable to animal-based proteins. Innovations combining pea, rice, soy, quinoa, and hemp proteins are improving digestibility scores (DIAAS/PDCAAS) and taste profiles. Fermentation technologies and precision nutrition approaches are further enhancing bioavailability. This trend is accelerating particularly in Europe and North America, where sustainability concerns are influencing consumer purchase decisions.

Mainstream Protein Fortification Across Everyday Foods

Protein fortification is no longer limited to sports supplements. Breakfast cereals, bakery items, snacks, frozen meals, and beverages are being reformulated to include complete protein claims. Retailers are expanding high-protein product shelves, and brands are targeting general households rather than niche athletic communities. Clinical nutrition and senior-focused formulations are also gaining prominence, especially in developed economies with aging populations.

What are the key drivers in the foods containing complete protein market?

Rising Health and Fitness Awareness

Consumers worldwide are increasingly prioritizing muscle maintenance, metabolic health, and weight management. Gym memberships, home fitness programs, and sports participation have significantly increased protein intake awareness. Sports and fitness nutrition remains one of the fastest-growing end-use segments, driving premium product adoption and innovation in ready-to-consume formats.

Aging Global Population

The rising population aged above 60 years is accelerating demand for protein-rich diets to combat sarcopenia and muscle loss. Clinical nutrition and fortified dairy products are expanding rapidly, particularly in Japan, Germany, and the United States. Medical recommendations supporting higher protein intake among seniors are strengthening long-term demand stability.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in dairy, soybean, poultry, and quinoa prices impact production costs and profit margins. Climate variability, supply chain disruptions, and trade barriers can create pricing instability, particularly for export-driven markets.

Clean Label and Processing Concerns

Consumers increasingly scrutinize ingredient lists, especially in ultra-processed protein snacks and beverages. Reformulation to meet clean-label standards often increases production costs and regulatory compliance complexity.

What are the key opportunities in the foods containing complete protein industry?

Government Nutrition Programs and Institutional Demand

Governments across Asia and Africa are promoting protein sufficiency through school meal programs and food fortification initiatives. Public procurement contracts offer large-scale volume opportunities for manufacturers. Institutional demand from hospitals, military programs, and elderly care facilities is expanding steadily.

Personalized and Functional Nutrition

AI-driven dietary planning and subscription-based nutrition platforms are enabling customized protein solutions for athletes, seniors, and patients. Companies investing in tailored amino acid formulations and direct-to-consumer channels can capture higher-margin segments and improve customer retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 158.9 Billion |

| Market Size in 2026 | USD 169.23 Billion |

| Market Size in 2031 | USD 231.86 Billion |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Type Insights

Animal-based complete protein foods dominate the global market, accounting for approximately 68% share in 2025. The segment’s leadership is primarily driven by superior amino acid profiles, high bioavailability, and strong consumer trust in traditional protein sources. Dairy products represent the largest sub-segment, supported by widespread global consumption, expanding fortified dairy portfolios, and established processing infrastructure. The growing popularity of high-protein yogurt, cheese snacks, and whey-based beverages further reinforces segment dominance. Poultry and seafood follow closely, benefiting from rising global protein intake, expanding quick-service restaurant penetration, and increasing awareness of lean protein diets.

Plant-based complete proteins, although smaller in overall share, are the fastest-expanding source segment, projected to grow at a CAGR exceeding 9% through the forecast period. Growth is primarily driven by sustainability commitments, environmental concerns related to animal agriculture, and the global shift toward flexitarian and vegan lifestyles. Innovation in soy, pea, quinoa, and blended plant protein formulations is enhancing amino acid completeness and sensory appeal, accelerating adoption across developed markets such as Europe and North America.

Product Format Insights

Fortified and functional packaged foods account for nearly 34% of the global market in 2025, making them the leading product format. The segment’s growth is driven by increasing consumer demand for convenience, on-the-go nutrition, and performance-oriented dietary solutions. Protein bars and ready-to-drink (RTD) beverages lead within this category due to portability, extended shelf life, and alignment with active and time-constrained lifestyles. Additionally, product innovation in flavor profiles, sugar reduction, and clean-label formulations continues to expand consumer penetration.

Whole food protein sources remain significant, particularly across emerging economies where minimally processed dietary patterns prevail. Rising awareness of natural protein sources, combined with affordability and cultural dietary preferences, sustains demand for fresh dairy, eggs, legumes, and meat products in these markets.

Distribution Channel Insights

Supermarkets and hypermarkets hold approximately 52% share of global distribution in 2025, supported by organized retail expansion, wide product assortments, and strong private-label penetration. The ability to offer diversified protein categories under one roof enhances consumer accessibility and impulse purchases. Strategic shelf positioning and in-store promotions further strengthen this channel’s dominance.

Online retail is the fastest-growing distribution channel, currently capturing nearly 18% market share. Growth is fueled by subscription-based nutrition models, direct-to-consumer (DTC) brand strategies, digital marketing engagement, and expanding e-commerce penetration in Asia-Pacific and North America. Personalized nutrition platforms and targeted online promotions are further accelerating digital channel adoption.

End-Use Insights

Household consumption accounts for approximately 46% of total demand, reflecting the mainstream integration of complete protein foods into daily diets. Rising health awareness, weight management trends, and preventive healthcare focus are key drivers supporting this segment’s leadership.

The sports and fitness nutrition segment is the fastest-growing end-use category, expanding at an estimated CAGR of 8.5%. Growth is driven by increasing gym memberships, athletic participation, influencer-driven marketing, and demand for muscle recovery and performance-enhancing nutrition. Expanding female participation in fitness activities is also broadening the consumer base.Clinical and infant nutrition segments are witnessing steady expansion, supported by hospital procurement systems, aging populations, rising chronic disease prevalence, and stringent pediatric dietary standards that emphasize high-quality complete protein intake.

Explore more data points, trends and opportunities Download Free Sample Report

Foods Containing Complete Protein Market Segmentations

By Source Type

- Animal-Based Complete Protein Foods

- Plant-Based Complete Protein Foods

By Product Format

- Whole Foods

- Fortified & Functional Packaged Foods

- Frozen & Ready Meals

- Bakery & Confectionery Products

- Infant & Clinical Nutrition Products

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health & Nutrition Stores

- Online Retail & E-commerce

- Institutional & Foodservice Channels

By End-Use

- Household Consumption

- Sports & Fitness Nutrition

- Clinical & Medical Nutrition

- Infant & Child Nutrition

- Foodservice & HORECA

Regional Insights

North America

North America accounts for nearly 35% of the global market in 2025, making it the leading regional contributor. The United States represents over 80% of regional demand, driven by high consumer awareness regarding protein intake, strong penetration of sports nutrition products, and advanced dairy and food processing infrastructure. Growth is further supported by clean-label trends, premium protein innovations, and widespread availability of plant-based alternatives. Increasing demand for personalized and functional nutrition continues to strengthen market expansion.

Europe

Europe holds approximately 27% market share, with Germany, France, and the United Kingdom leading consumption. Regional growth is primarily driven by rising plant-based protein innovation, regulatory support for protein labeling transparency, and sustainability certifications. The European Green Deal and carbon reduction commitments are accelerating the shift toward alternative protein sources. Additionally, high dairy consumption in Western Europe sustains demand for traditional complete protein products.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 8.2% CAGR during the forecast period. China and India serve as major growth engines due to rising disposable incomes, rapid urbanization, and expanding middle-class populations. Government-led nutrition programs and school feeding initiatives further stimulate protein demand. Japan remains a strong clinical nutrition market, where aging demographics and increased healthcare spending drive adoption of high-quality protein supplements and fortified foods.

Latin America

Brazil and Mexico dominate regional demand, supported by well-established poultry and dairy industries. Growth is driven by rising domestic consumption of animal protein, improving retail infrastructure, and export-oriented dairy production. Increasing sports participation and expanding middle-income households further contribute to protein product demand across the region.

Middle East & Africa

The Middle East & Africa region demonstrates steady growth, with Gulf Cooperation Council (GCC) countries recording high per capita protein intake due to strong purchasing power and premium food imports. In Africa, market expansion is supported by international nutrition intervention programs, fortified food initiatives, and increasing urbanization. Government-backed food security programs and expanding modern retail networks are further contributing to long-term regional growth.

Key Players in the Foods Containing Complete Protein Market

- Nestlé S.A.

- Danone S.A.

- Tyson Foods Inc.

- Cargill Incorporated

- Archer Daniels Midland Company

- Glanbia plc

- Fonterra Co-operative Group

- Lactalis Group

- Hormel Foods Corporation

- Maple Leaf Foods Inc.

- Otsuka Holdings Co., Ltd.

- Kellogg Company

- General Mills Inc.

- BRF S.A.

- Arla Foods