Food Waste Management Market Size

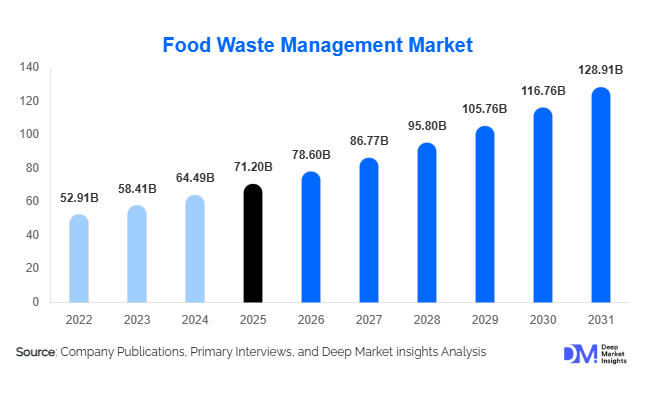

According to Deep Market Insights, the global food waste management market size was valued at USD 71.2 billion in 2025 and is projected to grow from USD 78.60 billion in 2026 to reach USD 128.91 billion by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The food waste management market growth is primarily driven by increasing global emphasis on circular economy practices, stricter landfill diversion regulations, rising investments in renewable bioenergy infrastructure, and growing adoption of sustainable waste processing technologies across industrial and municipal sectors.

Key Market Insights

- Governments worldwide are implementing organic waste diversion mandates, accelerating adoption of composting and anaerobic digestion solutions.

- Anaerobic digestion and waste-to-energy technologies are gaining prominence as food waste becomes a key feedstock for renewable energy generation.

- Europe dominates the global market due to strict environmental regulations and advanced recycling infrastructure.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization and expanding municipal waste programs in China and India.

- Commercial food service and food processing industries generate the largest waste volumes, creating strong demand for integrated waste services.

- Digital technologies such as AI-based waste monitoring and smart collection systems are improving operational efficiency and cost optimization.

What are the latest trends in the food waste management market?

Circular Economy and Resource Recovery Models

The industry is transitioning from traditional waste disposal toward circular economy frameworks where food waste is converted into valuable outputs such as biogas, fertilizers, and bio-based chemicals. Municipalities and corporations are increasingly prioritizing resource recovery rather than landfill disposal. Waste processors are integrating energy recovery facilities that transform organic waste into renewable electricity and biomethane. This trend aligns with global carbon neutrality targets and corporate ESG commitments, enabling companies to monetize waste streams while reducing environmental impact. Partnerships between retailers, food manufacturers, and waste processors are expanding to create closed-loop systems that maximize resource utilization.

Digitalization and Smart Waste Management

Technology adoption is reshaping operational efficiency across the food waste management ecosystem. IoT-enabled smart bins, AI-powered waste analytics, and automated sorting systems are improving waste segregation accuracy and reducing collection costs. Businesses are deploying real-time monitoring platforms to track food waste generation, enabling predictive logistics and compliance reporting. Cloud-based analytics solutions help restaurants and retailers reduce food losses upstream while optimizing waste processing downstream. These innovations are attracting technology providers and startups into the market, transforming waste management into a data-driven service industry.

What are the key drivers in the food waste management market?

Stringent Environmental Regulations

Governments across Europe, North America, and parts of Asia have introduced regulations restricting landfill disposal of organic waste. Mandatory waste segregation policies and carbon emission reduction targets are compelling municipalities and corporations to adopt structured food waste processing solutions. Regulatory compliance has become one of the strongest drivers of investment in composting and anaerobic digestion facilities worldwide.

Growth of Food Service and Retail Industries

The rapid expansion of supermarkets, quick-service restaurants, and online food delivery platforms has significantly increased food waste generation. Organized food supply chains require professional waste handling to maintain hygiene standards and regulatory compliance. As food consumption rises globally, structured waste collection and treatment services are becoming operational necessities, driving sustained market demand.

What are the restraints for the global market?

High Infrastructure Investment Requirements

Establishing advanced waste treatment facilities such as anaerobic digestion plants requires substantial capital expenditure. Smaller municipalities and developing economies often face funding constraints, slowing infrastructure deployment despite rising waste volumes.

Inefficient Waste Segregation at Source

Improper segregation of organic waste reduces processing efficiency and increases operational costs. Lack of consumer awareness and inconsistent collection systems in emerging markets remain significant barriers to achieving optimal recycling and recovery outcomes.

What are the key opportunities in the food waste management industry?

Expansion of Waste-to-Energy Infrastructure

Food waste is increasingly recognized as a reliable renewable energy feedstock. Investments in anaerobic digestion facilities present strong opportunities for operators to generate revenue through electricity, biomethane, and fertilizer production. Government incentives supporting renewable energy projects further enhance investment attractiveness, particularly in Asia-Pacific and Latin America where infrastructure penetration remains low.

Smart Waste Analytics and Integrated Service Platforms

The integration of digital monitoring systems into waste management services enables companies to offer predictive collection, sustainability reporting, and operational optimization. Businesses adopting data-driven waste reduction strategies create recurring revenue opportunities for technology-enabled service providers. This segment is expected to grow rapidly as corporations prioritize ESG compliance and cost efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 71.20 Billion |

| Market Size in 2026 | USD 78.60 Billion |

| Market Size in 2031 | USD 128.91 Billion |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

The food waste management market demonstrates strong diversification across waste generation sources, with industrial food processing facilities emerging as the dominant contributor, accounting for nearly 29% of the global market share. The leading position of this segment is primarily driven by continuous large-scale organic waste generation from food manufacturing, beverage processing, dairy operations, and packaged food production plants. These facilities generate predictable and homogeneous waste streams, making them highly suitable for advanced treatment technologies such as anaerobic digestion and bio-conversion processes. Increasing regulatory pressure on industrial emissions and waste disposal practices, along with corporate sustainability commitments and ESG reporting requirements, are further encouraging manufacturers to adopt structured waste management solutions. Additionally, rising investments in circular economy models are enabling industrial operators to convert waste into valuable by-products such as biogas, fertilizers, and bio-based chemicals, reinforcing segment dominance.Commercial food service establishments, including hotels, restaurants, catering services, and quick-service chains, represent another major source segment due to growing compliance requirements related to food safety and hygiene standards. The expansion of organized food service sectors across urban economies has significantly increased daily organic waste volumes, prompting businesses to outsource waste handling to specialized service providers. Digital waste tracking systems and sustainability certification programs are also encouraging restaurants and hospitality operators to adopt efficient waste diversion strategies.Residential food waste generation is witnessing steady expansion, supported by rapid urbanization, changing consumption patterns, and rising household food consumption levels. Government-led awareness campaigns promoting waste segregation at source and composting initiatives are strengthening residential participation in waste management ecosystems. Meanwhile, institutional waste generated by hospitals, universities, and public facilities is growing as structured sustainability policies and green campus initiatives gain traction globally, contributing to stable long-term demand for organized waste treatment services.

Treatment Method Insights

Anaerobic digestion remains the leading treatment method, accounting for approximately 31% of global market share, supported by its ability to simultaneously reduce organic waste volumes while generating renewable energy in the form of biogas and biomethane. The leading growth driver for this segment is the increasing global transition toward renewable energy systems and carbon reduction targets, which position anaerobic digestion as both a waste management and energy production solution. Governments and private investors are increasingly supporting biogas infrastructure through subsidies, feed-in tariffs, and renewable gas integration programs, making this technology economically attractive for municipalities and industrial operators.Composting continues to maintain widespread adoption, particularly within municipal waste management programs, due to its relatively low capital investment requirements and operational simplicity. The method plays a critical role in supporting sustainable agriculture by producing nutrient-rich compost that enhances soil fertility and reduces dependence on synthetic fertilizers. Increasing consumer demand for organic farming practices and regenerative agriculture is further strengthening compost utilization globally.Waste-to-biofuel processing is emerging as a high-growth treatment segment as industries seek alternative low-carbon fuels. Technological advancements in biochemical conversion and fermentation processes are enabling food waste to be transformed into ethanol, biodiesel, and sustainable aviation fuel precursors. This transition aligns with global decarbonization strategies across transportation and industrial sectors, positioning biofuel production as a strategic future opportunity.Landfill disposal continues to decline steadily worldwide as environmental regulations tighten and landfill taxation policies increase operational costs. Many governments are implementing landfill bans on organic waste, accelerating the shift toward resource recovery-based treatment methods and reinforcing market transformation toward sustainable waste processing technologies.

Service Model Insights

Integrated waste management solutions lead the market with nearly 33% share, driven primarily by organizations’ growing preference for end-to-end service providers capable of managing collection, transportation, treatment, compliance reporting, and resource recovery within a single operational framework. The leading driver for this segment is the rising complexity of environmental regulations and sustainability reporting requirements, which encourage businesses to partner with specialized providers offering comprehensive waste lifecycle management. Integrated solutions also improve operational efficiency, cost optimization, and traceability, making them increasingly attractive for multinational food companies and large retail chains.Municipal waste services remain a foundational component of the market, particularly in developed economies where established public waste infrastructure ensures consistent service delivery. Governments are increasingly modernizing municipal systems through smart waste monitoring technologies and public-private partnerships aimed at improving diversion rates and operational efficiency.On-site processing solutions are gaining significant traction among large food manufacturers and distribution centers seeking to minimize transportation costs, reduce carbon emissions, and improve waste handling autonomy. Advances in compact digestion and composting equipment are enabling decentralized waste treatment, allowing companies to convert waste into energy or soil amendments directly at production facilities.

End-Use Insights

Energy generation represents the fastest-growing end-use application within the food waste management market, driven by accelerating global demand for renewable energy sources and biomethane production. The leading driver for this segment is the increasing integration of organic waste-derived gas into national energy grids and transportation fuel systems. Governments worldwide are recognizing food waste as a valuable bioenergy resource, supporting investments in waste-to-energy infrastructure and renewable gas certification programs.Agricultural applications continue to hold a significant share as compost and digestate products derived from treated food waste improve soil structure, enhance nutrient availability, and support sustainable farming practices. Rising concerns regarding soil degradation and chemical fertilizer dependency are encouraging farmers to adopt organic soil amendments, strengthening demand for recycled waste outputs.Industrial bio-product manufacturing is emerging as a promising application area, utilizing food waste as feedstock for biodegradable plastics, enzymes, organic acids, and specialty chemicals. Innovations in biotechnology and bio-refining processes are enabling higher-value utilization pathways, transforming food waste into a strategic industrial resource.Export-driven food manufacturing hubs, particularly across Asia and Latin America, are also contributing to growing demand for scalable waste treatment infrastructure as companies seek compliance with international sustainability standards and supply chain environmental requirements.

Explore more data points, trends and opportunities Download Free Sample Report

Food Waste Management Market Segmentations

By Source

- Residential Food Waste

- Commercial Food Service Waste

- Food Processing & Manufacturing Waste

- Retail & Supermarket Waste

- Institutional Waste

By Treatment Method

- Anaerobic Digestion

- Composting

- Waste-to-Energy Incineration

- Animal Feed Conversion

- Landfill Disposal

- Biofuel & Biochemical Processing

By Service Type

- Collection Services

- Transportation & Logistics

- Processing & Treatment Services

- Integrated Waste Management Solutions

- On-site Waste Management Systems

By End Use

- Energy Generation

- Agricultural Fertilizers & Soil Amendments

- Industrial Bio-Products

- Municipal Waste Management Programs

- Animal Feed Production

Regional Insights

North America

North America accounts for nearly 28% of global market share, supported by advanced waste management infrastructure and strong regulatory enforcement across the United States and Canada. Regional growth is primarily driven by landfill diversion mandates, renewable energy incentives, and corporate sustainability commitments among large food producers and retailers. The United States leads regional demand due to significant investments in anaerobic digestion facilities and renewable natural gas production, supported by federal and state-level clean energy policies. Increasing adoption of ESG frameworks and carbon accounting practices among corporations is further accelerating outsourcing of food waste management services. Additionally, rising consumer awareness regarding food waste reduction and expanding organic waste collection programs across major metropolitan areas continue to strengthen market expansion.

Europe

Europe holds approximately 30% of global market share and represents the most mature regional market due to comprehensive environmental legislation and strong circular economy adoption. Growth across the region is driven by mandatory organic waste separation policies, landfill restrictions, and ambitious climate neutrality targets established by the European Union. Countries such as Germany, France, the United Kingdom, Italy, and the Netherlands have implemented structured collection systems supported by government subsidies for biogas and compost production. Increasing investments in bioenergy infrastructure, combined with strong public participation in waste segregation programs, are reinforcing market stability. Furthermore, Europe’s leadership in sustainable agriculture and renewable energy integration continues to support long-term demand for advanced food waste treatment technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at over 12.5% CAGR, driven by rapid urbanization, rising food consumption, and increasing pressure on landfill capacity. China leads regional growth through large-scale infrastructure investments under environmental modernization and waste reduction initiatives aimed at improving urban sustainability. India is expanding municipal composting programs and nationwide waste segregation campaigns supported by government cleanliness missions and smart city projects. Japan and South Korea maintain highly advanced recycling ecosystems characterized by strict regulatory frameworks, high public compliance, and technological innovation in waste processing. Growing middle-class populations, expanding food processing industries, and increasing renewable energy adoption across Southeast Asia are further accelerating regional demand.

Latin America

Latin America is emerging as a high-potential market led by Brazil and Mexico, where expanding food processing industries and urban population growth are increasing organic waste volumes. Regional growth is supported by improving municipal waste infrastructure, rising environmental awareness, and increasing collaboration between governments and private operators through public-private partnership models. Investments in composting and anaerobic digestion facilities are gaining momentum as cities seek cost-effective solutions to reduce landfill dependency. Additionally, agricultural economies across the region are creating strong demand for compost and organic fertilizers derived from food waste, strengthening circular resource utilization.

Middle East & Africa

The Middle East & Africa region is witnessing gradual yet significant development in food waste management driven by urban expansion, sustainability commitments, and diversification strategies beyond oil-dependent economies. Gulf countries, particularly the UAE and Saudi Arabia, are investing heavily in waste-to-energy and large-scale treatment facilities to reduce landfill reliance and achieve national sustainability targets. Mega-city development projects and tourism expansion are increasing waste generation, creating opportunities for advanced waste processing solutions. Across Africa, adoption is supported by international development funding, climate-focused initiatives, and growing urban populations demanding structured waste management systems. Increasing partnerships with global technology providers and rising awareness of resource recovery benefits are expected to accelerate regional market maturity over the coming years.

Key Players in the Food Waste Management Market

- Veolia Environment S.A.

- Suez S.A.

- Waste Management Inc.

- Republic Services Inc.

- Clean Harbors Inc.

- Covanta Holding Corporation

- Biffa plc

- Remondis SE & Co. KG

- Stericycle Inc.

- FCC Environment

- Renewi plc

- Hitachi Zosen Corporation

- Paprec Group

- GFL Environmental Inc.

- Cleanaway Waste Management Ltd.