Food Ultrasound Market Size

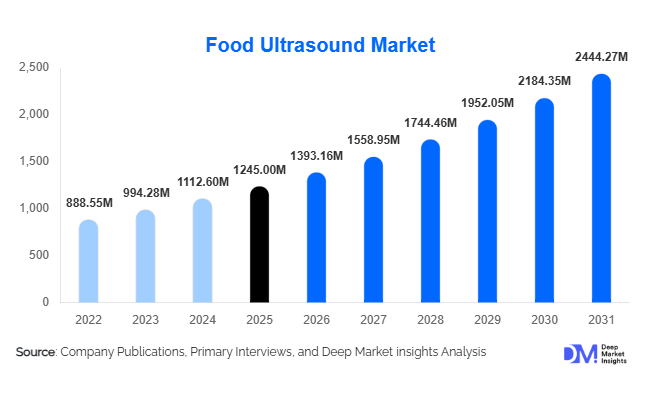

According to Deep Market Insights, the global food ultrasound market size was valued at USD 1,245 million in 2026 and is projected to grow from USD 1,393.16 million in 2026 to reach USD 2,444.27 million by 2031, expanding at a CAGR of 11.9% during the forecast period (2026–2031). The food ultrasound market growth is primarily driven by increasing adoption of non-thermal and energy-efficient food processing technologies, rising demand for minimally processed and clean-label foods, and expanding application of ultrasound-assisted extraction and emulsification across the global food industry.

Key Market Insights

- High-intensity ultrasound dominates industrial applications, being widely used for emulsification, microbial reduction, and bioactive extraction, particularly in dairy and beverage processing.

- Continuous processing systems are increasingly preferred, offering automated inline integration, efficiency gains, and reduced processing times for large-scale manufacturers.

- Dairy processing leads end-use adoption, with ultrasound enhancing homogenization, shelf-life, and nutritional preservation.

- Asia-Pacific is the fastest-growing region, driven by increasing food exports from China and India and rising adoption of smart food-processing technologies.

- Europe maintains strong market share, fueled by strict food safety regulations and clean-label policies that encourage ultrasound adoption.

- Technological integration, including AI monitoring and process analytics, is accelerating adoption and providing real-time quality assurance in production lines.

What are the latest trends in the food ultrasound market?

Non-Thermal and Energy-Efficient Processing

Food ultrasound technology is increasingly being deployed as a non-thermal alternative to traditional heat-based processing. High-intensity ultrasound enables microbial inactivation, emulsification, and extraction without significant temperature rise, preserving nutritional and sensory qualities. Manufacturers are leveraging this technology to produce clean-label foods and functional beverages with extended shelf life, while simultaneously reducing energy consumption by 20–40%. Continuous systems are gaining traction, enabling inline integration and supporting Industry 4.0 automation trends.

Integration with Smart Manufacturing

Emerging trends include AI-enabled ultrasound systems for real-time process monitoring, inline quality inspection, and predictive analytics. Smart factories are incorporating ultrasound sensors to measure viscosity, detect crystallization, and optimize extraction efficiency. These technological enhancements allow manufacturers to reduce waste, improve yields, and ensure consistent product quality. Digitalization also facilitates compliance with strict food safety regulations, particularly in Europe and North America.

What are the key drivers in the food ultrasound market?

Rising Demand for Clean-Label and Nutritionally Preserved Foods

Consumers are increasingly demanding minimally processed foods that retain natural nutrients and flavors. Ultrasound processing preserves protein, vitamins, and bioactive compounds better than conventional thermal methods, driving adoption in dairy, beverages, and functional foods. This trend is particularly strong in health-conscious markets and export-oriented food sectors.

Energy and Process Efficiency Goals

Food manufacturers are under pressure to reduce operational costs and energy consumption. Ultrasound systems lower energy requirements, shorten processing times, and enhance product yield. These benefits align with corporate sustainability goals and regulatory mandates, further driving market growth globally.

Expansion of Functional Foods and Bioactive Extraction

Ultrasound-assisted extraction improves yields of antioxidants, essential oils, proteins, and nutraceutical compounds. The growing functional foods sector, driven by preventive healthcare trends and aging populations, relies on such efficient extraction techniques. Manufacturers increasingly adopt ultrasound to reduce solvent usage and enhance sustainability, creating a key driver for market growth.

What are the restraints for the global market?

High Capital Expenditure

Industrial ultrasound equipment requires significant upfront investment, including specialized transducers, reactors, and integration engineering. High initial costs can be a barrier for small and medium-sized food manufacturers, limiting wider adoption despite operational benefits.

Lack of Standardized Processing Protocols

Many food categories still lack standardized industrial guidelines for ultrasound processing. Variability in processing parameters and limited regulatory validation for new applications slow adoption, particularly in conservative manufacturing sectors concerned with scalability and compliance.

What are the key opportunities in the food ultrasound industry?

Growth of Non-Thermal Processing Applications

There is significant opportunity to expand ultrasound technology across non-thermal preservation, microbial inactivation, and product texture enhancement. With global consumers prioritizing clean-label foods, manufacturers can leverage ultrasound to replace chemical preservatives and traditional heat-based processes, creating new market openings.

Functional Food and Nutraceutical Manufacturing

Ultrasound-assisted extraction of bioactives, proteins, and plant-based compounds offers opportunities for manufacturers of functional foods, beverages, and nutraceuticals. Reduced solvent usage, higher yields, and better retention of nutrients position ultrasound as a key enabling technology for next-generation functional food products.

Smart Factory and Automation Integration

Integrating ultrasound with AI, IoT, and Industry 4.0 manufacturing platforms presents a major opportunity. Real-time monitoring, inline quality assurance, and predictive analytics can improve efficiency and reduce production losses. Companies offering modular, sensor-integrated ultrasound systems stand to gain significant adoption among modern food processors.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1245 Million |

| Market Size in 2026 | USD 1393.16 Million |

| Market Size in 2031 | USD 2444.27 Million |

| CAGR | 11.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The food ultrasound market is primarily driven by the widespread adoption of high-intensity ultrasound systems, which dominate global demand due to their direct applicability in industrial-scale food processing operations. High-intensity ultrasound enables efficient emulsification, homogenization, cell disruption, and microbial reduction, making it highly suitable for improving processing efficiency while maintaining product quality. The leading segment driver for high-intensity systems is the growing industry requirement for energy-efficient processing technologies capable of enhancing texture stability, improving dispersion uniformity, and reducing reliance on chemical additives. Food manufacturers increasingly prefer these systems as they support clean-label formulation trends while simultaneously improving production throughput.Low-intensity ultrasound and hybrid systems are gaining traction across analytical monitoring, quality assessment, and process optimization applications. These technologies are particularly valuable in pilot-scale innovation environments and research-driven functional food production, where precision measurement and process validation are critical. Hybrid ultrasound solutions combining thermal and non-thermal processing methods are also emerging as flexible technologies that enable manufacturers to optimize processing parameters without compromising nutritional integrity.From an operational perspective, continuous inline ultrasound systems are increasingly preferred for large-scale industrial applications because they integrate seamlessly into automated production lines, enabling real-time processing with minimal downtime. However, batch systems remain relevant for specialty food manufacturers, small-scale processors, and product development laboratories where flexibility and controlled experimentation are prioritized. The growing transition toward Industry 4.0-enabled food factories is further accelerating demand for scalable inline ultrasound configurations.

Application Insights

Emulsification and homogenization represent the leading application segment globally, supported by expanding demand for dairy alternatives, plant-based beverages, protein-enriched drinks, and functional liquid formulations. The primary growth driver for this segment is the increasing need for stable emulsions with improved mouthfeel, enhanced nutrient bioavailability, and longer shelf life without synthetic stabilizers. Ultrasound technology enables finer particle size reduction compared to conventional mechanical methods, resulting in superior product consistency and improved consumer acceptance.Extraction of bioactive compounds is one of the fastest-growing applications, particularly within functional foods, nutraceuticals, and natural ingredient processing. Ultrasound-assisted extraction improves yield efficiency while reducing solvent usage and processing time, aligning with sustainability objectives and regulatory preferences for environmentally responsible processing techniques. Manufacturers are increasingly adopting ultrasound to extract antioxidants, proteins, essential oils, and plant-derived functional ingredients used in health-oriented food products.Emerging applications such as ultrasound-assisted microbial inactivation, drying enhancement, and texture modification are gaining momentum as regulatory agencies emphasize food safety and shelf-life extension. These technologies allow producers to reduce thermal intensity during processing, thereby preserving sensory attributes and nutritional value. As consumer demand shifts toward minimally processed foods, ultrasound-supported non-thermal processing is expected to become a critical innovation area across multiple food categories.

Distribution Channel Insights

Direct OEM sales account for the dominant share of distribution channels, particularly among large industrial food processors that require customized equipment configurations and long-term service agreements. The leading driver for this segment is the increasing complexity of food processing systems, which necessitates close collaboration between equipment manufacturers and end users during installation, calibration, and operational optimization. Direct procurement also enables manufacturers to integrate ultrasound technology into existing automated production environments more efficiently.Engineering procurement contractors (EPCs) and food processing system integrators play a crucial intermediary role, especially for mid-sized manufacturers undergoing facility upgrades or capacity expansion projects. These partners provide turnkey solutions by combining ultrasound systems with broader processing infrastructure, accelerating adoption among companies seeking modernization without internal engineering expertise.Digital platforms offering technical consulting, remote diagnostics, retrofitting solutions, and installation support are emerging as influential distribution channels. The expansion of digital service ecosystems allows equipment suppliers to reach geographically dispersed customers while reducing implementation timelines. This shift toward digitally enabled service delivery is supporting faster adoption rates in developing food processing markets.

End-Use Industry Insights

Dairy processing remains the largest end-use industry, accounting for over 26% of global market demand. The leading driver of this segment is the industry's ongoing focus on improving homogenization efficiency, protein dispersion, and microbial stability while lowering energy consumption. Ultrasound technology supports advanced dairy formulations, including lactose-free products, fortified milk, and high-protein beverages, enabling producers to meet evolving nutritional trends.Beverage processing represents one of the fastest-growing end-use categories, driven by rising consumption of functional beverages, plant-based drinks, and ready-to-drink nutritional products. Ultrasound enhances flavor infusion, particle stability, and ingredient solubility, making it highly attractive for innovative beverage formulations targeting health-conscious consumers.Adoption across meat and seafood processing is increasing as manufacturers seek improved tenderization, microbial control, and marination efficiency. Functional foods and ready-to-eat meal segments are also expanding rapidly, supported by urbanization, convenience-oriented consumption patterns, and demand for longer shelf life without compromising product quality. Export-driven production in Asia-Pacific and Europe is further shaping equipment deployment strategies focused on quality standardization, regulatory compliance, and energy-efficient processing technologies.

Explore more data points, trends and opportunities Download Free Sample Report

Food Ultrasound Market Segmentations

By Technology Type

- High-Intensity Ultrasound

- Low-Intensity Ultrasound

- Hybrid Ultrasound Systems

By Equipment Type

- Ultrasonic Processors / Reactors

- Ultrasonic Homogenizers

- Ultrasonic Emulsifiers

- Ultrasonic Cutters & Slicers

- Ultrasonic Cleaning Systems

- Ultrasonic Drying Systems

- Ultrasonic Extraction Systems

- Inline Ultrasound Processing Units

By Application

- Emulsification & Homogenization

- Extraction

- Microbial Inactivation & Preservation

- Crystallization Control

- Degassing & Defoaming

- Tenderization & Texture Modification

- Drying Enhancement

- Quality Inspection & Process Monitoring

By End-Use Industry

- Dairy Processing

- Beverage Processing

- Meat & Seafood Processing

- Fruits & Vegetables Processing

- Bakery & Confectionery

- Edible Oils & Fats

- Functional Foods & Nutraceuticals

- Ready-to-Eat & Processed Foods

By Mode of Operation

- Batch Processing Systems

- Continuous Processing Systems

- Inline Integrated Systems

By Frequency Range

- Low Frequency

- Medium Frequency

- High Frequency

Regional Insights

North America

North America accounts for approximately 28% of global market demand, led by the United States and Canada. Regional growth is driven by advanced food processing infrastructure, high automation adoption, and strong regulatory frameworks supporting clean-label and minimally processed foods. Increasing investment in food technology innovation, coupled with strong collaboration between equipment manufacturers and research institutions, is accelerating commercialization of ultrasound-assisted processing. Additionally, rising demand for plant-based foods, functional beverages, and premium packaged products continues to expand application opportunities across industrial processors.

Europe

Europe holds nearly 30% of the global market, with Germany, France, Italy, and the Netherlands serving as key adoption hubs. Growth in the region is supported by stringent food safety regulations, sustainability mandates, and strong consumer preference for minimally processed and environmentally responsible food products. The European Union’s emphasis on reducing energy consumption and processing waste encourages manufacturers to adopt non-thermal technologies such as ultrasound. Furthermore, the region’s strong dairy and specialty food export sectors are driving investments in advanced processing technologies to maintain global quality standards.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at an estimated CAGR of around 14%, with China, India, Japan, and South Korea driving demand growth. Rapid modernization of food processing infrastructure, expanding middle-class consumption, and rising exports of processed foods are major regional growth drivers. Governments across the region are supporting food safety improvements and industrial automation, encouraging adoption of advanced processing equipment. Increasing investments in plant-based foods, dairy alternatives, and functional nutrition products further accelerate ultrasound technology deployment across large-scale manufacturing facilities.

Latin America

Latin America is experiencing steady growth led by Brazil and Mexico, where modernization of food manufacturing and export-oriented production is expanding equipment demand. Regional growth is driven by increasing investments in premium processed food production aimed at international markets requiring consistent quality and extended shelf life. Improvements in cold-chain logistics and food processing infrastructure are also supporting adoption of advanced processing technologies such as ultrasound, particularly in beverage, meat, and fruit processing industries.

Middle East & Africa

The Middle East & Africa region is emerging as a developing market supported by rising food security initiatives and industrial diversification strategies. The United Arab Emirates and Saudi Arabia are key markets where high-income populations and growing demand for premium packaged foods encourage adoption of advanced processing technologies. Across Africa, expanding dairy processing hubs and functional food production facilities are creating new opportunities for ultrasound equipment deployment. Government-led food industry modernization programs and increasing intra-regional trade are expected to generate incremental growth throughout the forecast period.

Key Players in the Food Ultrasound Market

- Hielscher Ultrasonics GmbH

- Sonics & Materials Inc.

- Dukane Corporation

- Herrmann Ultraschalltechnik GmbH & Co. KG

- Emerson Electric Co.

- Branson Ultrasonics

- Telsonic AG

- Crest Ultrasonics Corp.

- Weber Ultrasonics AG

- Sonic Italia Srl

- Cheersonic Ultrasonic Equipment

- UIP GmbH

- Bandelin electronic GmbH

- Syncore Technologies AB

- Misonix Inc.