Food Processing Ingredients Market Size

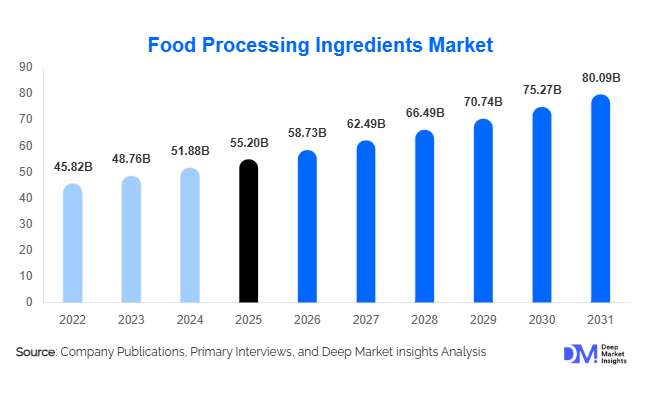

According to Deep Market Insights,the global food processing ingredients market size was valued at USD 55.2 billion in 2025 and is projected to grow from USD 58.73 billion in 2026 to reach USD 80.09 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). Market growth is primarily driven by rising global consumption of processed and convenience foods, increasing demand for clean-label and functional ingredients, and expanding food manufacturing capacity across emerging economies. As food processors focus on shelf-life extension, sensory enhancement, and nutritional fortification, demand for preservatives, emulsifiers, enzymes, sweeteners, and functional proteins continues to accelerate worldwide.

Key Market Insights

- Preservatives lead the ingredient category, accounting for approximately 21% of the global market share in 2025, driven by shelf-life optimization and food waste reduction initiatives.

- Plant-based ingredients dominate by source, contributing nearly 54% of total market demand due to clean-label and sustainability preferences.

- Asia-Pacific holds the largest regional share, representing about 34% of global demand in 2025, led by China and India.

- Industrial food manufacturers account for nearly 68% of total demand, reflecting bulk procurement and continuous production requirements.

- Powdered ingredients dominate by form, with over 62% share, due to easier storage, transport, and blending efficiency.

- Functional and fortified food applications are the fastest-growing segment, expanding at over 8% CAGR globally.

What are the latest trends in the food processing ingredients market?

Clean-Label and Natural Reformulation

Food manufacturers are increasingly reformulating products to eliminate synthetic additives and replace them with natural preservatives, plant-based emulsifiers, and fermentation-derived stabilizers. Consumer demand for recognizable ingredients is influencing R&D spending, leading to growth in botanical extracts, natural colorants, and enzyme-based processing solutions. Regulatory pressures in North America and Europe are further accelerating the shift toward transparent labeling and minimally processed formulations. Ingredient suppliers are investing heavily in fermentation and biotechnology platforms to deliver natural alternatives with equivalent functional performance.

Enzyme Innovation and Biotechnology Integration

Advancements in enzyme engineering and microbial fermentation are enhancing efficiency in bakery, dairy, and meat processing. Enzymes are increasingly used to improve dough texture, increase cheese yield, and enhance protein digestibility. Microencapsulation technologies are also being deployed to protect sensitive ingredients such as probiotics and omega-3 fatty acids during processing. These innovations are improving cost efficiency and sustainability by reducing waste and optimizing production cycles across food manufacturing facilities.

What are the key drivers in the food processing ingredients market?

Rising Demand for Processed and Convenience Foods

Urbanization, dual-income households, and rapid retail expansion are driving global demand for packaged foods, ready-to-eat meals, frozen products, and beverages. These products require stabilizers, preservatives, flavor enhancers, and sweeteners to maintain quality and consistency. Emerging markets in Asia-Pacific and Latin America are contributing significantly to incremental volume growth as per capita processed food consumption rises steadily.

Growth in Health-Oriented and Functional Foods

The surge in demand for high-protein, low-sugar, gluten-free, and fortified foods is accelerating ingredient innovation. Functional proteins, dietary fibers, omega-3 fatty acids, and sugar reduction solutions are witnessing robust growth. Aging populations in Europe and Japan, along with wellness-focused millennials globally, are driving demand for nutritionally enhanced processed food products.

What are the restraints for the global market?

Volatility in Agricultural Raw Material Prices

Food processing ingredients rely heavily on agricultural inputs such as corn, soy, sugarcane, and dairy derivatives. Fluctuating commodity prices, climate change impacts, and supply chain disruptions create cost pressures for manufacturers. These variations directly affect pricing structures and profit margins across bulk ingredient categories.

Stringent Regulatory Compliance

Global regulatory frameworks such as FDA, EFSA, FSSAI, and Codex Alimentarius impose strict guidelines on additive usage, labeling standards, and safety approvals. Regulatory disparities across regions increase compliance costs and extend product approval timelines, especially for new synthetic or novel functional ingredients.

What are the key opportunities in the food processing ingredients industry?

Expansion in Emerging Economies

Rapid food processing industrialization in India, Indonesia, Vietnam, Brazil, and African economies presents substantial growth potential. Government-backed initiatives such as India’s Production Linked Incentive (PLI) scheme and China’s “Made in China 2025” are strengthening domestic ingredient manufacturing capabilities, encouraging foreign direct investments and localized production.

Functional & Fortified Food Integration

Opportunities are expanding in fortified bakery, dairy, and beverage applications. Protein enrichment, fiber fortification, and probiotic inclusion are becoming mainstream. Ingredient companies focusing on plant-based proteins and specialty enzymes are positioned to capture premium margins in health-focused product categories.

Ingredient Type Insights

Preservatives dominate the global food processing ingredients market, accounting for approximately 21% of total revenue share in 2025. Their leadership is primarily driven by the rapid expansion of packaged and convenience foods, increasing global trade of perishable food products, and stringent food safety regulations requiring extended shelf stability. The rising demand for longer distribution cycles in emerging economies and growing e-commerce penetration in food retail further strengthen the segment’s dominance. Emulsifiers and stabilizers follow closely, supported by their critical role in enhancing texture, mouthfeel, and product consistency across bakery, dairy, sauces, and beverage formulations. The leading driver for this segment is the increasing consumer expectation for premium-quality, visually appealing, and structurally stable food products.

Sweeteners, particularly high-intensity alternatives such as stevia, sucralose, and monk fruit extracts, are gaining strong traction amid global sugar reduction initiatives, obesity concerns, and regulatory pressure on sugar content in beverages and processed foods. Reformulation strategies adopted by multinational food companies are accelerating demand for alternative sweetening systems. Enzymes represent one of the fastest-growing ingredient categories, supported by technological advancements in fermentation, bio-processing, and clean-label manufacturing. The leading driver for enzymes is their ability to improve production efficiency, enhance yield, reduce waste, and enable natural processing methods, making them highly attractive for sustainable and cost-optimized food manufacturing.

Application Insights

Bakery and confectionery applications account for nearly 24% of the total market in 2025, making it the leading application segment. The primary growth driver is the consistently high global consumption of bread, biscuits, cakes, pastries, and sweet snacks across both developed and emerging economies. Urbanization, changing dietary patterns, and demand for convenience foods continue to fuel ingredient utilization in this segment, particularly preservatives, emulsifiers, enzymes, and flavor enhancers. Product innovation in artisanal-style packaged bakery goods and extended shelf-life products further strengthens demand.

Dairy and frozen desserts remain strong contributors, particularly for stabilizers, emulsifiers, cultures, and enzymes used to enhance texture, shelf life, and nutritional value. The segment benefits from rising consumption of yogurt, flavored milk, plant-based dairy alternatives, and premium ice creams. Beverages represent one of the fastest-growing application areas, fueled by demand for functional drinks, energy beverages, protein-enriched drinks, and sugar-reduced formulations. Clean-label reformulations and fortification with vitamins, minerals, and probiotics are key drivers in this segment. Processed meat and ready meals also generate substantial demand for preservatives, flavor enhancers, binders, and phosphates, supported by busy lifestyles, rising disposable incomes, and growing organized retail distribution.

End-Use Industry Insights

Industrial food manufacturers account for approximately 68% of total demand in 2025, representing the dominant end-use segment. Large-scale production capabilities, global distribution networks, and continuous product innovation drive substantial ingredient consumption across multiple food categories. The leading driver for this segment is the increasing reliance on standardized, high-volume food processing to meet growing urban and export demand.

Foodservice and quick-service restaurant (QSR) chains are expanding at over 7% CAGR, driven by rapid global expansion of franchise networks, rising dining-out culture, and digital food delivery platforms. These operators require consistent ingredient quality, stable formulations, and extended shelf life, thereby supporting steady ingredient demand. Nutraceutical and functional food producers are emerging as high-growth consumers, particularly for specialty proteins, probiotics, dietary fibers, plant extracts, and bioactive compounds. Rising consumer awareness regarding preventive healthcare and immunity enhancement is the primary driver for ingredient innovation in this segment.

| By Ingredient Type | By Source | By Form | By Application | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with around 34% share in 2025, supported by rapid urbanization, expanding middle-class populations, and increasing packaged food consumption. China alone contributes nearly 16% of global demand, driven by large-scale food processing operations, strong export activity, and government support for industrial modernization. The country’s growing ready-to-eat and convenience food sector significantly boosts demand for preservatives, stabilizers, and enzymes. India is the fastest-growing major market, expanding at over 8% CAGR, supported by infrastructure modernization, rising disposable income, increasing penetration of organized retail, and expansion of domestic food processing capacity. Japan and South Korea maintain steady demand in high-value enzyme and specialty ingredient categories, driven by innovation in functional foods, premium bakery products, and aging population-driven health food demand.

North America

North America accounts for approximately 28% of global demand, with the United States representing nearly 22% of the total market. The region benefits from advanced food processing infrastructure, high per capita processed food consumption, and strong demand for functional, fortified, and clean-label products. Reformulation initiatives aimed at reducing artificial additives and sugar content are accelerating innovation in enzymes and natural sweeteners. The expansion of plant-based food alternatives and protein-enriched products further supports ingredient demand. Canada contributes steadily, particularly in dairy, bakery, and meat processing ingredients, supported by export-oriented food production and strong regulatory compliance standards.

Europe

Europe holds about 24% of the market, led by Germany, France, the U.K., and Italy. Stringent regulatory standards, clean-label reforms, and sustainability initiatives are key drivers shaping ingredient innovation across the region. Germany remains a major exporter of processed foods, supporting stable demand for enzymes, stabilizers, and preservation systems. Western European markets emphasize organic and natural ingredients, while Eastern Europe is witnessing growing investment in food processing infrastructure. Increasing consumer preference for reduced-sugar, allergen-free, and plant-based products further drives specialty ingredient demand.

Latin America

Latin America represents nearly 8% of global demand, with Brazil and Mexico leading growth in bakery, beverage, and processed food segments. Expansion of organized retail chains, increasing urban consumption patterns, and rising processed food exports are key growth drivers. The region is also benefiting from improving cold chain logistics and foreign direct investment in food manufacturing facilities. Growing middle-class populations and increasing consumption of packaged snacks and dairy products continue to support ingredient demand.

Middle East & Africa

The Middle East & Africa accounts for approximately 6% of global demand and is the fastest-growing region at around 8.5% CAGR. UAE and Saudi Arabia are key import-driven markets, supported by strong reliance on packaged food imports, expanding foodservice sectors, and government investments in food security initiatives. Rising tourism and hospitality expansion further contribute to ingredient demand. South Africa supports regional food processing activity with relatively advanced manufacturing capabilities. Increasing urbanization, rising disposable incomes, and expanding supermarket penetration across select African economies are expected to sustain long-term market growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Food Processing Ingredients Market

- Cargill Incorporated

- Archer Daniels Midland Company (ADM)

- Ingredion Incorporated

- Kerry Group plc

- DSM-Firmenich

- Tate & Lyle PLC

- International Flavors & Fragrances Inc. (IFF)

- Givaudan SA

- Novozymes A/S

- BASF SE

- DuPont Nutrition & Biosciences

- Associated British Foods plc

- Ajinomoto Co., Inc.

- Corbion N.V.

- Chr. Hansen Holding A/S