Food Pathogen Testing Market Size

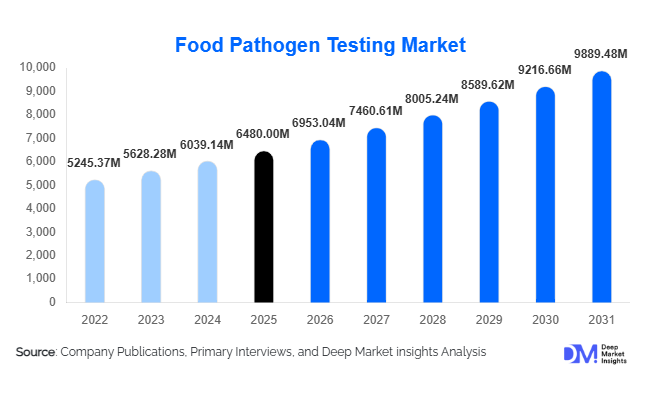

According to Deep Market Insights, the global food pathogen testing market size was valued at USD 6,480 million in 2025 and is projected to grow from USD 6,953.04 million in 2026 to reach USD 9,889.48 million by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). The food pathogen testing market growth is primarily driven by stringent food safety regulations, rising incidences of foodborne illnesses, increasing global trade of perishable food products, and technological advancements in rapid diagnostic methods.

Food pathogen testing plays a critical role in ensuring microbiological safety across the global food supply chain, covering raw materials, processed foods, dairy, meat, seafood, beverages, and ready-to-eat products. The market is evolving from conventional culture-based techniques toward rapid and highly sensitive molecular diagnostics such as PCR and immunoassay-based detection systems. Governments worldwide are tightening compliance standards, mandating hazard analysis and preventive control programs, which directly increase testing volumes across food processing facilities.

In addition, consumer awareness regarding food safety and traceability has intensified after several high-profile recalls, pushing manufacturers to invest in in-house laboratories and third-party accredited testing services. Export-driven economies are also strengthening pathogen surveillance to meet international regulatory benchmarks. As global supply chains become more complex and processed food consumption continues to rise, the demand for accurate, fast, and cost-effective pathogen testing solutions is expected to sustain steady growth over the next five years.

Key Market Insights

- Molecular diagnostic technologies are gaining rapid adoption, reducing testing turnaround time and improving detection accuracy.

- The meat, poultry, and seafood segments account for the largest testing volumes due to higher contamination risks.

- North America dominates the market owing to strict regulatory enforcement and advanced laboratory infrastructure.

- Asia-Pacific is the fastest-growing region, supported by expanding food exports and regulatory modernization.

- Third-party laboratory services are expanding as small and mid-sized processors outsource compliance testing.

- Automation and AI-based laboratory management systems are improving efficiency and cost optimization.

What are the latest trends in the food pathogen testing market?

Shift Toward Rapid and Molecular Testing Platforms

Traditional culture-based methods, while reliable, require 2–5 days for confirmation. The market is witnessing accelerated adoption of PCR-based, ELISA-based, and next-generation sequencing technologies that reduce detection time to under 24 hours. Food manufacturers increasingly prefer rapid kits and automated systems to minimize product hold times and reduce recall risks. Multiplex PCR systems capable of detecting multiple pathogens in a single test are gaining commercial traction, particularly in large-scale processing facilities.

Integration of Digital Traceability and Smart Lab Systems

Digital laboratory information management systems (LIMS), blockchain-enabled traceability, and AI-driven data analytics are transforming pathogen testing workflows. These technologies improve compliance documentation, enhance recall response times, and allow predictive contamination monitoring. Cloud-connected diagnostic instruments are enabling centralized oversight across multi-location food production networks, further modernizing the industry.

What are the key drivers in the food pathogen testing market?

Stringent Food Safety Regulations

Governments across North America, Europe, and Asia have strengthened food safety frameworks, mandating hazard analysis and risk-based preventive controls. Regulatory agencies require routine pathogen screening for Salmonella, Listeria, E. coli, and Campylobacter, increasing mandatory testing volumes across food categories. Export-focused producers must comply with importing country standards, further driving demand.

Rising Incidence of Foodborne Illnesses

Globally reported outbreaks have heightened industry accountability. Large-scale recalls cause financial losses and brand damage, pushing companies to adopt proactive pathogen testing strategies. Increased surveillance in ready-to-eat and minimally processed foods has significantly boosted laboratory testing demand.

What are the restraints for the global market?

High Capital and Operational Costs

Advanced PCR instruments, automated analyzers, and skilled laboratory personnel require substantial investments. Small-scale processors in emerging economies often face budget constraints, limiting adoption of high-end technologies.

Complex Regulatory Harmonization

Variations in pathogen threshold limits and testing protocols across countries create compliance complexities for multinational food exporters. Standardization gaps increase operational burdens and testing redundancies.

What are the key opportunities in the food pathogen testing industry?

Expansion in Emerging Export Economies

Asia-Pacific and Latin America are strengthening food export capabilities. Governments are investing in accredited laboratories and testing infrastructure to meet international standards. This creates strong growth prospects for diagnostic kit suppliers and third-party testing service providers.

Automation and AI Integration

Smart laboratories with robotics-based sample preparation and AI-driven contamination forecasting present significant efficiency gains. Companies offering integrated digital solutions can capture premium market segments focused on productivity and traceability.

Ready-to-Eat and Plant-Based Food Testing

Rising demand for ready-to-eat meals and plant-based protein alternatives introduces new microbial risk profiles. Specialized pathogen panels tailored to these categories represent a growing niche opportunity for testing providers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6480 Million |

| Market Size in 2026 | USD 6953.04 Million |

| Market Size in 2031 | USD 9889.48 Million |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Insights

Molecular diagnostics (PCR-based testing) dominate the global food pathogen testing market, accounting for approximately 42% of total revenue in 2025. The leadership of this segment is primarily driven by the growing need for rapid turnaround times, high analytical sensitivity, and compliance with increasingly stringent food safety regulations. Real-time PCR platforms can detect pathogens such as Salmonella, Listeria monocytogenes, and E. coli within hours rather than days, significantly reducing product quarantine time and minimizing recall risks. Large-scale food processors prefer PCR-based systems because they enhance operational efficiency and reduce inventory holding costs. Furthermore, multiplex PCR technologies that enable simultaneous detection of multiple pathogens in a single run are accelerating adoption across high-throughput facilities.

Immunoassay-based testing holds approximately 28% of the 2025 market share and remains widely adopted due to cost-effectiveness and ease of use, especially in mid-sized laboratories and developing markets. Meanwhile, traditional culture-based methods account for nearly 20% of global revenue, primarily because they remain the regulatory gold standard for confirmatory testing. However, their slower turnaround time is gradually limiting their share in high-volume commercial environments. Rapid test kits, including lateral flow assays and portable detection systems, are witnessing growing demand in decentralized testing environments and field-level inspections, particularly in emerging export economies.

Pathogen Type Insights

Salmonella testing leads the pathogen segment with nearly 30% share of the global market in 2025. Its dominance is driven by strict zero-tolerance policies in poultry, meat, and processed food exports, particularly in North America and Europe. Salmonella remains one of the most commonly reported causes of foodborne outbreaks worldwide, compelling mandatory routine testing across slaughterhouses, poultry processors, and packaged food facilities.

Listeria testing accounts for approximately 22% of the total market and is particularly critical in ready-to-eat (RTE) foods, dairy, and frozen products. The high fatality rate associated with Listeria monocytogenes infections has prompted regulatory bodies to enforce stringent environmental monitoring programs in food processing plants, strengthening segment growth. E. coli testing contributes nearly 18% of global revenue, especially in beef, fresh produce, and raw milk segments. Increasing cross-border trade in leafy greens and meat products has intensified routine screening requirements. Other pathogens, including Campylobacter and Vibrio species, are gaining relevance in seafood-exporting regions, further diversifying pathogen testing demand.

Food Type Insights

Meat, poultry, and seafood collectively represent the largest food category, contributing approximately 34% of global revenue in 2025. This segment leads due to higher intrinsic contamination risks, complex cold-chain logistics, and stringent export certification requirements. Countries with significant meat exports mandate comprehensive pathogen screening before shipment, substantially increasing testing volumes.

Dairy products account for nearly 18% of the market, driven by Listeria and Salmonella surveillance in milk, cheese, and infant formula production. Processed and packaged foods contribute around 16%, supported by growth in ready-to-eat meals and frozen food consumption. Fresh produce testing is one of the fastest-growing sub-segments due to recurring contamination incidents in leafy greens and fruits involved in international trade.

Testing Site Insights

In-house testing laboratories dominate with approximately 55% of the global market share in 2025. Large food processing companies are increasingly investing in internal laboratory infrastructure to maintain real-time quality control, reduce turnaround time, and avoid third-party dependency. Automation, robotics-assisted sample preparation, and integrated LIMS platforms are strengthening the in-house testing ecosystem. Third-party testing laboratories account for 45% of market revenue and are expanding rapidly among small and medium enterprises that lack capital investment capabilities. These labs benefit from accreditation, cross-border certification expertise, and economies of scale, particularly in export-driven regions.

End-Use Insights

Food processing companies represent nearly 60% of total market demand in 2025, making them the dominant end-use segment. Growth in global packaged food production, expansion of multinational food brands, and rising export volumes are driving continuous pathogen screening across production batches. The ready-to-eat meals segment is among the fastest-growing end uses, expanding at over 8% annually due to urbanization, changing dietary habits, and convenience-driven consumption. Plant-based protein manufacturing is emerging as a new testing-intensive category, as novel ingredients require microbiological validation. Additionally, global processed food exports exceeding USD 1 trillion annually reinforce long-term demand for compliance testing, especially among export-oriented manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Food Pathogen Testing Market Segmentations

By Product Type

- Molecular Diagnostics

- Immunoassay-Based Testing

- Culture-Based Methods

- Rapid Test Kits

By Pathogen Type

- Salmonella

- Listeria

- E. coli

- Campylobacter

- Others (Vibrio, Shigella)

By Food Type

- Meat, Poultry, Seafood

- Dairy Products

- Processed Foods

- Fresh Produce

By Testing Site

- In-House Laboratories

- Third-Party Laboratories

By End-Use Industry

- Food Processing Companies

- Export-Oriented Food Manufacturers

- Ready-to-Eat Food Producers

- Plant-Based Protein & Novel Food Manufacturers

Regional Insights

North America

North America accounts for approximately 35% of the global market share in 2025, with the United States contributing nearly 28% alone. Regional dominance is driven by stringent enforcement of preventive food safety regulations, high recall accountability standards, and advanced laboratory infrastructure. The presence of large multinational food processors, strong retail supply chains, and high consumer awareness regarding food safety significantly increase routine pathogen testing volumes. Canada also maintains strict import-export inspection requirements, further supporting regional demand.

Europe

Europe represents approximately 27% of the global market in 2025. Germany, France, the United Kingdom, Italy, and Spain are major contributors. Growth is supported by strict microbiological criteria for foodstuffs, mandatory environmental monitoring in food facilities, and strong traceability regulations. The European Union’s harmonized food safety standards require extensive testing across dairy, meat, and RTE segments. Export-focused countries such as Germany and the Netherlands further drive testing volumes to maintain compliance in global trade.

Asia-Pacific

Asia-Pacific accounts for approximately 24% of global revenue and is the fastest-growing region, expanding at nearly 9% CAGR. China leads regional demand due to rapid food industrialization, government-led food safety modernization initiatives, and increasing export scrutiny. India is witnessing accelerated growth driven by regulatory reforms and the expansion of packaged food manufacturing. Japan and Australia maintain mature testing markets supported by strong seafood and dairy exports. Rising middle-class consumption, urbanization, and increasing cross-border trade are key regional growth drivers.

Latin America

Latin America contributes around 8% of global revenue, led by Brazil and Mexico. Brazil’s position as one of the world’s largest poultry and beef exporters necessitates extensive pathogen monitoring to meet U.S. and European import standards. Mexico’s growing processed food exports and regulatory alignment with North American markets further strengthen testing demand.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of the global market. Growth is driven by rising food imports, increasing packaged food consumption, and the modernization of national food safety authorities. Gulf Cooperation Council (GCC) countries are investing heavily in laboratory infrastructure to reduce import dependency risks. In Africa, export-oriented agricultural economies are gradually strengthening pathogen surveillance systems to improve international market access.

Key Players in the Food Pathogen Testing Market

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- bioMérieux

- Neogen Corporation

- Merck KGaA

- QIAGEN

- Agilent Technologies

- PerkinElmer

- SGS SA

- Eurofins Scientific

- Bureau Veritas

- Intertek Group

- Romer Labs

- Shimadzu Corporation

- Bruker Corporation