Food Grade Industrial Gases Market Size

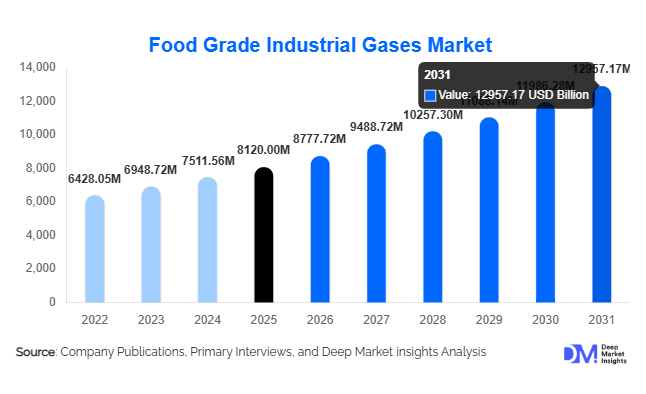

According to Deep Market Insights,the global food grade industrial gases market size was valued at USD 8120 million in 2025 and is projected to grow from USD 8777.72 million in 2026 to reach USD 12957.17 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). Market growth is primarily driven by the rapid expansion of processed and packaged food industries, increasing adoption of modified atmosphere packaging (MAP), and rising global demand for frozen and export-oriented food products. Growing food safety regulations across developed economies and expanding cold chain infrastructure in emerging markets are further accelerating demand for food-grade nitrogen, carbon dioxide, oxygen, and specialty gas blends.

Key Market Insights

- Carbon dioxide dominates the market, accounting for nearly 42% of total revenue share in 2025, driven by carbonation and packaging applications.

- Modified Atmosphere Packaging (MAP) remains the leading application, contributing approximately 35% of global demand.

- Asia-Pacific holds the largest regional share (31%), supported by rapid food processing expansion in China and India.

- Bulk supply mode accounts for nearly 48% of total distribution, preferred by large beverage and meat processors.

- Top five players control nearly 65% of the global market, reflecting moderate-to-high industry concentration.

- Rising frozen food exports and cold chain investments are significantly boosting cryogenic gas consumption worldwide.

What are the latest trends in the food grade industrial gases market?

Expansion of Modified Atmosphere Packaging (MAP)

MAP adoption is expanding rapidly across meat, dairy, bakery, and fresh produce categories. Retailers are prioritizing extended shelf life, reduced food waste, and enhanced product appearance. Nitrogen and CO₂ blends are increasingly customized for specific food matrices, enabling optimized oxygen displacement and microbial growth control. Supermarket penetration in Asia and Latin America is further strengthening MAP adoption, especially for ready-to-eat and convenience foods.

On-Site Gas Generation Systems

Food manufacturers are investing in on-site nitrogen generation systems to reduce dependency on bulk deliveries and improve cost efficiency. Pressure swing adsorption (PSA) technology and membrane-based nitrogen generators are gaining traction in mid-sized food plants. This shift is particularly prominent in emerging economies where logistics costs remain high. Digital monitoring systems integrated with generation units are improving supply predictability and operational control.

What are the key drivers in the food grade industrial gases market?

Growth in Processed & Convenience Foods

The global processed food sector is expanding at over 6% annually, directly increasing demand for freezing, chilling, and packaging gases. Urbanization, dual-income households, and changing dietary patterns are accelerating consumption of packaged and ready-to-eat products.

Rising Food Safety Regulations

Stringent regulations across the U.S., Europe, Japan, and India require controlled atmosphere storage and hygienic processing environments. Compliance with ISO 22000, FDA, and EFSA standards is driving adoption of certified food-grade gases, especially in export-focused industries.

What are the restraints for the global market?

Energy-Intensive Production Processes

Air separation units used for nitrogen and oxygen production require substantial electricity, making manufacturers vulnerable to energy price volatility. Rising power costs can compress operating margins.

Infrastructure & Logistics Constraints

Transportation of cryogenic gases requires specialized tankers and storage facilities. Developing regions often face infrastructure gaps, limiting rapid penetration into smaller food processing clusters.

What are the key opportunities in the food grade industrial gases industry?

Export-Driven Meat & Seafood Processing

Global meat and seafood exports continue to expand, particularly from Brazil, India, Vietnam, and Thailand. Cryogenic freezing using liquid nitrogen and CO₂ ensures product integrity during long-haul transport. Gas suppliers partnering with export clusters can secure long-term supply agreements.

Cold Chain Infrastructure Development

Governments are investing heavily in cold storage, refrigerated transport, and food parks. Public-private partnerships in India, Southeast Asia, and the Middle East are enhancing frozen food capabilities, increasing structural demand for industrial gases.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8120 Million |

| Market Size in 2026 | USD 8777.72 Million |

| Market Size in 2031 | USD 12957.17 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Gas Type Insights

Carbon dioxide leads the market, holding approximately 42% share in 2025, primarily driven by its extensive application in beverage carbonation and Modified Atmosphere Packaging (MAP). The leading position of CO₂ is supported by rising global consumption of carbonated beverages, increasing demand for ready-to-eat meals, and the need for extended shelf life across processed food categories. Its cost-effectiveness, availability, and compatibility with multiple packaging formats further reinforce its dominance. Nitrogen follows closely, benefiting from its inert properties that prevent oxidation and maintain product freshness in snack foods, dairy, coffee packaging, and edible oils. Oxygen plays a crucial role in modified atmosphere storage for fresh produce, red meat blooming, and seafood preservation, where controlled oxygen levels help retain color and quality. Specialty gas blends are emerging as high-margin offerings, particularly in premium meat, bakery, and convenience food applications, where customized gas mixtures enhance shelf life and product integrity while reducing food waste.

Application Insights

Modified Atmosphere Packaging accounts for nearly 35% of the total market, making it the leading application segment due to increasing global demand for longer shelf life, improved food safety, and reduced spoilage during transportation and storage. The segment’s leadership is primarily driven by rapid expansion of packaged and convenience foods, growth in modern retail chains, and the globalization of food trade. Freezing and chilling applications are growing steadily at over 8% CAGR, supported by expanding seafood and poultry exports, rising demand for frozen ready meals, and increased cold chain infrastructure investments across emerging economies. Carbonation remains a stable and high-volume segment, underpinned by consistent global beverage consumption, including soft drinks, sparkling water, and alcoholic beverages. Additional applications such as inerting and blanketing continue to gain importance as manufacturers prioritize oxidation control and product consistency in edible oils, wine, and processed foods.

Mode of Supply Insights

Bulk liquid supply dominates with 48% market share, primarily driven by large-scale food and beverage processors requiring uninterrupted, high-volume, and cost-efficient gas delivery systems. Bulk supply ensures operational efficiency, lower per-unit cost, and reduced downtime, making it the preferred choice for industrial-scale meat processors, dairy manufacturers, and beverage bottlers. Cylinder-based distribution continues to serve small and medium-sized food processing units, commercial kitchens, and regional beverage producers where demand volumes are moderate and flexibility is essential. On-site gas generation is gaining traction in cost-sensitive and infrastructure-constrained markets, as it reduces logistics dependency, enhances supply reliability, and offers long-term cost savings. Technological advancements in compact gas generation systems are further accelerating adoption, particularly among mid-sized processors seeking operational autonomy.

End-Use Industry Insights

The meat, poultry & seafood segment leads with 29% market share, driven by extensive use of freezing, chilling, and MAP technologies to maintain freshness, color stability, and microbiological safety. Growth in global protein consumption, rising exports of processed meat products, and stringent food safety regulations continue to reinforce the segment’s dominance. The beverage sector remains a high-volume consumer of CO₂, supported by sustained demand for carbonated drinks, craft beverages, and alcoholic products. Dairy and frozen desserts demonstrate consistent growth aligned with rising global exports, urbanization, and increased consumption of value-added dairy products. Bakery and confectionery applications are also expanding steadily, as nitrogen-based packaging solutions help extend shelf life and maintain texture quality in packaged snacks and baked goods.

Explore more data points, trends and opportunities Download Free Sample Report

Food Grade Industrial Gases Market Segmentations

By Gas Type

- Carbon Dioxide (CO₂)

- Nitrogen (N₂)

- Oxygen (O₂)

- Argon (Ar)

- Hydrogen (H₂)

- Specialty Gas Blends (MAP Mixtures)

By Application

- Modified Atmosphere Packaging (MAP)

- Carbonation

- Freezing & Chilling

- Blanketing & Inerting

- Dry Ice Production

- Food Processing & Preservation

- Controlled Atmosphere Storage

By Mode of Supply

- Bulk (Liquid Supply)

- Cylinder Packaged Gas

- On-Site Generation

- Microbulk

By End-Use Industry

- Meat, Poultry & Seafood Processing

- Dairy & Frozen Desserts

- Beverages

- Bakery & Confectionery

- Fruits & Vegetables Processing

- Ready-to-Eat & Convenience Foods

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 31% of global market share in 2025 and remains the fastest-growing region at 9.2% CAGR. China leads regional demand, contributing nearly 40% of APAC consumption, followed by India and Japan. Regional growth is primarily driven by rapid expansion of food processing industries, increasing urbanization, rising disposable incomes, and strong growth in packaged and convenience food consumption. Expanding cold chain infrastructure, government support for food exports, and growing seafood and poultry processing capacity further accelerate demand. India’s rising organized retail penetration and Japan’s advanced food preservation technologies also contribute significantly to market expansion.

North America

North America holds about 28% market share, with the U.S. accounting for over 80% of regional demand. Growth in this region is supported by advanced food safety regulations, widespread adoption of MAP technologies, and a mature beverage industry with high per capita carbonated drink consumption. Strong cold storage infrastructure, technological innovation in packaging solutions, and increasing demand for clean-label and minimally processed foods continue to sustain market development. Canada also contributes steadily through seafood exports and expanding dairy processing operations.

Europe

Europe represents 24% of the global market, led by Germany, France, the U.K., and Italy. Regional growth is driven by strict regulatory compliance standards for food safety, strong dairy and meat export industries, and high penetration of advanced packaging technologies. Sustainability initiatives and efforts to reduce food waste are accelerating adoption of MAP and controlled atmosphere storage solutions. The region’s well-established retail networks and consumer preference for high-quality packaged foods further strengthen demand for food-grade gases.

Latin America

Brazil and Mexico dominate regional demand, supported by expanding meat exports, particularly beef and poultry, along with steady growth in beverage manufacturing. Increasing foreign investment in food processing infrastructure and improvements in cold chain logistics are strengthening market penetration. Rising urbanization and growing consumption of packaged foods across Chile, Argentina, and Colombia are also contributing to regional expansion.

Middle East & Africa

Saudi Arabia, the UAE, and South Africa are key contributors to regional growth, supported by high food import dependency and expanding investments in cold storage and food processing facilities. The region’s harsh climatic conditions necessitate advanced preservation and packaging technologies, thereby increasing reliance on food-grade gases. Government initiatives aimed at enhancing food security, along with rapid retail sector development and tourism-driven food demand, further stimulate market growth across the Middle East & Africa.

Key Players in the Food Grade Industrial Gases Market

- Linde plc

- Air Liquide

- Air Products and Chemicals, Inc.

- Messer Group

- Nippon Sanso Holdings Corporation

- Taiyo Nippon Sanso

- SOL Group

- Matheson Tri-Gas

- Gulf Cryo

- Yingde Gases

- Ellenbarrie Industrial Gases

- SIAD Group

- Coregas

- Universal Industrial Gases

- Air Water Inc.