Food Grade Ethanol Market Size

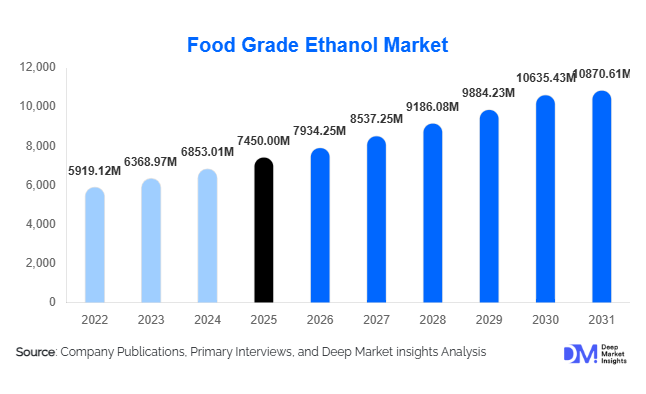

According to Deep Market Insights,the global Food Grade ethanol market size was valued at USD 7450 million in 2025 and is projected to grow from USD 7934.25 million in 2026 to reach USD 10870.61 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The Food Grade ethanol market growth is primarily driven by increasing alcoholic beverage production, rising demand for natural flavor extraction, expansion of clean-label food formulations, and growing use of food-safe sanitization solutions across hospitality and processing industries.

Key Market Insights

- Alcoholic beverages account for over 60% of total demand, making beverage manufacturing the dominant revenue-generating segment globally.

- Asia-Pacific leads global consumption, supported by expanding distillery capacity in China and India and strong population-driven beverage demand.

- Corn-based ethanol dominates feedstock supply, particularly in North America, due to stable agricultural output and high fermentation efficiency.

- Clean-label and natural extraction trends are increasing ethanol usage in botanical extracts, flavors, and nutraceutical applications.

- Export-oriented spirits production in Mexico, France, Scotland, and Japan is strengthening global trade flows.

- Government biofuel programs in India, Brazil, and Southeast Asia are indirectly boosting Food Grade ethanol infrastructure investments.

What are the latest trends in the food grade ethanol market?

Shift Toward Clean-Label & Natural Extraction

Food manufacturers are increasingly adopting ethanol as a preferred solvent for botanical extraction, natural flavor concentration, and herbal tincture production. With rising consumer demand for transparency and synthetic-free ingredients, ethanol’s recognition as a safe and plant-derived solvent strengthens its role in clean-label formulations. Organic-certified and non-GMO ethanol variants are gaining premium positioning, particularly in North America and Europe. The nutraceutical industry is also expanding ethanol-based herbal extraction processes to meet rising global demand for plant-based supplements and fortified foods.

Premiumization of Global Alcohol Markets

Premium spirits and craft beverage segments are expanding rapidly across Asia-Pacific, Latin America, and the Middle East. Distilleries require high-purity (96%–99.5%) ethanol for consistent quality and flavor stability. Countries such as India, Vietnam, Mexico, and Brazil are witnessing rising middle-class consumption of premium spirits. This trend is encouraging investments in specialized distillation, improved fermentation yield technologies, and supply contracts focused on purity assurance. Export-driven spirits industries are increasingly securing long-term ethanol procurement agreements to ensure supply reliability.

What are the key drivers in the food grade ethanol market?

Rising Alcoholic Beverage Production

The global alcoholic beverages industry, valued at over USD 1.7 trillion, continues to expand steadily, particularly in emerging markets. Increasing urbanization, disposable incomes, and premium alcohol consumption are directly increasing food grade ethanol demand. Craft breweries and boutique distilleries are further driving decentralized ethanol procurement across developed economies.

Growth in Food Processing & Preservation

Ethanol plays a critical role in vinegar manufacturing, preservation processes, and extraction of essential oils. The processed food industry’s expansion, particularly in Asia-Pacific and Latin America, is contributing to higher industrial ethanol consumption. Rising global trade in packaged foods and ready-to-eat products strengthens this demand trajectory.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in corn, sugarcane, molasses, and wheat prices significantly affect production costs. Weather patterns, global trade disruptions, and biofuel policy shifts influence feedstock availability and pricing, impacting producer margins.

Regulatory & Excise Complexities

Food grade ethanol overlaps with beverage alcohol regulations, resulting in strict licensing requirements, taxation frameworks, and compliance standards. Regulatory inconsistencies across regions may delay capacity expansions and increase operational costs.

What are the key opportunities in the food grade ethanol industry?

Expansion in Emerging Asian Markets

India is projected to grow at nearly 9–10% CAGR, driven by increasing alcohol consumption and fermentation industry expansion. Southeast Asia is also investing in distillation capacity, supported by government incentives. New entrants can benefit from rising regional demand and export opportunities.

Organic & Specialty Ethanol Production

Demand for organic-certified ethanol is rising among premium beverage and natural food producers. Companies offering traceability, sustainability certification, and specialty purity grades can capture higher margins and long-term supply contracts.

Source Insights

Corn-based ethanol dominates the global food grade ethanol market, accounting for approximately 38% of the 2025 market share. Its leadership is primarily driven by abundant raw material availability, well-established supply chains, and highly efficient dry- and wet-milling fermentation technologies. The United States and China lead production due to large-scale corn cultivation, advanced bioprocessing infrastructure, and government-supported agricultural productivity programs. The strong integration between corn processing industries and ethanol manufacturing further reduces production costs and ensures stable output, reinforcing corn’s position as the leading source segment.

Sugarcane-based ethanol follows as the second-largest source, particularly strong in Brazil and India. The segment benefits from vertically integrated sugar mills, lower feedstock costs in tropical climates, and favorable agro-climatic conditions that allow multiple harvest cycles annually. Brazil’s mature ethanol ecosystem and India’s expanding sugar-to-ethanol diversion programs continue to enhance production capacity, making sugarcane ethanol highly competitive in cost-sensitive and export-oriented markets.

Purity Level Insights

The 96%–99.5% purity segment holds around 42% of global market share, making it the leading purity category. Its dominance is driven by extensive utilization in spirits production, brewing, flavor extraction, and food processing applications where high purity and consistent organoleptic properties are essential. The segment benefits from its optimal balance between production efficiency and regulatory compliance, making it the preferred choice for large beverage manufacturers seeking quality stability and cost efficiency.

Absolute ethanol (≥99.5%) is witnessing increasing demand, particularly in premium beverage formulations, pharmaceutical-grade food applications, herbal extraction, and specialty flavor processing. Growth in this segment is supported by stricter food safety regulations, rising demand for ultra-high purity ingredients, and expanding use in nutraceutical and functional product development.

Application Insights

Alcoholic beverages represent the largest application segment, accounting for nearly 61% of total market revenue in 2025. The segment’s leadership is driven by growing global consumption of spirits, beer, wine, and craft beverages, alongside premiumization trends and expanding middle-class populations in emerging economies. Rising demand for flavored spirits, ready-to-drink cocktails, and artisanal alcoholic products continues to stimulate ethanol requirements. Export-oriented production in major beverage-producing nations further strengthens this segment’s dominance.

Vinegar production and food extraction applications are expanding steadily at 6–7% annually, supported by rising processed food demand, increased adoption of natural preservatives, and growth in flavor and fragrance industries. The expanding clean-label movement and preference for plant-based extracts are further contributing to sustained growth across these applications.

Distribution Channel Insights

Direct industrial sales dominate the distribution landscape with approximately 54% market share, as large beverage manufacturers and food processors prefer long-term supply contracts to ensure quality consistency, traceability, and price stability. Vertical integration strategies and strategic procurement agreements strengthen supplier relationships and reduce volatility risks. The scale of industrial beverage production and export-driven contracts serve as the primary growth driver for this channel.

Bulk distributors and intermediaries play a critical role in serving mid-sized distilleries, regional breweries, and food processors. Their presence ensures logistical flexibility, smaller shipment capabilities, and regional market penetration, particularly in developing economies where fragmented production structures exist.

End-Use Industry Insights

Beverage manufacturers account for nearly 58% of total food grade ethanol demand, making them the dominant end-use industry. The segment’s growth is driven by rising global alcohol consumption, expansion of craft distilleries, increasing demand for premium and flavored spirits, and strong international trade in whisky, tequila, wine, sake, and specialty liquors. Export-driven demand from tequila in Mexico, whisky in Scotland, wine in France, and sake in Japan significantly contributes to global ethanol trade flows and capacity expansion.

The fastest-growing end-use segment is nutraceutical and herbal extraction, expanding at over 8% CAGR due to rising plant-based product consumption, growing awareness of botanical supplements, and increasing demand for natural health formulations. Expanding pharmaceutical-grade food applications and functional beverages are further accelerating ethanol consumption within this segment.

| By Source (Feedstock) | By Purity Level | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 34% of the global market share in 2025, making it the leading regional market. Growth is supported by large-scale fermentation capacity, expanding beverage industries, and rising disposable incomes across China, India, Japan, and Southeast Asia. China’s extensive alcohol production industry and strong industrial fermentation capabilities sustain consistent demand. India is the fastest-growing country in the region, expanding at nearly 9–10% CAGR due to increasing spirits consumption, rapid urbanization, and government-supported ethanol infrastructure development. Rising demand for premium alcoholic beverages and growing food processing activities across ASEAN nations further drive regional expansion.

North America

North America accounts for nearly 28% of global market share, led by the United States’ advanced corn-based ethanol production facilities and strong agricultural productivity. The region benefits from integrated bio-refinery infrastructure, technological advancements in fermentation efficiency, and established distribution networks. Growth is further supported by strong demand for craft beer, premium spirits, and flavored alcoholic beverages. Canada also contributes through expanding food processing industries and high regulatory standards that favor premium-grade ethanol production.

Europe

Europe represents about 24% of global demand, driven by France, Germany, the United Kingdom, and Italy. The region’s growth is supported by strict purity regulations, advanced distillation technologies, and strong export performance in premium alcoholic beverages such as wine, whisky, and specialty liquors. Increasing demand for natural food ingredients, sustainable production practices, and high-quality beverage exports reinforces Europe’s position as a premium ethanol producer. Regulatory emphasis on food safety and traceability further drives demand for high-purity ethanol grades.

Latin America

Latin America holds around 8% of global market share, led by Brazil and Mexico. Brazil’s well-established sugarcane-based ethanol ecosystem and cost-efficient production structure provide a strong competitive advantage. Mexico’s tequila exports significantly contribute to ethanol demand, while expanding beverage manufacturing across Argentina and Chile supports regional consumption. Favorable climatic conditions for sugarcane cultivation and export-oriented beverage production remain primary growth drivers.

Middle East & Africa

The Middle East & Africa region accounts for roughly 6% of global demand. Growth is led by South Africa’s beverage production sector and the UAE’s hospitality-driven consumption patterns. Nigeria and the UAE represent the fastest-growing markets due to expanding food processing industries, rising urbanization, and increasing tourism-related beverage demand. Investments in food manufacturing infrastructure and import-driven supply chains are gradually strengthening regional market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Food Grade Ethanol Market

- Archer Daniels Midland Company (ADM)

- Cargill Incorporated

- Green Plains Inc.

- Valero Energy Corporation

- POET LLC

- Raízen S.A.

- Wilmar International Ltd.

- MGP Ingredients Inc.

- Tereos Group

- CropEnergies AG

- Cristalco SAS

- The Andersons Inc.

- Thai Ethanol Power Public Co. Ltd.

- Jiangsu Huating Biotechnology Co. Ltd.

- Alcoholes del Uruguay (ALUR)