Food Automation Market Size

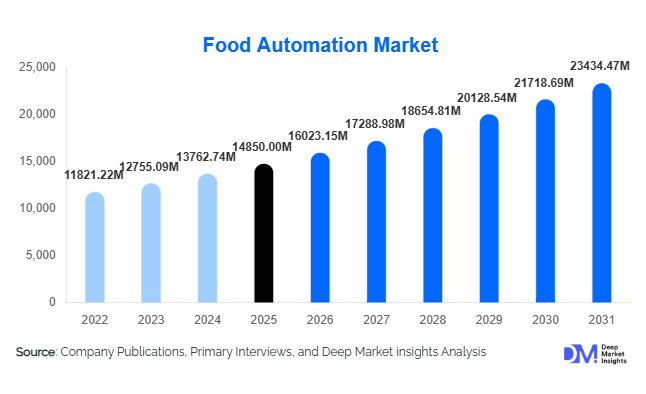

According to Deep Market Insights, the global food automation market size was valued at USD 14,850 million in 2025 and is projected to grow from USD 16,023.15 million in 2026 to reach USD 23,434.47 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The food automation market growth is primarily driven by rising labor shortages in food processing facilities, increasing demand for packaged and convenience foods, and stricter food safety regulations worldwide. Manufacturers are increasingly integrating robotics, AI-enabled inspection systems, automated material handling, and smart control systems to improve productivity, reduce contamination risks, and enhance operational efficiency.

Key Market Insights

- Robotics and AI-powered inspection systems are rapidly transforming food production lines, reducing human intervention and improving consistency and hygiene compliance.

- Packaging automation remains the largest revenue-generating operation segment, driven by high-speed labeling, palletizing, and flexible packaging requirements.

- North America dominates the global market, supported by high labor costs and advanced manufacturing infrastructure.

- Asia-Pacific is the fastest-growing region, fueled by industrial expansion in China and India and rising processed food consumption.

- Fully automated systems account for the largest automation level share, as large processors seek throughput optimization and cost stability.

- Software-led automation solutions, including MES and predictive analytics, are emerging as high-margin growth areas within the broader automation ecosystem.

What are the latest trends in the food automation market?

AI-Integrated Vision and Quality Inspection Systems

Food manufacturers are increasingly deploying AI-powered machine vision systems for contamination detection, grading, and quality assurance. These systems can detect micro-defects, foreign particles, and inconsistencies in real time, reducing recall risks and improving compliance with global food safety standards such as HACCP and ISO 22000. Vision-guided robotics are also being used for precise cutting and portioning, particularly in meat and poultry processing. As food safety regulations tighten globally, demand for intelligent inspection systems is accelerating, especially in export-oriented markets where traceability and compliance documentation are critical. Integration with cloud-based monitoring platforms further enhances predictive maintenance and operational transparency.

Collaborative Robotics and Flexible Automation

Collaborative robots (cobots) are gaining traction in small- and medium-scale food processing units due to their flexibility, lower cost of deployment, and ease of integration. Unlike traditional industrial robots, cobots can safely operate alongside human workers and adapt to multi-product production environments. This trend aligns with the growing demand for small-batch production, customized packaging, and plant-based food lines. Robotics-as-a-Service (RaaS) models are also emerging, allowing processors to adopt automation with lower upfront capital investment. This flexibility is reshaping adoption patterns, particularly among mid-sized processors transitioning from semi-automated to fully automated systems.

What are the key drivers in the food automation market?

Labor Shortages and Rising Wage Pressures

The food processing industry is facing persistent labor shortages, particularly in North America and Europe. Wage inflation and high employee turnover have increased operational costs significantly. Automation helps manufacturers stabilize production capacity, reduce dependency on manual labor, and ensure operational continuity. In high-volume segments such as meat processing and beverage bottling, automation has become essential for maintaining profitability and meeting demand fluctuations.

Growth of Processed and Convenience Foods

Global demand for ready-to-eat meals, frozen foods, packaged snacks, and beverages is expanding at a steady pace. Urbanization, changing lifestyles, and rising disposable incomes are driving processed food consumption, especially in the Asia-Pacific region. This growth necessitates high-speed processing, advanced packaging automation, and warehouse automation systems. As food companies scale production, automation investment becomes critical to maintaining quality, consistency, and cost efficiency.

What are the restraints for the global market?

High Initial Capital Investment

Food automation systems require significant upfront capital expenditure, particularly for robotics, integrated control systems, and end-to-end automated lines. Small and mid-sized enterprises often face financing constraints, delaying large-scale automation adoption. Although long-term ROI is favorable, the initial cost remains a major barrier in developing economies.

Integration Complexity in Legacy Facilities

Many food processing plants operate legacy equipment and outdated layouts, making integration of advanced automation technically complex. Retrofitting operations can cause production downtime and require specialized engineering support. These integration challenges slow modernization efforts, especially in facilities operating under tight production schedules.

What are the key opportunities in the food automation industry?

Emerging Market Industrialization

Rapid industrialization in countries such as India, Vietnam, Indonesia, and Brazil is creating significant opportunities for automation providers. Government-backed food parks, agro-processing clusters, and export-focused food manufacturing zones are investing in modern infrastructure. Localized manufacturing and service capabilities can enable automation providers to capture growing demand in these emerging markets.

Warehouse and Cold Chain Automation Expansion

The growth of frozen foods and e-commerce grocery channels is accelerating demand for automated cold storage and warehouse systems. Automated guided vehicles (AGVs), robotic palletizers, and smart storage solutions are being integrated into distribution centers to improve efficiency and reduce spoilage. This presents long-term opportunities for automation vendors offering end-to-end logistics integration solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14850 Million |

| Market Size in 2026 | USD 16023.15 Million |

| Market Size in 2031 | USD 23434.47 Million |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Industrial robots are the leading product segment in the food automation market, accounting for approximately 22% of the total market share in 2025. Robotics adoption is particularly strong in palletizing, pick-and-place operations, cutting, and high-speed packaging lines, driven by the need for high-precision, high-throughput operations and hygiene compliance in sectors such as meat, poultry, and seafood processing. Packaging automation systems follow closely, contributing around 31% of operational automation demand when measured by application value. These systems are increasingly required for flexible packaging formats, automated labeling, sealing, and palletizing in ready-to-eat, frozen, and confectionery food lines.

Control systems, including PLC and SCADA solutions, remain a critical backbone of automation infrastructure, particularly in large-scale processing plants, enabling real-time monitoring, predictive maintenance, and process optimization. Software solutions such as Manufacturing Execution Systems (MES) are growing faster than hardware components, driven by the rising demand for traceability, regulatory compliance, analytics, and predictive maintenance capabilities. Integration of AI, IoT, and cloud-based platforms is further enhancing the operational efficiency of food processing lines, offering manufacturers actionable insights for continuous improvement and cost reduction.

Application Insights

Processing automation and packaging automation dominate application areas in the global food automation market, with packaging accounting for roughly 31% of the 2025 market value. Quality control and inspection automation is one of the fastest-growing application segments due to stringent food safety regulations, contamination detection requirements, and the need to mitigate product recalls. Storage and warehouse automation is expanding rapidly in response to growth in frozen foods, ready-to-eat meals, and e-commerce grocery distribution, while material handling automation continues to gain traction in high-volume beverage, grain, and oilseed processing facilities, where efficiency, throughput, and labor optimization are critical.

End-Use Industry Insights

The meat, poultry, and seafood segment holds the largest share of the food automation market, accounting for approximately 24% of total demand in 2025. This leadership is driven by hygiene-sensitive operations requiring robotic cutting, deboning, and inspection systems to ensure product quality, reduce contamination risks, and comply with regulatory standards. The bakery and confectionery segment follows, supported by high production volumes and automated packaging requirements. The ready-to-eat and frozen foods segment is the fastest-growing end-use industry, expanding at nearly 8–9% annually, fueled by increasing urbanization, busy lifestyles, and the surge in processed food consumption globally. Beverage processing also remains a significant contributor, particularly in high-speed bottling, labeling, and packaging operations.

Explore more data points, trends and opportunities Download Free Sample Report

Food Automation Market Segmentations

By Product Type

- Industrial Robots

- Automated Processing Equipment

- Packaging & Palletizing Automation Systems

- Sorting & Grading Systems

- Control Systems

- Food Automation Software

By Automation Level

- Semi-Automated Systems

- Fully Automated Systems

- Autonomous & AI-Integrated Systems

By Operation Type

- Processing Automation

- Packaging Automation

- Quality Control & Inspection Automation

- Storage & Warehouse Automation

- Material Handling Automation

By End-Use Industry

- Dairy Processing

- Bakery & Confectionery

- Meat, Poultry & Seafood

- Beverages

- Fruits & Vegetables Processing

- Ready-to-Eat & Convenience Foods

- Frozen Foods

- Grain & Oilseed Processing

By Distribution Channel

- Direct OEM Sales

- System Integrators

- Aftermarket Services & Retrofits

Regional Insights

North America

North America accounts for approximately 34% of the global food automation market in 2025, with the United States representing nearly 78% of regional demand. The region’s growth is primarily driven by high labor costs, stringent food safety regulations, and advanced manufacturing infrastructure, which encourage food processors to adopt robotics, packaging automation, and quality inspection solutions. Meat, poultry, and beverage processing are key applications fueling demand. Additionally, ongoing digitalization in manufacturing facilities, the adoption of Industry 4.0 technologies, and government incentives for smart factory implementations are further accelerating automation adoption in North America.

Europe

Europe holds around 27% of the global market share, led by Germany, France, Italy, and the Netherlands. The region benefits from strong regulatory frameworks for food safety, such as EU food hygiene directives and HACCP compliance mandates, which drive adoption of quality control and inspection automation. Germany leads the region due to its advanced manufacturing base, robust export-oriented food processing industry, and investments in Industry 4.0 technologies. Additionally, the shift toward sustainable and energy-efficient manufacturing processes, coupled with increasing demand for ready-to-eat meals and processed foods, is supporting the growth of packaging and process automation systems across Europe.

Asia-Pacific

Asia-Pacific accounts for nearly 28% of the global market and is the fastest-growing region with a CAGR exceeding 9%. China contributes roughly 42% of regional demand, driven by large-scale industrial modernization initiatives, “Made in China 2025” upgrades, and high demand for packaged and processed foods. India is the fastest-growing country in the region, fueled by government-supported food parks, export-oriented processing units, and increasing urban consumption of convenience foods. Japan, South Korea, and Southeast Asian countries are also investing heavily in advanced food automation systems for high-volume bakery, beverage, and dairy processing. Drivers for regional growth include rising labor costs, evolving regulatory frameworks, and the need for efficiency and scalability in meeting both domestic and export-oriented food demand.

Latin America

Latin America represents approximately 7% of the global food automation market, with Brazil leading regional demand due to its dominant meat export industry. The growth in this region is driven by automation adoption in processing, inspection, and packaging systems to comply with international safety and quality standards. Rising labor costs, government incentives for industrial modernization, and increased demand for packaged and frozen foods in urban centers are supporting growth. Argentina and Mexico are also investing in automation to enhance production efficiency and competitiveness in global markets.

Middle East & Africa

This region accounts for about 4% of global demand. In the Middle East, Saudi Arabia and the UAE are investing in food security, cold chain infrastructure, and local processing capabilities, which is driving automation adoption in processing, packaging, and storage systems. In Africa, South Africa leads regional demand due to its established food processing infrastructure and a growing need for compliance with export regulations. Drivers for regional growth include rising urban populations, government initiatives to modernize food production, and increasing investment in high-volume automated processing facilities to ensure quality, hygiene, and operational efficiency.

Key Players in the Food Automation Market

- ABB Ltd.

- KUKA AG

- FANUC Corporation

- Rockwell Automation

- Siemens AG

- Mitsubishi Electric

- Schneider Electric

- Tetra Pak International

- GEA Group

- Marel hf.

- JBT Corporation

- SPX FLOW

- Bosch Rexroth

- Yaskawa Electric

- Bühler Group